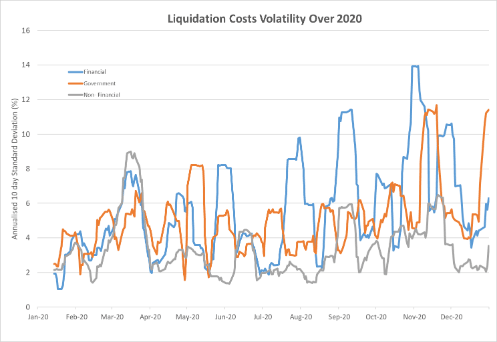

The COVID-19 pandemic is changing how risk is perceived globally. Market and Credit risk remain in focus across the industry, however liquidity risk metrics supporting the execution of trading strategies have once again fallen into the spotlight since the pandemic up-ended the apple cart in March 2020. To better understand the market impact of these unprecedented events, we analyzed liquidity in the fixed income market through 2020 using Bloomberg’s award-winning LQA market liquidity analytics.

A year for the books

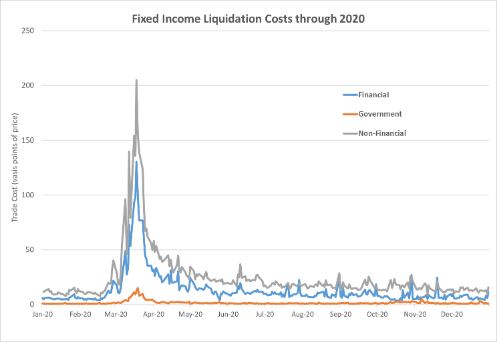

Prior to the global outbreak of the coronavirus, average liquidation costs for fixed income securities were generally low; under 15 basis points for most issues. As the virus spread, risk premia increased markedly, in many sectors liquidation costs increased by a factor of 10x. As expected, government bonds benefited from a flight to quality, while both Financial and Non-Financial sectors exhibited significant increases in liquidation costs. In particular, the Basic Goods, Consumer Cyclicals and Energy sectors experienced some of the largest increases in liquidation cost.