How can firms become "MiFID II friendly"?

When asked whether they had heard of the EU’s Markets in Financial Instruments Directive overhaul (“MiFID II”) scheduled to go into effect in January 2018, virtually everyone in a packed auditorium during Bloomberg’s inaugural Buy-Side Week 2017 New York event raised their hands. This is the good news.

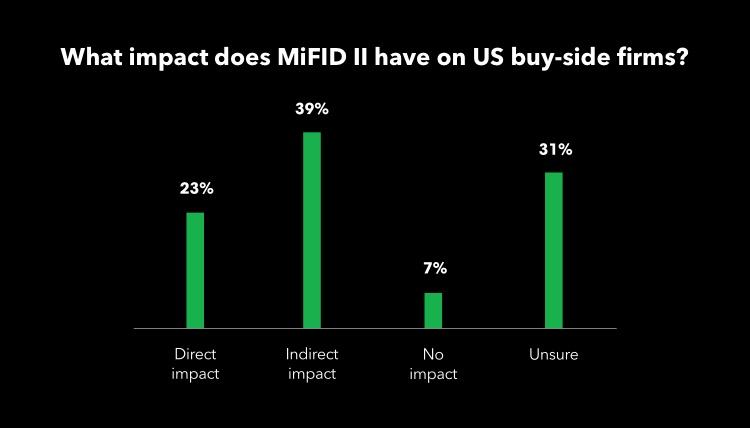

Unfortunately, the same number of people also raised their hands when asked how many needed an overview of the new regulations. Nearly two-thirds of those responding to a survey during the event said they believe MiFID II will have “direct or indirect” implications for buy-side firms, highlighting the conundrum facing many U.S.-based financial professionals just six months before the law’s implementation.

Most know about MiFID II, and most believe it will impact them in some way, but few have a specific plan to become “MiFID II Friendly.”

Broadly speaking, MiFID is a far-reaching series of European Securities and Markets Authority directives aimed at improving transparency, regulation, compliance and supervision of banks, asset managers, broker-dealers, research providers, and trading firms across the EU. The goals are laudable – increase investor protections and prevent another financial crisis – but MiFID II regulations are extremely complex and implementation requirements are extensive.

MiFID II only directly impacts EU investment firms. The UK is going a set further by gold plating the regulations and applying them to UCITS (Undertakings for Collective Investment in Transferable Securities) funds. Thus, at first glance, that MiFID II’s new rules on price transparency to the strict unbundling of research from trading commissions will only impact U.S. firms with European offices. But it’s not nearly so simple, says Bloomberg’s Market Structure and Regulatory Policy Strategist Gary Stone, because even though a U.S. firm may not fall under the MiFID II umbrella, their EU counterparties and competitors do.

“This is not just an EU problem,” Stone said. “The U.S. buy side needs to talk to their EU investors and EU brokerage partners and determine if they need anything so that they can be compliant with MiFID II.” For example, EU investors may demand the same transparency and disclosures from the U.S. active managers that they receive from the EU-based active managers. This may mean that U.S. managers may have to create an order execution policy disclosing how their U.S. desks approach executions. They may need to demonstrate through transaction cost analysis or execution price fairness benchmarks that they are taking all sufficient steps to achieve best execution. Failure raise current transparency and disclosure standards could become a competitive issue when seeking new mandates and/or result in a loss of current mandates Though not a regulatory requirement in local markets, EU investors may look at MiFID II requirements such as “immutable storage” of books and records and taping trading desk phones as a required best practices for today’s operating environment. Firms should begin to examine, “How are we stacking up against a MiFID II compliant competitor when the discussion turns to best execution practices or use of client commissions to pay for research?” If competitively, MiFID II becomes the global best practice, Stone asks, “your investors and customers may hold you to that standard – and if you decide not to, do you risk coming up short.” U.S. buy-side trading desks investing in EU assets will be operating in a new market structure where they will constantly have to evaluate whether pre-MiFID II trading strategies provide similar execution results as in the post-MiFID world. For example, U.S. traders need to be aware how they communicate with their EU brokers and pay particular attention or order size. The new pre-trade transparency regime requires trading venues and brokers that deal often and have a large market share in certain instruments to make their pre-trade firm prices publically available.

There are certain waivers – for example pre-trade prices in block sized trades do not need to be broadcasted. “Asking for a price on $49.8 million in 10-year Bunds could be different than where are you on $50 million because of the block threshold,” Stone noted. “Knowing that the price will be publicized may work against you.”

Meanwhile, a broader consideration to the EU’s new rules is whether there will be a competitive disadvantage to not complying with MiFID II directives. “There is a question whether MiFID II’s rules, or some version of them, will become best practices in the U.S.,” said Stone. “Rules around transparency, trade reporting and research may leave non-compliant firms out in the cold when dealing with new mandates.