Topics in this section: - European REIT sector divide may narrow if disruptive risks abate - REIT Indexes face risk-on, risk-off rollercoaster - Headwinds for mall REITs won't fade away easily - Unwinding risks may pare segment divide - Virus relief, rent re-basing may unwind discounts

European REIT sector divide may narrow if disruptive risks abate

The promise of a vaccine in 2021 has triggered a lurch in the performance of retail and office REITs, yet the chasm between their share prices and reported net assets requires both virus and structural risks to fade. Safe-haven logistics and residential segments may stay firm but lose some luster if low-valued retail and office segments catch up.

REIT Indexes face risk-on, risk-off rollercoaster

European REITs may continue to vacillate while the promise of a vaccine is weighed against the immediate challenges of rent collection and vacancies. Their 23% underperformance in 2020 reflects the present threats and long-term concerns about rising online retail and less office-based work. The structural changes may dampen enthusiasm, even when the short-term threats are clear. These matters weigh on offices and retail segments, so that volatility may be more exaggerated than for more-resilient industrial or residential REITs.

Low interest rates may help shore up investment demand for real estate that offers robust income, keeping yields firm and paring decline in property values. Industrial property yields may tighten, while office and retail yields may reflect the oscillation in risk appetite and rent re-basing.

Headwinds for mall REITs won't fade away easily

REITs with mall exposure (Unibail-Rodamco-Westfield, Klepierre, Landsec, British Land and Merlin Properties) still face an uphill battle in 1H as unscheduled closings continue to threaten rent. Mall valuations in 2020 could decline 15-25% in the U.K., less so for continental malls, yet share prices have tumbled more than 40%, hurt by discounted equity calls and cancelled dividends. Structural trends for offices may accelerate, bifurcating underlying values between prime and unmodernized space. REITs focused on city centers (Derwent, Gecina) may fare better.

Nordic and German residential landlords and logistics-focused REITs are relatively unscathed by the virus and populate the leaders' board for 2020. Continued resilience is probable, and their ability to pay dividends provides a total-return advantage.

Unwinding risks may pare segment divide

The gulf between equity market valuations for retail REITs and industrial and residential specialists may dissipate only when retail rents are lowered to sustainable occupancy costs. A lurch in retail and office REIT shares on positive vaccine news may signal a partial switch from defensive property segments as virus risks unwind. Yet uncertainty over rent intake, earnings, dividends and mall values may keep a sizable discount in place. Underlying office property resilience is hard to square with the uncertainty of working from home, and shares may not reflect full value until occupiers make space decisions.

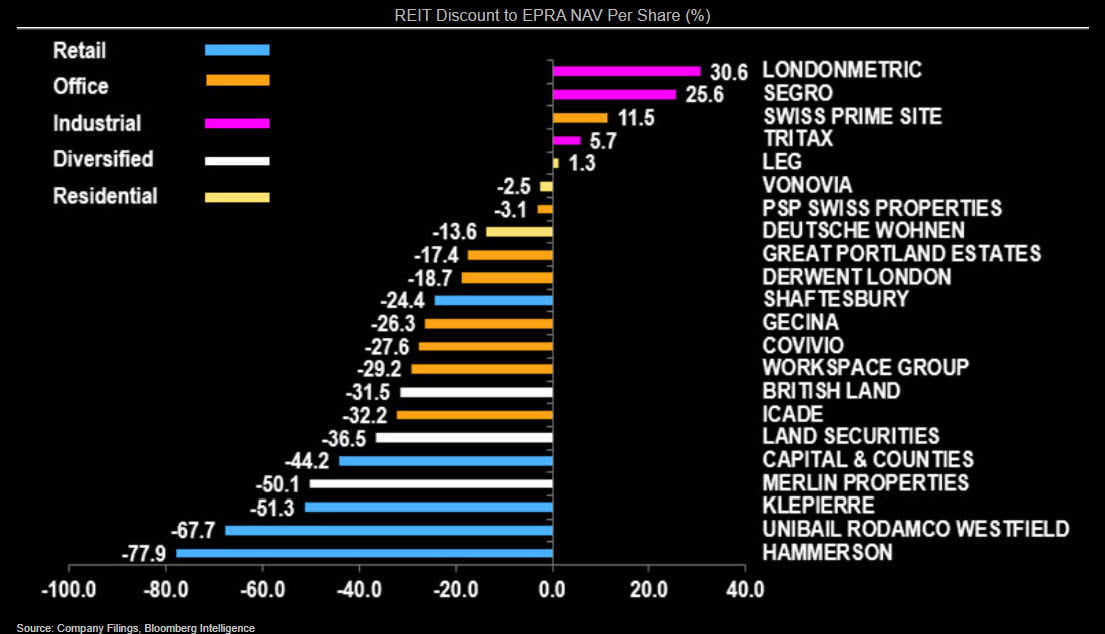

Segro and LondonMetric trade above asset value as growing demand for space buoys earnings and values. German residential companies Vonovia, Deutsche Wohnen and LEG are proving resilient, backed by government support.

Virus relief, rent re-basing may unwind discounts

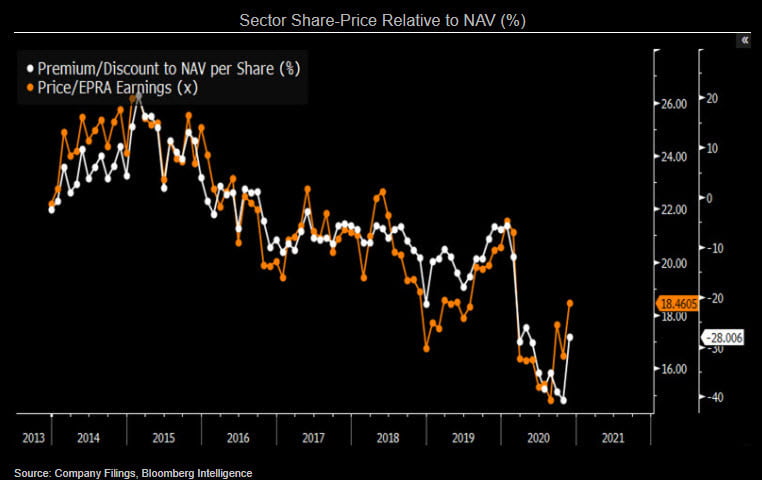

European REITs' average discounts may move toward the 10-year average of 7.2% in 2021, but that would require some of the lower built-in property declines to be realized and the virus and longer-term structural risks to unwind. A floor upon which retail can begin to build a recovery looks imminent at British Land and Hammerson, yet tenant insolvency may weigh on mall REITs, especially in 1H21. Office REITs also need to understand the role and dimensions of offices before the gap narrows.

Taking the average loan-to-value ratio (LTV) of 36% and average discount to net asset value of 28%, the built-in sector portfolio value decline is 22%, with retail REITs at 71% vs. offices at 32%, including diversified REITs in both. Lower LTVs amplify the implied decline. Industrials, Segro and LondonMetric, still price in growth.