by Gary Stone and Mark Croxon.

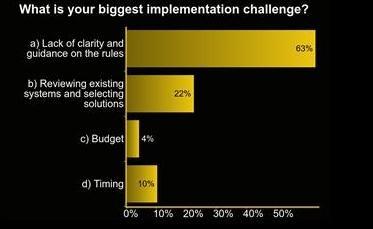

The biggest implementation challenge to MiFID II continues to be the lack of clarity and guidance on the rules. This was the overwhelming opinion of the over 200 participants who attended the MiFID II: The Market Practitioner’s View conference held at Bloomberg London on 19 October 2016.

Although little over a year is left before MiFID II starts to apply on 3 January 2018, panelists agreed that most rules are likely to be finalized only next summer, as senior regulators across the EU have indicated. Practically, this leaves five months for major systems to be built, with participants expressing their desire to begin testing of transparency and transaction reporting services in September 2017.

When the implementation delay was being discussed in November 2015, this is why we argued that a simple 12 month push-out of all the dates was not sufficient, but instead the market needed more time between the finalization of the rules and their applicability.

It doesn’t matter. The view of the market practitioners at our event could be described simply as: “it’s time to make some assumptions and get on with it.”

Specifically, in three sessions, “The Impact of MiFID II on the Functioning of the Markets”, “How are Investment Firms Meeting the Challenges of MiFID II?” and “MiFID II Related Data”, panelists almost uniformly suggested that planning, reparation and building now means creating robust systematic processes, procedures and supporting technology based on educated assumptions. More importantly, firms should document the reasoning and principles behind their decisions where there is ambiguity or guidance is pending. Waiting for clarity isn’t an option because you will simply not be far enough down the path to compliance if you don’t move forward now.

Fortunately, regulation entering into force while the guidance is still evolving is not a new concept. Most recently, the European Market Infrastructure Regulation on derivatives, central counter parties and trade repositories (EMIR) and the Market Abuse Regulation (MAR), went into force with guidance still pending. In both cases, the regulator’s examination and enforcement posture seemed to prioritize getting it right. The level of initial compliance for MiFID II expected on 3 January 18 similarly seems to focus on whether firms are making “legitimate and sensible” efforts to meet the requirements. Firms should be expected to “prove” that they are making progress through demonstrable processes, procedures, documented logic and audit of those initial decisions.

We believe that this view is implicitly confirmed by regulators when they describe MIFID II implementation as “a process, not an event.”

However, firms should also take heed of the insights offered by keynote speaker, Jenny Knott, CEO of Post Trade Risk and Information at ICAP. According to her, MiFID II provides the industry with an opportunity to serve its clients better. In order to achieve that objective, firms will need to think, behave and act differently. If you do not re-engineer your processes, the technology will not work. Technology alone does not automatically eliminate inefficiencies and reduce costs.