Topics in this section: - European retail property's online nadir in sight for late 2021 - Value crunch for malls may linger until 2022 - Tenant deals begin transition to sustainable rent - Mall REITs' loan-to-value ratios set to soar - Development plans stripped to minimum to conserve cash

European retail property's online nadir in sight for late 2021

Mall REITs still face challenges through 2021 as tenants grapple with unscheduled closures and cash rent receipts are squeezed. Landlords are being forced to accelerate rent transitions to lower sustainable levels, straining rental income and weighing on property values. Yet a nadir may be found by end-2021, leading to stability and eventual recovery.

Value crunch for malls may linger until 2022

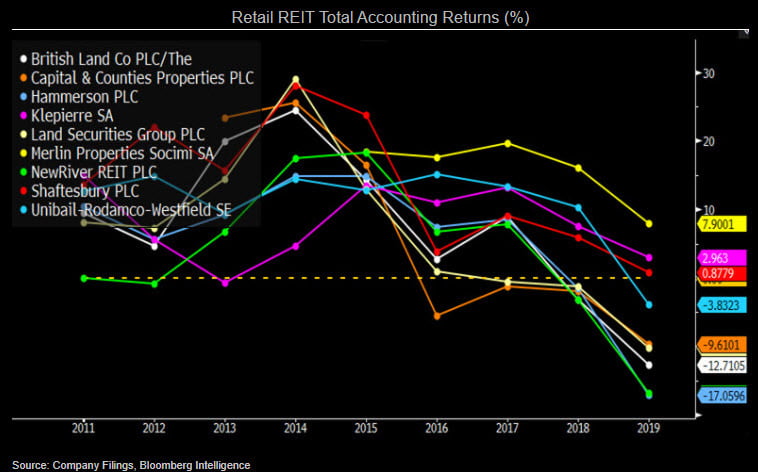

Retail REITs' total accounting returns may stay negative until 2022 as REIT regime dividend payments track earnings lower, and mall values may decline further. U.K. underlying property values slumped 15-20% in 1H, and they may trend lower while the virus rages, causing similar cuts to total returns. Attrition for continental malls may be milder -- Klepierre reported a 2.8% value decline in 1H -- as shops reopened sooner, reducing stress. Halting the slide requires rents to be re-based to sustainable levels, yet deals struck during the virus may achieve that over the next year.

URW, Klepierre, Hammerson, British Land, Landsec, Shaftesbury and Capital & Counties have supported tenants and are negotiating new deals, which may take rents 10-20% below previous levels or be based on sales.

Tenant deals begin transition to sustainable rent

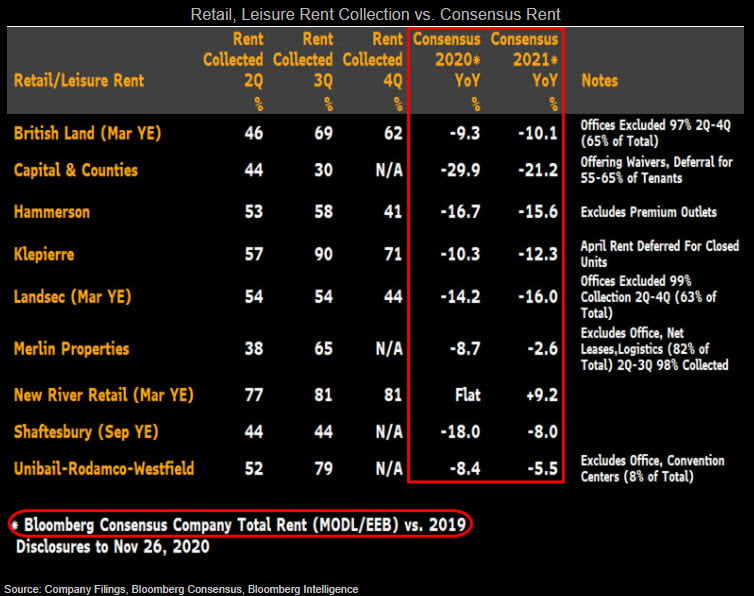

Retail landlords' negotiations with tenants to provide immediate relief and forge sustainable future rents may facilitate recovery into 2022, an outcome that consensus rent forecasts are beginning to signal. Yet until a vaccine is distributed, more closures may mean receipts are erratic, varying with tenant sales. Deals are customized, yet most landlords have sought pain-sharing compromises so that lower rents are compensated with longer leases or more space. By year-end, most REITs will have reached solutions with all but those refusing to pay.

Klepierre and URW's continental European malls have fared better than those in the U.K., where internet penetration is higher, eviction is banned and closings longer. Central London has lost commuter and tourist foot traffic, hitting Shaftesbury and Capital & Counties' tenants.

Mall REITs' loan-to-value ratios set to soar

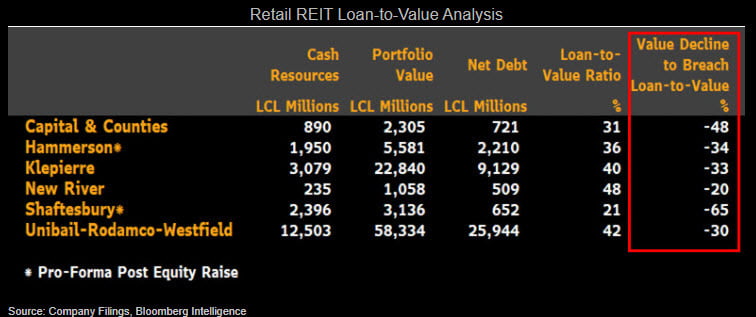

Retail REITs' liquidity assessments may prioritize interest coverage due to curbed cash receipts, yet loan-to-value ratios could also rise sharply. While most have a cushion for a decline of 30% or more in portfolio value before breaches at a proportionately consolidated level occur, debt repayments or refinancings require access to liquidity in the debt markets. If the ratio rises, credit ratings could be lowered, and that could increase financing costs or limit liquidity. Credit agencies look at interest coverage as well, so a rating may be reduced even if the LTV is sound.

Hammerson and Shaftesbury raised equity to alleviate financial stress, yet URW's proposed capital increase failed. Despite a credit downgrade, the REIT sold 2 billion euros of bonds at 0.625% for 6 years and 1.375% for 11-year maturity in November.

Development plans stripped to minimum to conserve cash

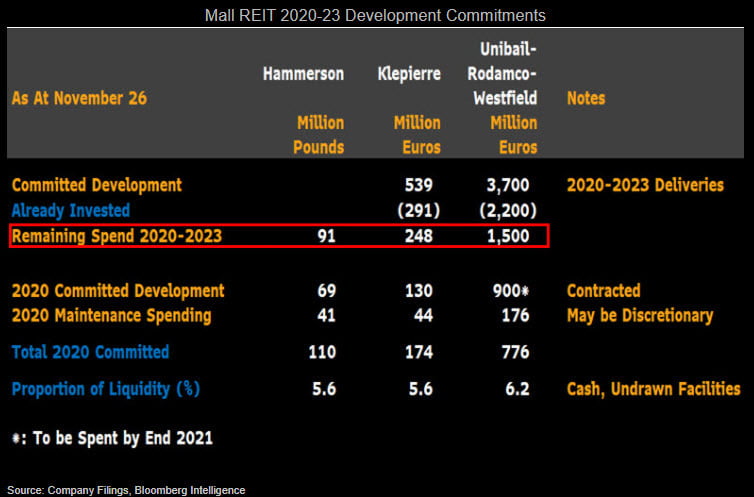

Retails REITs' need to conserve cash following limited rent collection could cut sector development significantly over the next two years, with low-cost, high-impact upgrades preferred. Unibail-Rodamco-Westfield, Klepierre and Hammerson have chosen not to embark on new projects, and deferred or paused them where possible. URW has cut 2.9 billion euros of potential investment from its controlled pipeline and shaved a committed spend to 1.5 billion euros. Hammerson hopes to complete on-site projects in France, though material savings have been identified and outlays have been cut to 110 million pounds in 2020. Shaftesbury and Klepierre usually focus on upgrades and renovation, which offer more flexibility in terms of timing and investment.