The combination of rapidly increasing computing power for steadily decreasing costs has placed robust quantitative strategies within reach for more investment managers than ever before. Simultaneously, extremely low volatility is increasing the demand for computer-driven strategies that are able to systematically crunch exabytes of data to find an edge, while the types of structured and unstructured data sets are also expanding.

These trends are resulting in increasing capital flows to quantitative hedge funds, which commanded 17%, or $500 billion, of total hedge fund assets, according to Barclay’s.

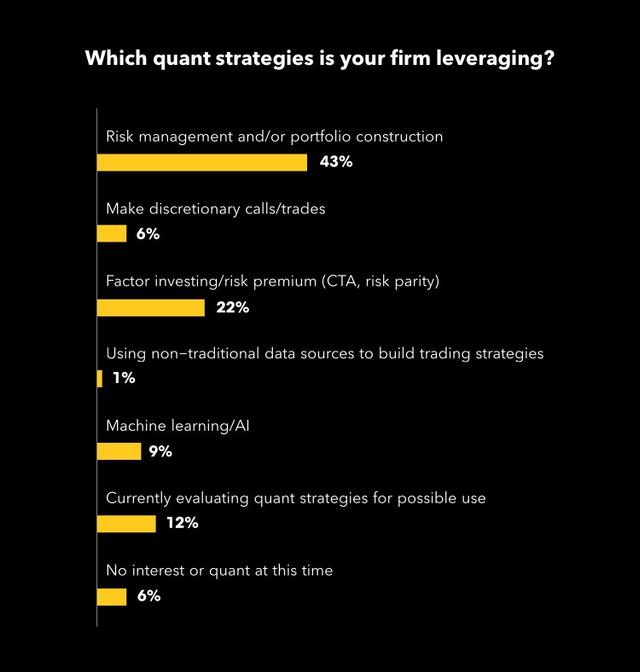

Nonetheless, with technical tools easier and cheaper to build and implement, their use has skyrocketed. 43% of respondents to a survey during Bloomberg’s inaugural Buy-Side Week 2017 New York said their firm uses quant strategies for risk management and/or portfolio construction, while another 22% employ them in factor or risk-premium strategies. Only 6% admitted to having no interest in quant at the moment, and 12% are evaluating quant strategies for possible use. There are two major distinctions to make when discussing quantitative trading notes Maria Vassalou, Partner at Perella Weinberg Partners and Portfolio Manager for the PWP Global Macro strategy.

The first delineates across the holding period of the trade, i.e. from high frequency trading to several months. The second refers to the type of information used to inform that trade, i.e. technical, fundamental and everything in between. Wall Street began its quant love affair with the former: the high-frequency trading (HFT) craze of the 1990s. Today, it is increasingly concentrated on the latter.

This shift is occurring partly because there are only so many nanoseconds you can squeeze out of a trade, but also because extraordinarily large amounts of previously uncollectable data are now available quickly and cheaply and can be processed in the cloud equally quickly and cheaply. Both open up ways of doing things that weren’t possible before.

The second distinction is using quant as a tool versus using quant as a strategy. An algorithm that systematically manages multiple types of risk in a portfolio is a tool; one that systematically places trend-following, high-frequency trades is a strategy.

In each case, use of quantitative methods is growing across the board, and it is raising not only clear use cases in which quant approaches are best suited, but also questions about the risks they pose.

“A quant approach allows you to do things otherwise not possible as an individual portfolio manager,” said PWP’s Vassalou. “Humans can’t compete in HFT and intra-day strategies, for example. For longer-term strategies, a quant approach can help provide discipline, risk management, verify your strategic thinking, and help confirm your portfolios have been structured correctly.”

Another advantage often ascribed just to HFT but applicable to quant-driven investing as a whole is an increase in liquidity. The low cost and high speed made possible by these tools has helped lower costs and tighten spreads. Consider: twenty years ago, the spread between the bid and ask of a major U.S. blue chip like General Electric was $0.20-$0.25 per share. Now it’s a penny, and often less than that in the HFT world. Granted, this hasn’t been good news for the brokers that relied on those spreads for revenue, but there is no denying it has led to tighter, more efficient markets.

At the same time, the rise of systematic managers is reducing the speed it takes for the market to find fair value. “Brexit and the Trump election are examples of events that would have taken days to work through ten years ago,” said Bill Harts, CEO of the Modern Markets Initiative. “Instead, they were flushed pretty much through the system in a matter of hours. Algos mean news and emotion are reflected much faster and to a much greater scale.”

As quant involvement grows however, there a growing concern about whether it becomes harder to generate alpha by using it. For example, the first person to study satellite photos of Wal-Mart parking lots generated an undeniable advantage from it. But once everyone studies the same data, there is no advantage, and thus less alpha.

Another fear is that quant strategies will crowd out the need for humans. That’s absurd, said former Bridgewater Chief Business Architect, Jeff Wecker. “There are plenty of opportunities for humans to deploy these ideas and tools, see greater applications and use new sources of data.”

PWP’s Vassalou agreed. “It is misplaced to think humans are out of the picture. The fact is, you still need intuition, knowledge about relationships, history, etc. Alpha requires nuance as well as data. It is not just technique.”

Interestingly, a more recent concern coming out of the quant space comes from having too much data. “Good algos start with a hypothesis, then test using the best and most complete data possible,” said PWP’s Vassalou. “But we’re seeing quants starting with data, and then looking for a hypothesis to fit it, which is very dangerous. They are solutions looking for problems.”

Ultimately, the real value may come when really great quant techniques are paired with really smart people with a lot of imagination. “Large shifts in underlying issues may make an algo ineffective until it can be tweaked,” said Wecker. “They’re not built to handle wide departures from the status quo. There are no black swan algos out there.”