Cost control is only one axis of response for asset managers challenged by the Fee Gap.

Cost control is only one axis of response for asset managers challenged by the Fee Gap. The survey also asked what diversification strategies managers expect to use to maximise return and/or minimise risk.

Some of the anticipated strategies are unsurprising and may largely reflect a macroeconomic environment transitioning from an era defined by quantitative easing and rates at the zero bound, to one in which interest rates are rising – however slowly.

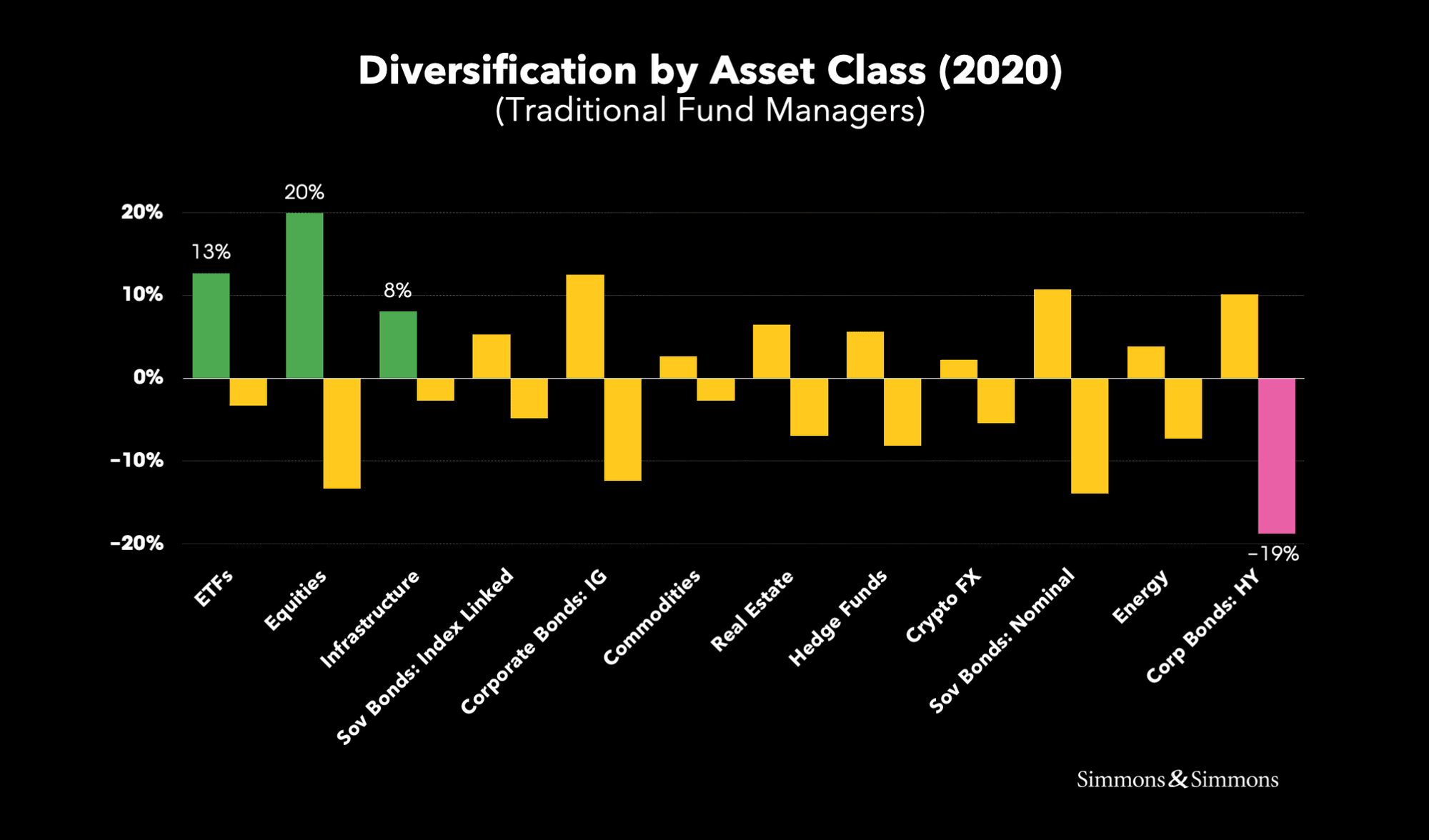

Traditional fund managers expect to move from interest-rate sensitive asset classes/types, such as Sovereign and Corporate (HY) Bonds, into Equities and the long-term demand pull of Infrastructure.

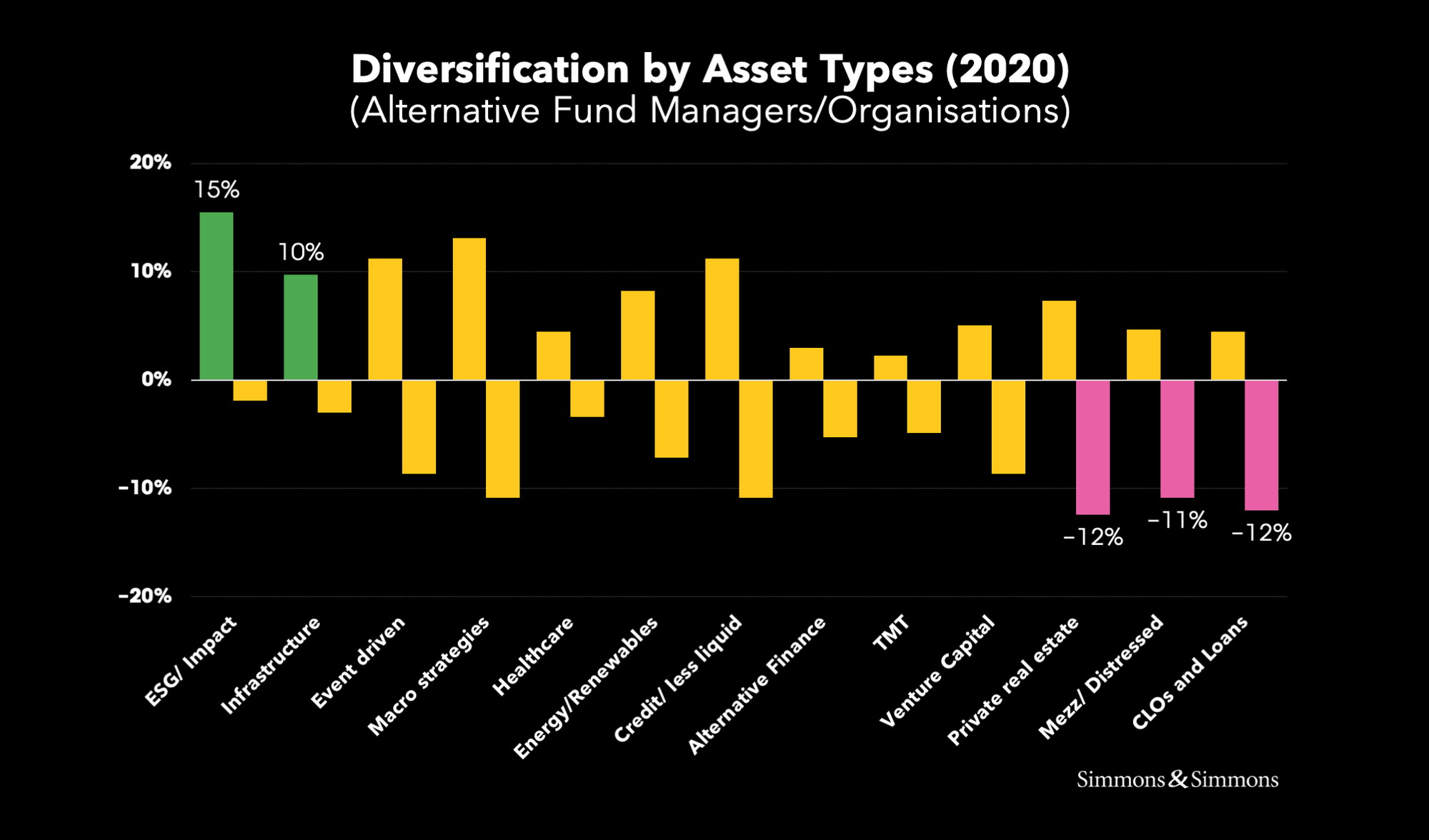

Similarly, alternative fund managers anticipate a move from CLOs/Loans, Mezzanine/Distressed Debt and Private Real Estate into ESG/Impact Investing and (private market) Infrastructure.

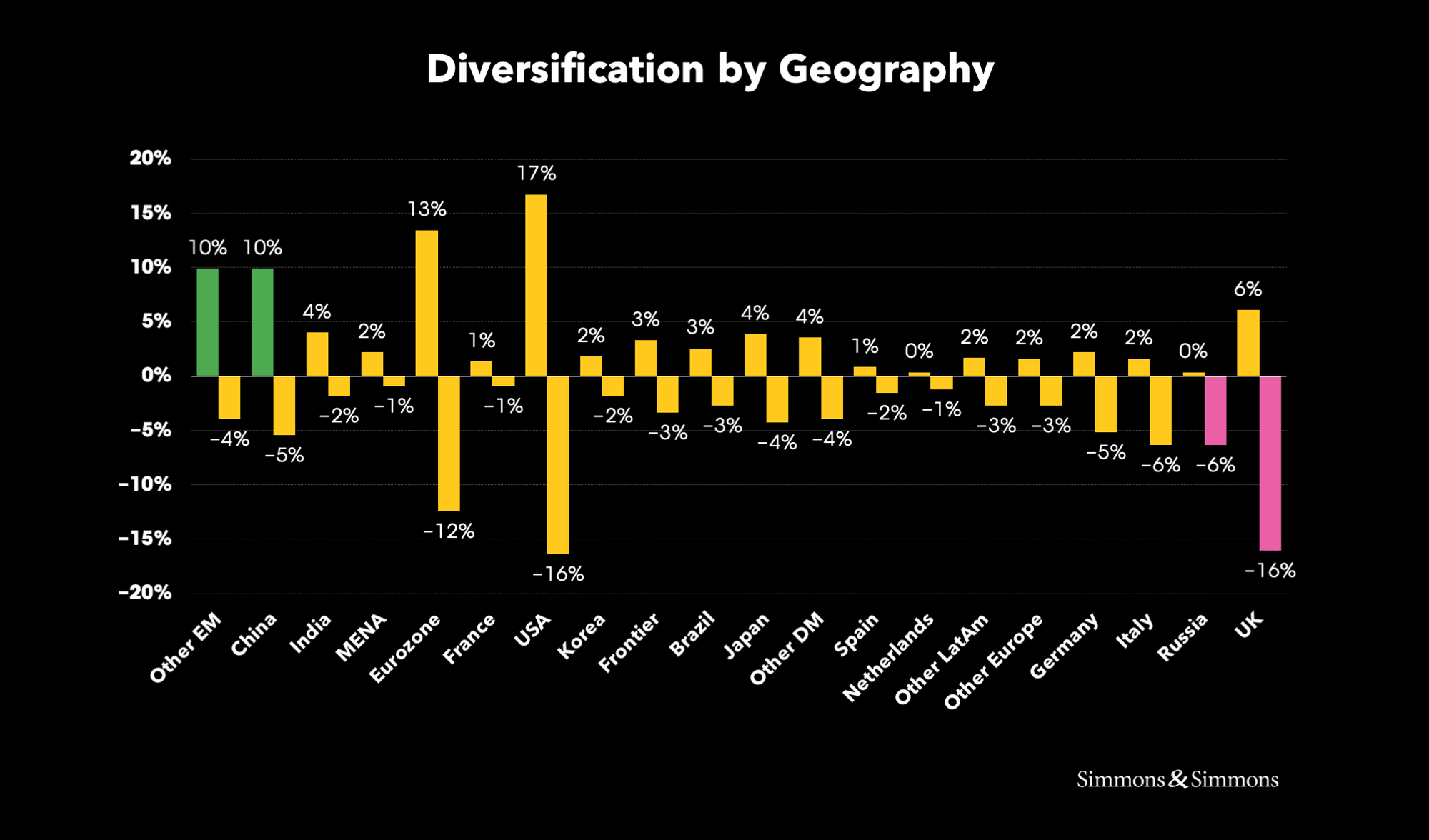

The biggest increases in exposure were expected to favour China and Other Emerging Markets, funded by reductions in exposure to Russia and – by quite some margin – the UK as international concern over Brexit mounts.

While those moves may be unsurprising given the rate cycle and geopolitics, two other diversification strategies suggested that more significant structural change lies ahead.

Investment style

Asked about Investment Style, respondents expected the biggest change to be a shift from passive to active investing. In itself that may not be a surprise: active management holds the promise of higher fees and as long as managers are truly able to demonstrate superior returns, their underlying clients will accept those higher charges.

The surprise comes from juxtaposing this response with the earlier one showing that traditional managers expect their biggest increase by asset class to be into ETFs – traditionally associated with passive investment.

Reading across to other results in the survey, it may be that the increases in investment in New Technology, Big Data, Quants and Alternative/Big Data tell a story of an industry seeking to find new, cost-efficient ways to generate excess return for investors. By using lower-cost collective vehicles to minimise stock-specific risk, it appears managers can justify using passive instruments as part of a broader active strategy.

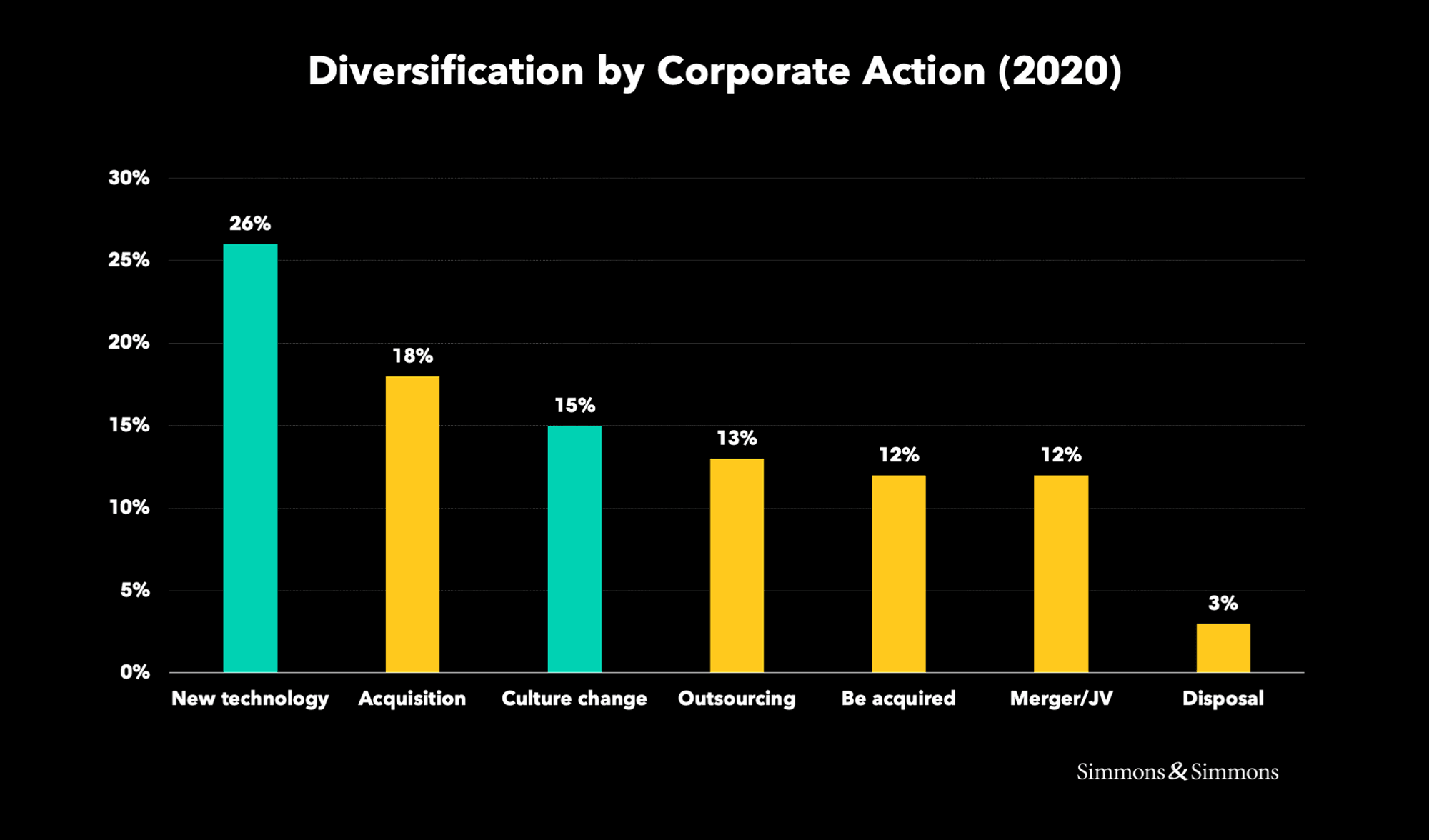

In the second of the more structural changes, almost 60% of respondents, of all types, cited different types of M&A as their most likely diversification strategy involving Corporate Action. Only 40% cited changes brought about by internal reorganisation.

It may be that the bias towards M&A, including the 12% of the sample who expect to Be Acquired, is a fitting coda to the broad narrative arc of our survey. It started with observations about falling savings rates and went on to identify lower growth rates than previous surveys and a Fee Gap, as AUM conversion to fee income becomes ever harder.

In any mature industry, consolidation through M&A is a typical feature. Our survey suggests that we have crossed that threshold and are likely to see an acceleration of the consolidation trend over the next few years with new, more agile and tech-savvy players harrying the more established leviathans.

Investment strategies: Active ETF management the big winner

The landscape of Asset Management 2025 is likely to feature much more active management using ETFs (thus reducing stock-specific risk) allowing more quant-based thematically-driven investment strategies. One of the biggest changes to investment style, reported above, is the move from passive back to active fund management. Undoubtedly that is motivated at least in part by the perception that active management allows higher fee tariffs to be charged, helping close the the Fee Gap. While that move may not be greatly surprising (the lure of higher margin) respondents also told us they expected ETFs to see one of the biggest increases in the share of their future asset mix. ETFs have traditionally been treated (wrongly according to some asset managers) as a tool of (lower cost) passive fund management. Our survey suggests a significant shift in that perception as asset managers seek the best of both worlds: the higher fees of active management coupled to the lower cost of ETFs likely to produce a boost in profit margins. The survey also reveals a desire by traditional fund organisations to expand offerings into alternative (unconstrained) investments in a bid to capture higher fees and boost overall margins.

However, the net impact is clearly expected to be negative for fee margin (respondents expect fees as a proportion of AUM to drop 11% from recent levels by 2025) and asset managers report that they anticipate being asked to do more with less. The drive to lower costs will continue and managers will increasingly seek to reduce costs through the active use of passive structures and algorithmic strategies.

Expectations of modest AUM and a declining fee margin led respondents to signal a desire to move into higher margin products. The extent to which this will be possible will be fascinating to watch, given it clashes with the shift into largely commoditized, passive investments that has possibly been the biggest feature of the industry in the past 10 years. However, the intent is clear: to move a greater proportion of AUM into assets that protect against shrinking margins.

One way to achieve this shift back to active management is to tie it to a reversal in the focus on bonds over the past decade. Respondents expect investors to move away from fixed income products (and particularly corporate high yield bonds) and into equities. This suggests a risk parity approach that aligns equities with higher risk bonds as assets that boost portfolio return – the difference being that equities are expected to outperform high yield (or junk) bonds in the coming years. This is a logical expectation in response to the ending of central banks’ accommodative monetary policy and rising bond yields.

If savers rediscover their appetite for equities and other potentially higher return assets, then managers’ ability to charge fees to help generate alpha and mitigate associated volatility should improve.

Respondents expect that long only and relative return strategies will fall out of favor as investors seek better returns from more active investment styles, such as Quant strategies, Long/Short, Alternative, Big Data and Smart Beta. Many of these would involve a return to active management, targeting the generation of performance fees that would improve the asset managers’ margins, albeit that such strategies generally involve a higher cost base.

The survey responses more generally challenge the traditional notion that ETFs are passive investments. Strategies such as smart beta should generate higher fees than typical passive ETFs as investors are paying for innovative fund design in expectation of better returns.

However, other respondents see the development of new automated management technologies – with the continued popularity of smart beta funds or automated quant strategies – as minimizing the industry’s ability to effect margin recovery. Active ETFs are also expected to play a greater role in the asset management industry of 2025 than they do today.

The survey suggests that investors will seek newer, higher-risk investment styles for portions of their investment portfolio to boost returns. But as risk appetite rises often so too does reliance on asset managers for advice on specific investments and portfolio balance.

As well as pure equity funds, managers also cite potential for higher fees in managing infrastructure funds. Infrastructure investment can generate large returns but these are longer-term and less liquid investments, and the underlying assets often carry varied and idiosyncratic risks, including political exposure. As investors diversify into areas such as this, asset managers who make successful moves should be able to offset the margin erosion from AUM allocated to more ‘plain vanilla’ investments. ESG investments are also expected to rise as incoming individual investors, notably Millennials, seek these types of sustainable and ethical investments, and investment rules for many institutional investors become increasingly strict.

The alternative investment styles that respondents expect to become less popular with clients are Mezzanine and Distressed Debt, CLOs and Loans, and Private Real Estate. These investments are all interest-rate sensitive and so a migration away from them is a logical expectation. The shift away from real estate is also worth highlighting given the importance that this asset class has typically played in portfolio construction.

All these anticipated changes seem to be in line with expectations for global growth and the rotation away from bonds as the global interest rate environment moves into a hiking cycle. However, the addition of risk (particularly equities) does increase AUM sensitivity to a global growth slowdown – which perhaps explains why respondents cited lower growth as one of the biggest downside risks to future industry performance.

The survey reveals that the best opportunity for new AUM with strong margins may lie in the organic penetration of new products and geographies. Respondents expect to change their investment strategies with regards to geographic exposure. Brexit appears to be driving investments away from UK risk, with 16% of respondents expecting to decrease exposure to this jurisdiction. Meanwhile China and other emerging markets are the most commonly cited beneficiaries of expected flows as respondents diversify the geographical exposure of AUM.

This is in line with other findings in the survey that show investors expect to take a moderately higher (if nuanced) risk-on approach to asset allocation over the next several years.

The planned increase in exposure towards Chinese assets contrasts with the stable expected increase in allocation to the U.S. This suggests that investors are sanguine about the longer-term risks of the trade war rhetoric even while respondents cite those trade tensions as one of the most negative global factors for AUM growth.

The survey also finds that, as well as seeking geographic diversification, respondents expect to differentiate themselves in the market through organic growth into new asset classes. Organic growth into innovative risks will generate a premium for asset managers who can bring new ideas to clients – be it by geography, investment strategy, the underlying assets, or a combination of all three.

Fees and other factors

The survey reveals that, for investors in Europe, regulatory pressure is the biggest factor affecting margins: 34% of respondents think that regulation has a positive impact on transparency (good for underlying clients), while 25% say that it has a negative impact on fee income.

Asset managers expect to be impacted by two tiers of regulation in regard to pricing transparency. At the EU level, MiFID II and PRIIPs rules introduce greater disclosure requirements for all fees within bundled offerings, including transaction costs. At the UK level, the FCA plans to improve disclosure on costs, charges and performance fees to enhance product comparability. Combined, these two tiers could see asset managers having to reduce costs or cut low performing products, or even change strategies (for example, committing to fewer trades).

These new regulations will also generate added compliance costs for asset managers – further pressuring profitability.

Interestingly, the potential for increased costs coming from recent equal pay legislation isn’t seen as one of the main likely drivers of increased costs. Equal pay legislation wasn’t even rated one of asset managers’ top People Issues, let alone a leading cause of cost and margin risks. This despite the fact that government-mandated disclosures this year revealed the asset management industry has a wider gender-pay gap than the national average: 28.5% (with a 55.4% bonus gap) compared to the national average of 9.7%.