Topics in this section: - Shiny new office space may salvage EU REITs from vacancy crunch - Office value slide starts with unrenovated space - Leasing activity nose-dives except for new-builds - Mass office exodus may create large 'grey' market - City office sub-lets play havoc with rents

Shiny new office space may salvage EU REITs from vacancy crunch

More employees working at home could profoundly alter the role of offices, amending space requirements, reconfiguring use and prioritizing robust climate credentials. To start, the prime portfolios of REITs Gecina, Covivio, Derwent London, Landsec and British Land may be resilient, yet they must embrace this evolution to avoid value erosion.

Office value slide starts with unrenovated space

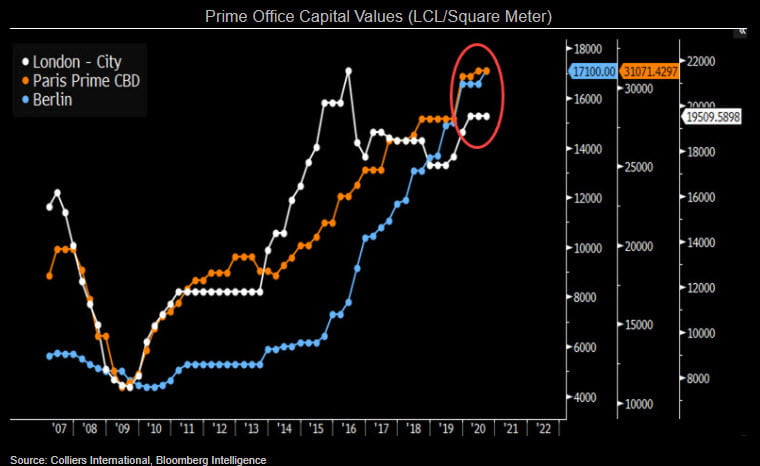

The quest for yield may offer some support to European city office values during 2021 as yield gaps have widened to record levels following monetary easing. The prime portfolios of Gecina, Covivio, Landsec, British Land and Derwent London may show some resilience. Yet with rent reliant on how work practices evolve, values of unleased space could fall 10-15%, polarizing it from new, well-occupied offices. Aligning renter space needs with lease commitments may take time, softening the pace of capital-value declines.

Transaction volume slumped 74% in London, 27% in Paris and 33% in German cities through August. Ominously, London offices for sale have jumped 435% since May, outweighing actual sales by 3x. Landlord distress is rare as occupiers are paying rent but this could change as tenants vacate secondhand space.

Leasing activity nose-dives except for new-builds

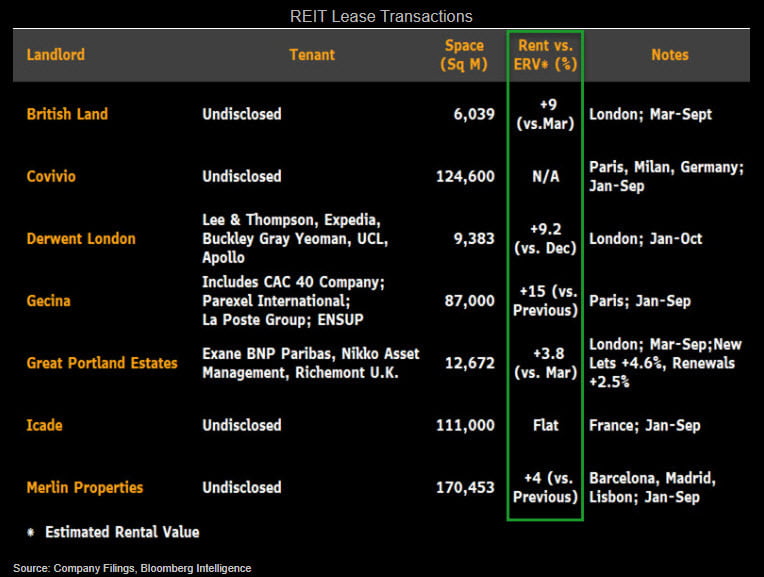

The 50-75% decline in office space take-up during 2Q-3Q in major European cities may add to fears that more remote working will lower demand for office space, yet deals struck by REITs have largely been secured at better than expected rents. Deals are taking longer as occupants reassess needs so activity may rise in 2021 once requirements become clear. REITs report that newly modernized space that's flexible, healthy and well located is sought after so that buildings under construction are generally 50-100% pre-let on completion.

Landlords in London, Paris and Berlin entered the pandemic with vacancy below average, rents at 10-year highs and developments significantly pre-let -- 60% in central London. Flex working space, if offering specifically allocated areas, is still proving popular.

Mass office exodus may create large 'grey' market

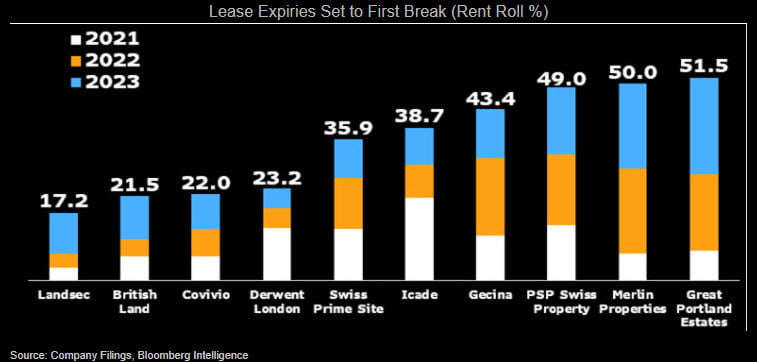

A swift change in office occupancy in European cities may be stymied by long-term leases yet large occupiers may consider sub-letting space at discounts, creating a 'grey market' and disrupting rent dynamics. Major office REITs report first lease breaks for just 10.2% of the rent roll in 2021, so that this grey and potentially vacant space won't cut REIT rental income in the short term. It could cut rental values, pressuring portfolio values. British Land forecasts a 10-15% fall in central London rents over the next year with secondary space falling more sharply than prime.

Great Portland Estates is the REIT most exposed to vacancies, given 51.5% of its leases expire within three years. Many are buildings with advanced renovation plans, though a faster-than-expected tenant exodus would still pressure revenue.

City office sub-lets play havoc with rents

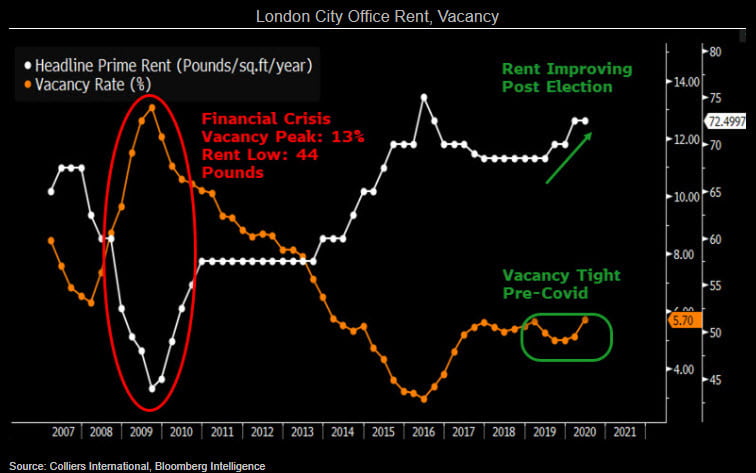

Traditional London City office rents may be buffeted by the Coronavirus with the danger an emergence of a large "grey" market of sub-let space causing price disruption. Tenants wanting to shed space but trapped in 10-15 year leases won't price sub-let rents for yield but in relation to their operating costs. For example, to reduce occupier cost by 10% an occupier three years into a ten year lease paying 2018 prime rent could sub-let a quarter of its space at a 60% discount, or 62% below current prime rent. This could cut secondary property rent sharply slashing average rent, though prime may be less pressured.

Physical vacancy is above 70% now, yet may fall if transport concerns and virus cases wane. Reduced worker densities may cushion the amount of redundant space so that vacancy avoids the financial-crisis nadir of 13%.