by Steve Niven, Bob Shea and Gary Stone

As we began to work our way through ESMA’s MiFID II implementation standards, we started to formulate a framework for understanding how aspects of the regulation are going to affect the investment life cycle on the buy side. Structuring this regulation is extremely important because at 585 pages for the regulatory technical and implementing standards alone (Annex I), MiFID II is an expansive document — and more is coming. At the end of November, ESMA will provide additional insight into the use of dealing commission, fixed income research and other areas.

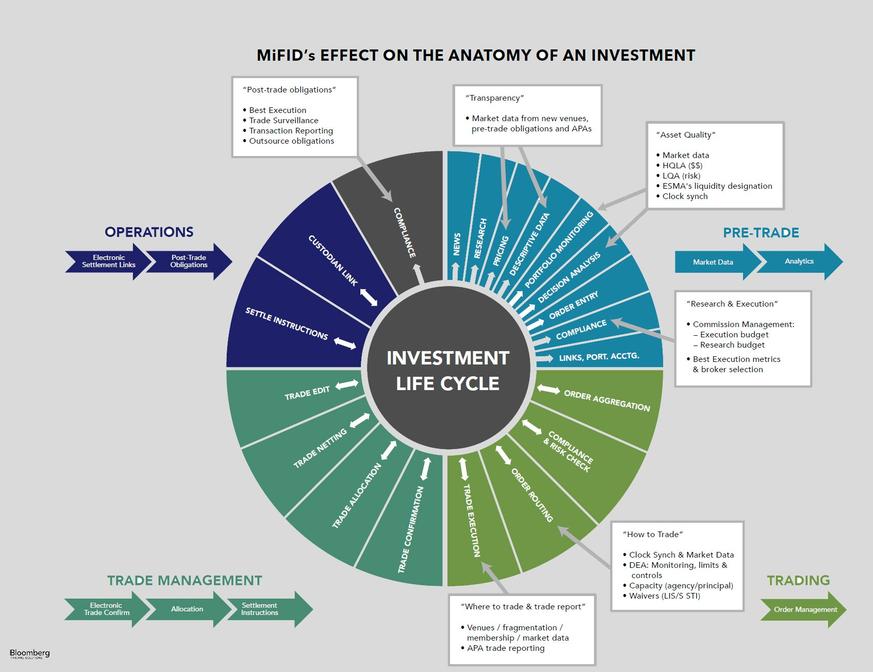

We have segmented the anatomy of an investment into eight functional activity groups.

There are defined activities within each of the functional activity groups that constitute the end-to-end investment process (workflow). It is against that backdrop — when we overlay the MiFID II changes — that the buy side can start to identify where their world will be changed.

At a high level, we look at the MiFID II regulation as resting upon three pillars:

When we break down the pillars into functional requirements, we see the regulation touching many of the workflows of an asset manager/owner.

New venues provide new data sources; APAs provide pre-trade transparency publications and post-trade publishing of trade information. Although ESMA is labeling assets as liquid/illiquid under MiFID II, each investment firm should use quantitative metrics to better understand the assets that they are placing in their portfolios. “Asset quality” quantitative metrics also require firms to identify the highly liquid assets in their portfolio to help them (pro-actively) manage their liquidity (redemptions). This isn’t solely a MiFID II issue. The principles behind the U.S. SEC’s proposal on fund liquidity are very similar. Guidance is needed as to whether the clock synchronization requirements extend into the order creation process for transaction cost analysis. We await the dealing commission guidance which may result in new compliance requirements for research and execution payments. For example, setting up independent budgets for research and execution, couple with appropriate best execution measures to demonstrate that such budgets are arrived at independently.

MiFID II is very prescriptive on how investment firms should execute. There is tremendous concern about information leakage from the new pre-trade transparency requirements as well as the post-trade trade reporting. If the buy side become members of MTFs or trading venues, then they will need to institute new monitoring, limits and controls processes and technology in accordance with the new direct electronic access (DEA) pre-trade controls requirements. Moreover, MiFID II may result in more execution method choices, competition among venues, fragmentation of liquidity and order types — all of which will need to be stitched together. The regulation will also force a new regulatory workflow.

New post-trade compliance processes will need to be formed, to deal with enhanced transaction reporting requirements, as well as the need for trade surveillance. In addition, firms outsourcing their trading and order management technology may need to develop new policies to supervise and govern their technology partners.

MiFID II is an expansive regulation. As we work through the implementation guidance and receive guidance from the 28 EU NCAs, we will expand upon this framework