While AUM often gets the headlines, the real drivers of asset management profitability are fees and costs.

While AUM often gets the headlines, the real drivers of asset management profitability are fees and costs. As noted in the Executive Summary, despite relatively strong expectations for top-line growth (21% growth in global AUM by 2025), fee income is expected to grow more slowly (rising by only 8% over the same period). That implies further falls in the fee margin (fees as a percentage of AUM), which survey respondents imply will fall by 11% of their recent value by 2025.

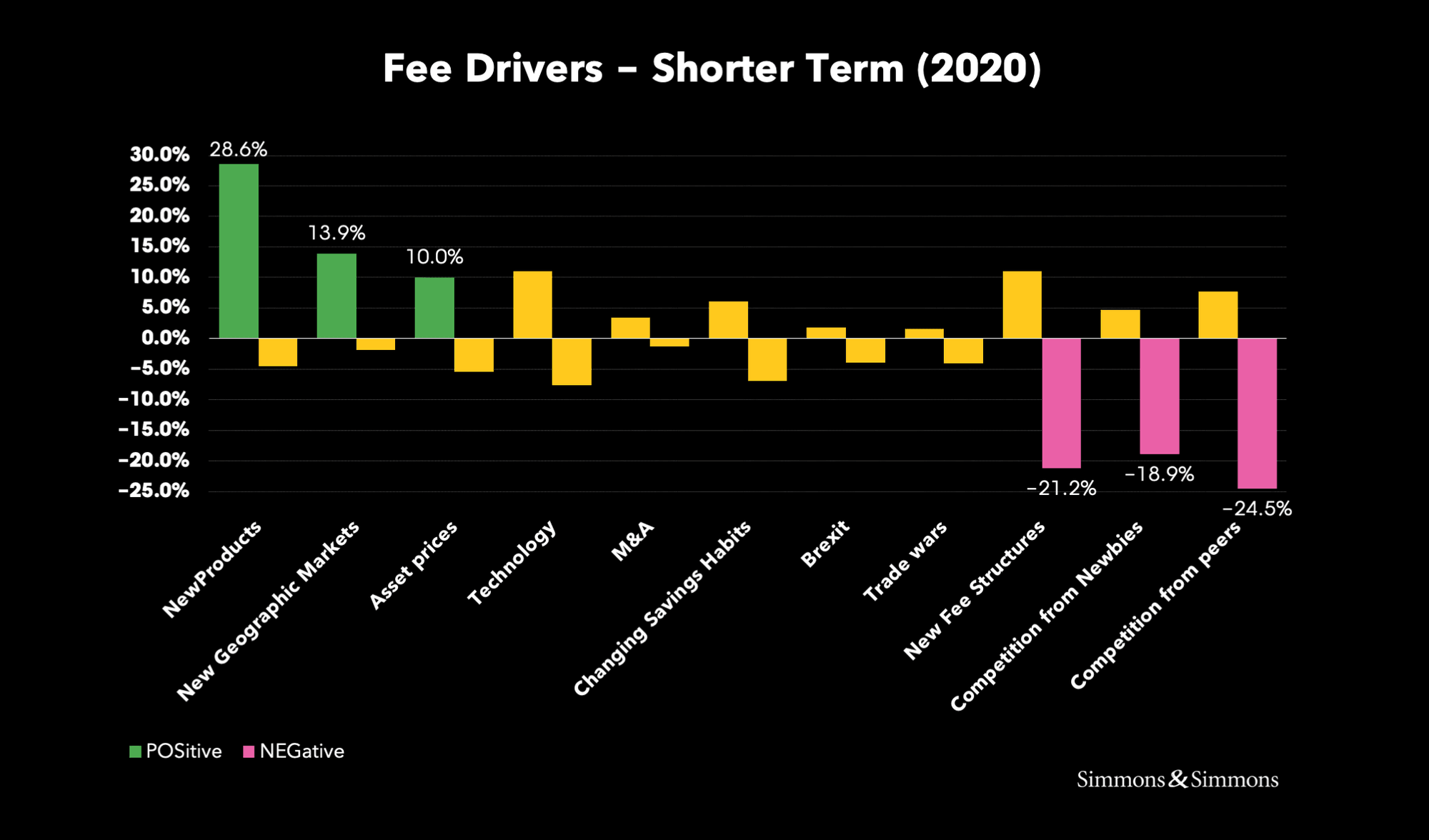

Respondents were asked to identify their key positive and negative drivers of fee income over the short term to 2020.

On the upside, largely in line with the drivers of AUM, they cited expected benefits from the introduction of New Products and entry to New Geographic Markets. Perhaps surprisingly, they also pinned hope on rising Asset Prices – presumably for the boost to AUM and thus AUM-based fee income tariffs. Given recent uncertainties in market behaviour in response to geopolitical and secular macroeconomic changes, that hope may be found wanting over the short term.

Indeed, respondents cited New Fee Structures among their top three downside factors: a possible reality check for those hoping that rising asset prices will drive income growth. The impact of Competition – both from existing competitors and new entrants – was cited as the biggest factor squeezing profits, confirming the pessimistic, but perhaps realistic, view that market competition will intensify and lead to a further competitive reduction in fee income.