by Bloomberg Intelligence analysts\ Sarah Jane Mahmud and Alison Williams

The EU’s MiFID II rules will require investment research to be paid for in one of two ways: from a fund manager’s own account, recoverable by raising fees, or via a client research-payment account. While regulators might permit research charges to be collected alongside transaction commissions, subject to stringent conditions, they maintain there should be no link to transaction value or volume. The move to an unbundled model would limit the long-held use of commissions, and may disrupt the industry worldwide.

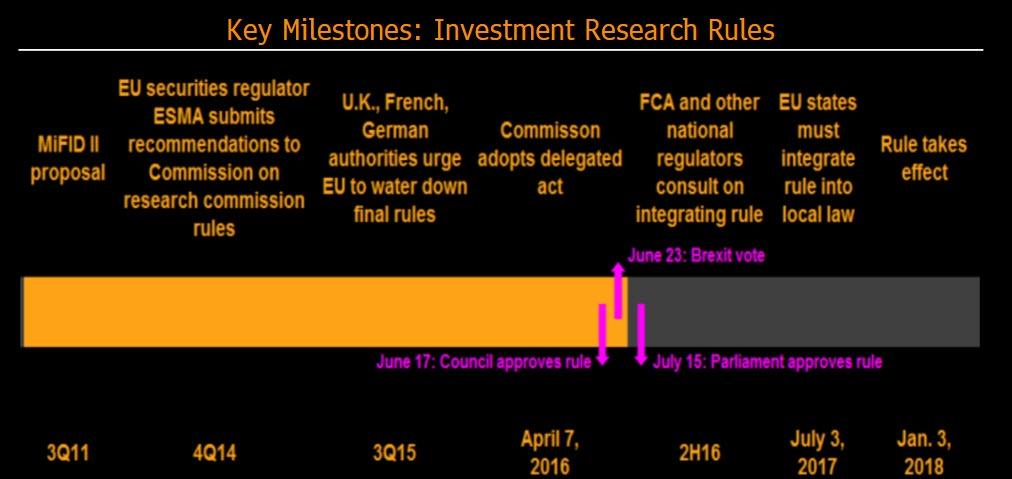

More detail on MiFID II rules separating research costs from dealing commissions will unravel in 4Q. By year-end, the U.K.’s Financial Conduct Authority, and the other EU countries’ securities regulators, will consult on integrating the rules into local law. They are likely to interpret and implement the rule differently, increasing divergence across the bloc. The European Commission’s April 7 draft rule received Parliament and Council approvals on July 15 and June 17.

Non-EU regulators haven’t yet issued proposals seeking to separate research payments from dealing commissions. Without international convergence, EU companies could become less competitive than their overseas peers. Global companies could roll out an EU-compliant system on a worldwide basis to minimize operational strain, especially as non-EU brokers will be bound by MiFID II when providing execution and research services to EU managers. This may encourage non-EU regulators to adopt the EU approach.

The rule won’t apply to non-EU investment managers that don’t have a presence in the EU. U.S. managers would be able to continue paying brokers, including those in the EU, for research on a bundled basis, subject to compliance with local rules.

Banks are reported to be adjusting pricing models for investment research in preparation for EU reforms that will prevent research from being paid for directly using dealing commissions. In an unbundled world, based on execution-only commission rates where payments for research are separated, competition in equity as well as fixed-income, currency and commodities research is likely to rise. Managers may look beyond traditional sources, triggering fragmentation. They may also move research in-house.

Asset managers that opt to pay for research via a dedicated client account will need to follow a strict budgetary and disclosure regime. This may make use of such an account too burdensome. It also poses compliance risk. Failure to follow U.K. client asset rules, for example, usually results in a hefty fine. In a retreat from prior proposals, short-term market commentary that doesn’t contain substantive analysis may be provided without charge, so not all sales or trading calls will classed as chargeable.

The Financial Conduct Authority has said it expects tighter bid and offer spreads in credit markets as a result of EU proposals — agnostic as to asset class — that seek to decouple research from trading. Fixed income research costs are typically embedded in the spread, which helps pay for the trade, and has been treated as part of a wider service. Many brokers maintain that spreads won’t change as they are competitively formed. Yet they may face regulatory pressure to reduce them when MiFID II comes into force.