Is the expense ratio the new performance chart?

There are few topics on Wall Street that rival the debate raging about passive versus active investment management. Like religion and politics, it’s become one of those subjects that one tries to avoid in polite gatherings.

The conventional wisdom, dating to 1973 and Burton Malkiel’s dart-throwing monkeys, holds that most money managers are no better (and often worse) than the broader market in generating portfolio returns, yet charge high fees. And in the past few years, it’s true that many active managers have struggled to consistently outperform their respective benchmarks. But the argument of active versus passive is actually much more nuanced than meets the eye.

Some figures to set the stage: According to Bank of America Merrill Lynch, $3.1 trillion has flowed to passive bond and equity funds, while $1.3 trillion has flowed out of active bond and equity funds since 2007. This is a colossal amount of money when considering there is about $10 trillion parked in active versus $5.8 trillion in passive funds (defined as index funds and ETFs), and starkly illustrates how much capital is abandoning the idea of an individual’s ability to beat the averages.

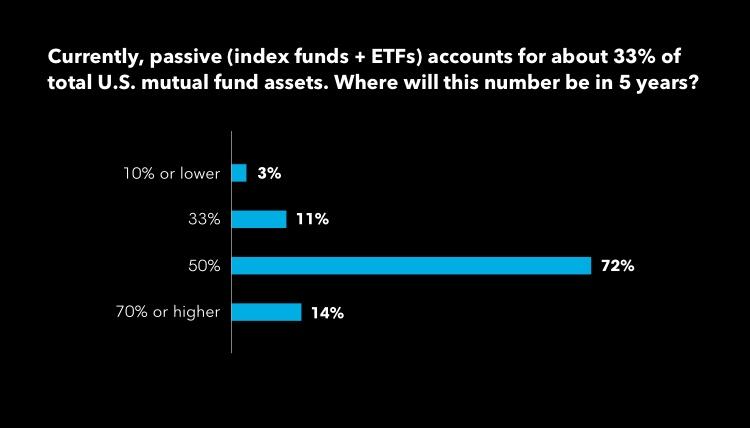

This trend is likely to continue. Passive funds currently make up around 33% of total U.S. mutual fund assets, but when asked where this figure would be in five years, a whopping 72% of attendees at Bloomberg’s inaugural Buy-Side Week 2017 New York event in early June said passive would command 50% of assets by then. On the low end, that’s another couple of trillion dollars. But there are a number of other factors at work than just mediocre returns in exchange for high fees.

First, the environment of the past decade has favored passive funds because of extremely low volatility that has made it much more difficult for a manager to generate true alpha. Even if a manager does guess right, in a low-volatility world, he or she will struggle to deliver much versus a benchmark.

But that environment is changing. Interest rates are rising again and a host of crisis-era responses like ZIRP and QE are being phased out. The next five years are likely to see tighter monetary policy and greater volatility, meaning they are likely to be better for active managers than the last five. “In a more normal environment, the entire equation shifts,” said Jonathan Golub, Chief Equity Strategist for RBC Capital Markets. “Value stocks, small-caps, and international stocks will do better. We could be entering a period in which active kills benchmarks.”

Another important point is the broad price deflation that has afflicted a range of industries, not just asset management. This “great cost migration” exists in the broader economy and has been the mother of all trends since the crisis. It overshadows the active versus passive debate, with even low-cost passive losing assets to lower-cost passive.

“The whole active versus passive debate is arguing about the wrong thing,” added Memani. “The debate should be about whether certain active managers can deliver value or not. If they can deliver value, the market will gravitate to them...otherwise flows would be going only to passive funds. But they’re not - actives that have been able to outperform or deliver value, have been able to gather assets.”

Thus the challenge for active managers is three-fold. They have to manage, at least for now, in a low-volatility environment that discourages wide return dispersions, deliver value significantly higher than the price they charge, and do it in the context of a highly price-sensitive consumer. Those that do can expect to attract assets.

A third factor behind the scenes is whether active managers pursuing esoteric or sophisticated strategies in less-efficient parts of the market are more valuable. “Passive replication of a model or asset allocation strategy with a low-cost ETF or index fund is easily possible in deeply liquid areas like large cap equities,” explained Memani, “but not in all areas, like bank loans or emerging markets.”

However, it may not be so simple. Assets have increasingly flowed to passive products designed with specific purposes in mind, instead of strategies. “The growth in passive assets is increasingly goal-driven, not structure-driven,” countered Jim Rowley, Senior Investment Strategist for Vanguard Investment Strategy Group. “They aim for a solution, like principle protection or a retirement date, instead of trying to beat some benchmark by 100 basis points.”

“The active industry did a disservice by teaching the investing world that the only value of an active manager is beating a benchmark,” Rowley continued. “The real growth in assets is in solutions-based products. For these investors, whether they use active or passive is more of an implementation issue, not a philosophical one.”

For now, the debate continues. “It’s a fact of life - low cost beats high cost,” Rowley declared in a statement that is certain to make active managers twitch. “And every basis point in fee means one less basis point of return.”