Topics in this section: - Covid's legacy won't show in Europe REIT 2021 earnings or values - Weak rent intake puts mall REIT cash flow in focus - Race for online fulfillment buoys industrial REITs - Office REIT's resilient as prime rents polarize from secondhand - Homebuilding rebound may be at hand in 2021

Covid's legacy won't show in Europe REIT 2021 earnings or values

Real estate company earnings and portfolio values in 2021 may defy Covid-19's disruptive repercussions on socializing and working. In our scenario where restrictions cease in 2H, retail REITs must muster liquidity to survive low 1H rent intake yet office REIT earnings may resist disruption in work practices. Logistics and residential landlords may expand.

Weak rent intake puts mall REIT cash flow in focus

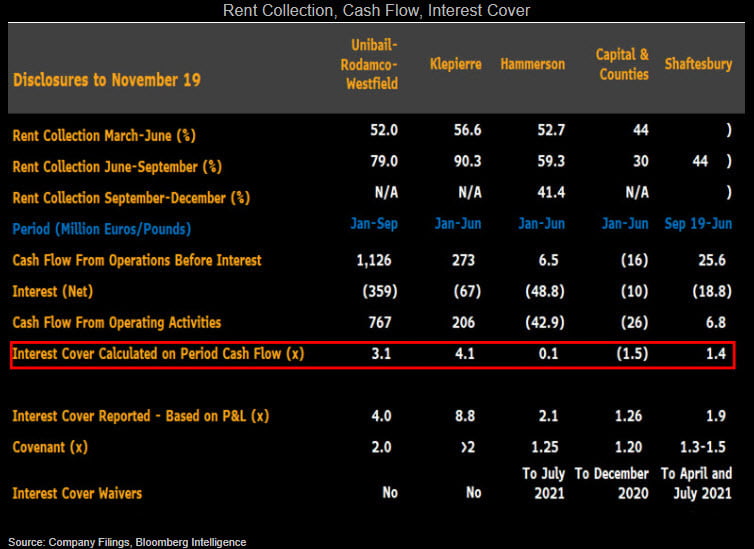

Subdued rent intake may pressure REITs with a focus on retail, hospitality and leisure as depleted cash flow could struggle to cover interest costs even if the covenant-defined interest cover indicates ample room. That's because covenants are based on Ebitda, including deferred rent, and provisions lag billing. Yet tenant sales in September reached 85% of normal, boding well for the eventual recovery.

European REITs focused on these sectors may endure severely restricted rent collection until 2H21 as store lights flick on and off to tame the virus. Hammerson and Shaftesbury tapped shareholders for funds in 3Q to lower debt and Capital & Counties has plentiful cash. URW's failed equity raise may haunt the new management if rent collection sours during winter lockdowns. Klepierre's strong 3Q replenishes cash ahead of winter.

Race for online fulfillment buoys industrial REITs

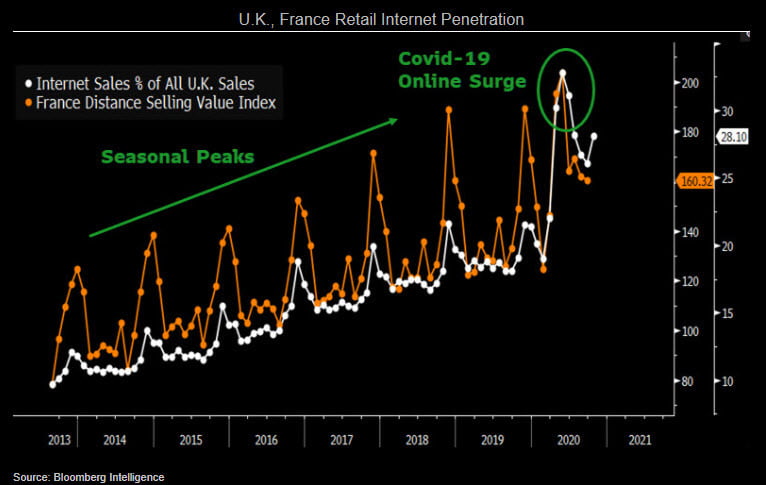

The rollout of online fulfillment infrastructure has accelerated due to shop closings, creating a surge in demand for warehousing that may persist in 2021 to keep rents and values rising. Segro has ramped up development to capture demand and may deliver its consistent 8-10% total returns in 2021. Online distribution requires more warehousing space than physical retail and in the U.K. every three percentage points of higher penetration requires a million sq./ft of extra space. At the dip in August, penetration was 8.6 ppt above August 2019. Supply capacity may take several years to catch up with demand.

Shop closings triggered a surge in online fulfillment, peaking at 32% in May in Britain with year-over-year growth tracking above 50% since. In France, penetration is 20-30% higher and similar trends are evident across Europe.

Office REIT's resilient as prime rents polarize from secondhand

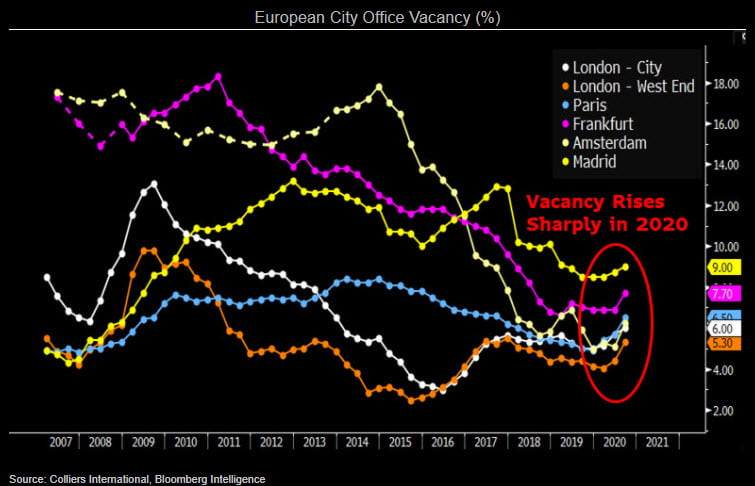

The Covid-19 impact for European city offices could be a faster paced change to more flexible and less formal working cultures, yet that may still be too slow to feature in 2021 performance. The market is bifurcating with limited supply of new space in both Paris and London propping up rent while higher second-hand vacancy (74% of London's vacant space) takes the hit from home-working demand attrition. Gecina, Derwent, Covivio, Great Portland Estates, Merlin, Landsec and British Land have collected over 95% of office rents and may prove resilient in 2021.

Asset values for well-let space may see less than 2-5% attrition during the pandemic yet vacant space, especially secondhand may be weighed by 5-10% lower rental values in London and new supply in Paris's La Defense.

Homebuilding rebound may be at hand in 2021

Our Covid-19 scenario that anticipates a 2H21 recovery may bode well for housing transactions, output and house prices. The robust momentum of residential permits in Germany points to strong 2021 activity, while prices should be reinforced by the segment's resilience amid the pandemic and a chronic housing shortage in the country's largest cities. This should support rents and valuation gains of German landlords, Vonovia, LEG and TAG. Swedish homebuilders, including JM and Skanska, may also cheer homebuilding volume stabilization -- already visible in new starts -- after a multiyear drop from a two-decade high.

We see the output of U.K. homebuilders, like Taylor Wimpey and Bellway, rebounding from its 2020 low -- even as it may trail 2019's level -- with price growth slowing vs. 2020 though, as government incentives end.