Part two

Having established that automation is here to stay, the next section will investigate the issues surrounding implementation and the watertight risk management strategies firms use to avoid bad trades and mitigate risk.

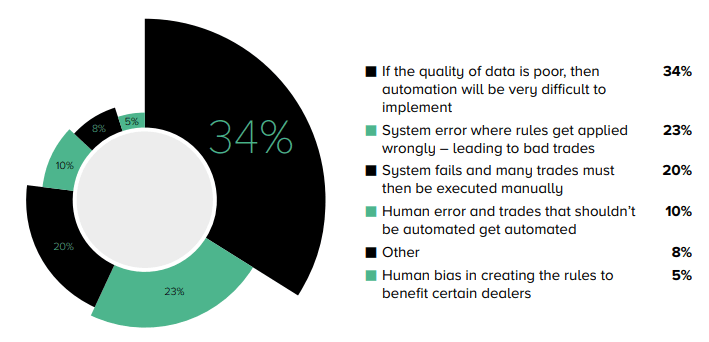

Our survey data found that the main concern for traders was poor data, which puts firms at risk of making bad trading decisions that could affect best execution and ultimately see the end-investor taking a hit. For the European fixed income trading industry, it’s evident from our survey results that data quality is the main area of concern when it comes to implementation issues. In contrast, in the U.S. traders were first focused on human and system errors when asked about their concerns with implementation. With the European trader more focused on the quality of reliable data, a potential outcome could be greater post-trade transparency.

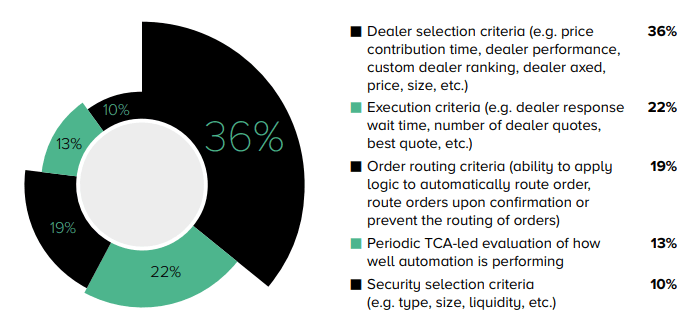

When it comes to implementation issues for automation technology, according to our survey, the highest priority for a trader is dealer selection criteria, e.g. price contribution time, measuring dealer performance, custom dealer ranking, dealer axed price and more.

These concerns arise because a huge part of a fixed income trader’s responsibilities is to know where the liquidity sits and which dealers are performing in any given sector based on experience. All are crucial to achieving the best results for a firm’s clients.

If the right teams within the fragmented markets of fixed income trading are collaborating with vendors in the implementation process to pool their collective knowledge, then this can be incorporated into a firm’s automation technology strategy to provide solutions to any potential issues.

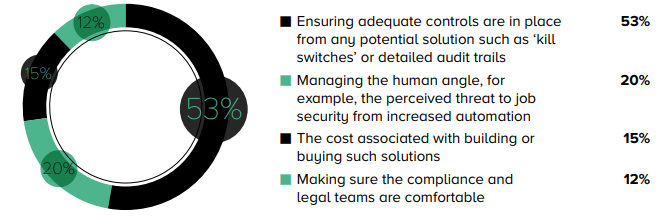

Our survey results found that the main obstacle fixed income traders saw for implementing automated technology was ensuring that adequate controls are in place – from kill switches to audit trails. This was followed by managing human error, the costs involved with building or procuring these solutions and ensuring that compliance and legal teams were also able to use the technology correctly and efficiently to optimise their trading desk.

Before implementing any automation, clean data is a prerequisite. This is a new style of trading for fixed income and all steps should be taken carefully.

– Carl James, Global Head of Fixed Income Trading, Pictet Asset Management

The worst case scenario for firms using bad data would be bad decisions that impact best execution and ultimately the end-investor. This is why the data being used must undergo stringent analysis, and firms must have a keen grasp on the inputs and model used to generate any derived values.

– Ravi Sawhney, Global Head of Trade Automation and Analytics, Bloomberg L.P.

It is interesting that in Europe the main concern is data quality. When U.S. managers were asked the same question, the primary concerns were either system or human errors. This may be an indication that Europe could benefit from greater post-trade transparency or a centralised trade tape.

– Alex Sedgwick, Market Structure and Electronic Trading Consultant, Fincisive Strategies

“There are plans for mitigating risk, such as working on data applicability by getting rid of unnecessary duplication and working more on the functionality of the scripts. These would draw out more productive statistics with the available data.”

“Using an AI-powered data classification tool that can operate with a large amount of data within minutes and provide data that’s required, storing the rest and running other tests on it to make it useful in other regions of the organisation.”

“No system can operate without a backup to the primary system. If a trade fails, the system should push it into the back end where it can be reviewed either manually or through another set of automations so that it can re-enter the system to be completed.”

“We’ve clearly marked our rules to prevent bias, although this does present a viable threat that would damage our reputation. Our strategic position is based on regulating the workflow so that there are no special allowances for a specific dealer.”

“We are looking at similar data, whether preference is a single source or multiple sources actioned, based on the level of automation intended. We are yet to make level considerations in this matter.”

The roles that remain in the operating model of the future will be high impact. Traders, and PMs, daily responsibilities will shift from doing the operational work to maintaining a relative value ranking list that feeds the automated process. Put another way, they are responsible for overseeing the automation each and every day and ensuring that it is achieving what it is intended to.

– Chris E. Wrazen, Head of Bond Indexing, Europe, Vanguard Asset Management Ltd

We can mitigate the main risks of automation by keeping control of the process. Aiming for a ‘one touch’ execution approach, rather than end-to-end automation, means the trader is fully in control and aware of what’s being processed. Coupled with that, traders should be intimately aware of the automation logic so there are no surprises in the results.

– Sam Knight, Trader, Fidelity International

It makes sense that dealer selection is chosen as the most important criteria. Selecting the right dealer still means a deep partnership, even if an AI is making this decision for you. It’s still crucial to have the right partners.

– David Bullen, Director, Lorgwood Ltd.

Understanding where liquidity sits, which dealers are performant in a given sector based on actual experience and who is ‘axed’ to trade at the moment of triggering a request-for-quote are all critical factors to achieving best execution for a firm’s underlying clients. To avoid human bias, you need to be working with other traders on their desk where there is overlap in what they trade, using actual trading data to drive decision-making and then periodically reviewing the performance of the dealer selection rules. It is also important to review new dealers as they arise and give them a chance to see if they can provide uplift in performance.

– Ravi Sawhney, Global Head of Trade Automation and Analytics, Bloomberg

Unlike equities, fixed income is comprised of several markets each of which has its own structure. This fragmentation may be a limiting factor for some firms because it requires teams with a breadth and depth of knowledge to implement a technology strategy. However, this shouldn’t be a deterrent: best practices can be imported from other asset classes – while the solutions may not be exactly the same, thematically the opportunities are the same.

It is critical to have a set of parameters built into the automation that are driven by the hierarchy of best execution factors highlighted in the organisation’s desk procedures.

“We’re channeling our resources based on our current strategies, which have provided reliable assets in themselves. We are encountering additional options day by day, but still in the process of registering these changes within the trading framework.”

“We have achieved a good acceptance rate when it comes to new asset classes, but limited ones ensure proper focus on each and deeper relative studies that have better applicability.”

“At present, we are not prepared enough to keep adding asset classes at speed. Rather, our focus point would be based on our expertise, both with manual input and automation innovation.”

“Our interest lies in more controllable sectors for long-term growth prospects. The necessity for new asset class inclusions is derived by leveraging available data and gauging all market considerations in detail.”

“If we automate equity operations, we could save a lot on operational costs and this would also allow us to introduce automated compliance to intensify the accuracy of our trading activity.”

“We are breaking away from the traditional activities and researching new alternative asset classes that only run on automated platforms. This will help us to operate with sophisticated portfolios that only need monitoring and it does the rest by itself.”

Proper monitoring and emergency protocols are easy when using Bloomberg Rules Builder. The challenge will be advancing this as automation takes off and you have to factor in volatility in the markets, which the machine may have never seen before. Volatility does not mean automation is turned off, it just requires a more careful control by the trader through the periods of turbulence. This works in the same way that the pilot of a modern airliner has ‘hands-on control’ for take-off (start of day) and landing (close of day), but during cruise (intraday), their hands will only ever take over from the autopilot where situations present themselves that take the machine out if its comfort zone. Over time, the machines can learn to spot patterns as to what triggers the trader to take over, and what they do in those situations such that it can improve its own autopiloting skills.

Respondents are likely to be looking through the prism of trading, so the risk controls make sense. However, from a wider perspective, we would see other answers getting higher scores. A CTO will see things differently to a CIO. As this style of trading is utilised by early adopters, it will become more usual in all firms’ trading offerings.

There’s a temptation to jump right in and solve problems in a one-off fashion as you react to frustrations in your day-to-day operations. It’s critical to add a step in your process where these items are collected and reviewed holistically, rather than just prioritised, to ensure that the way they are solved fits with the bigger picture. If the automated operating model of the future is a puzzle, the solution to each of these problems are the pieces. You have to pay close attention to all their shapes and how they fit together.

The main obstacle we have is systematically identifying orders that are suitable candidates for automated execution. Orders that are sent to market with little chance of being executed create information leakage and have a detrimental effect on overall execution quality.

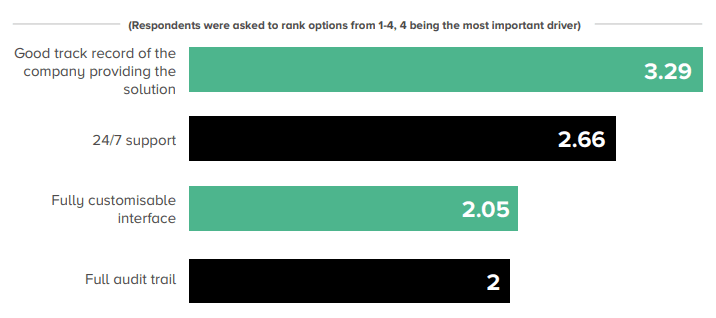

Traders can establish whether a vendor has a good track record based on historical interactions, peer feedback and the number of clients using the product.

From a build/infrastructure perspective, establishing a good track record would be the job of IT. From a trading performance perspective, the dealers already have this data and can assess the broker before automation and do a compare and contrast.

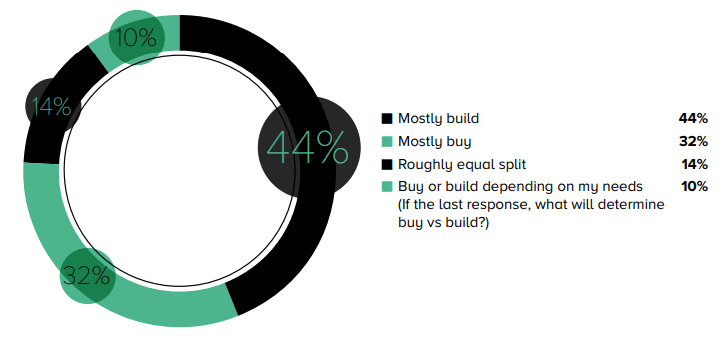

Very often, building tech will cost more than firms budget for, as they underestimate the ongoing support costs.

Our automated operating model will likely be a combination of purchased technologies/services and data sources that fit together with our proprietary trading applications.

We believe successful trading automation can give us a competitive advantage. We will focus on building the decision making technology in-house, but utilise third-party products for data and to connect to markets.

We will buy the base system and build the rest to customise it and make it a secure system without external participation.

Buying will depend on the quality of talent and skill the provider holds to support us post-integration.

Having a vendor create this system for us will be easier for us so that we have a wider range of expertise on the system. We will continue receiving support as and when required.

An equal mix of buying and building activity will be undertaken in the near future. This process will need our expertise to create a blueprint or strategy that will be followed in the system-building process so that execution and inclusion of the system will be smooth.