These fast-growing investments had less than $1 billion in issuance when they arrived in 2008 but quickly gained momentum, finishing their first decade with exponential growth in 2016 followed by more than $170 billion issued in 2017.

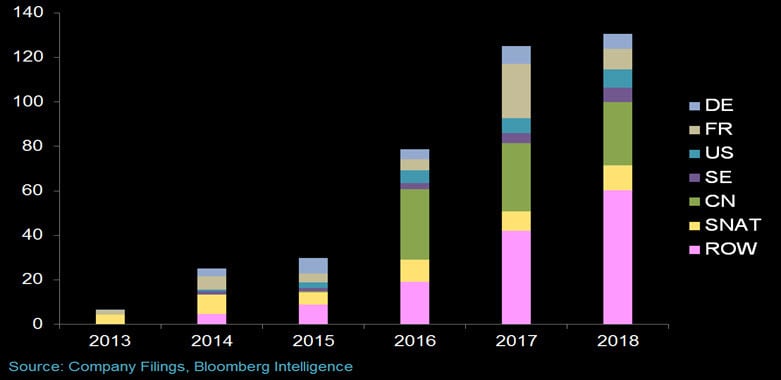

As a result, many predicted another record year for green bonds in 2018, but gains were modest. Bloomberg Intelligence saw issuance rise from $125 billion in 2017 to $130 billion in 2018. The question the buy side needs answered is whether this easing is a pause in the action or the start of a longer plateau.

Green bond basics

Green bonds are pegged to a specific environmental or sustainability goal. They typically finance projects for environmentally friendly infrastructure, energy efficiency and clean energy, allowing issuers to reach investors with specific environmental concerns and giving buyers a way to fulfill mandates for socially responsible investments.

A quick snapshot of the market: The three major regions for green bond issuance are Europe, the U.S. and Asia-Pacific. Most green bonds are euro-denominated, representing an equivalent of $157 billion, or 43 percent of outstanding green bonds worldwide, while 24 percent are dollar-denominated and 17 percent are yuan-denominated. Interestingly, most green bonds held by investment managers are dollar-denominated — $18.2 billion, or 42 percent of the amount managed — which may be due to better liquidity. Evidence also suggests green bonds denominated in dollars trade at a noticeable premium compared with regular bonds vs. euro-denominated securities.

Of course, green bonds still represent a very small portion of the fixed income market — about half a percent of all issues in 2018. For the sake of comparison, the U.S. issued approximately $8 trillion in new debt securities in 2017.

Green bond issuance by country ($bn)*

Understanding the slowdown

Slower growth in 2018 is due primarily to a $27.5 billion decline in run rate by Chinese and French issuers. New entrants are active, including aggregate offerings of $11.9 billion by issuers in Belgium, Ireland, Indonesia, Luxembourg and Portugal. These new contributions would look more significant, however, without the massive $16 billion (equivalent) issue by France in 2017. Without that single issue, new entrants would have easily offset the Chinese and French decline.

*This figure captures the issuance of green bonds as defined and recorded by Bloomberg Intelligence.

At the same time, growth in issuance from outside the traditional base of countries (China, France, the U.S., Germany and Sweden) is strong, representing nearly 50 percent of the green bond market. This share is up from just 24 percent in 2016.

Short break or permanent vacation?

Here are five factors to watch for in 2019 to help determine whether the green bond market will return to its recent strong growth trend.

1. More global issuers. Continued growth in the number of issuers could signify that the market’s longer-term growth trend remains strong. New issuers like Belgium and Ireland will need to continue to come to the market, picking up the slack in what could be a permanent slowdown in Chinese offerings. Right now, the breadth of the issuer base is indeed growing. Investors can select from 10 out of 11 industry sectors in 45 countries. Issuers of over $100 million reached 314 last year, up from 236 in 2017 and 134 in 2016.

2. Consistent labeling. If the 2018 decline in Chinese green bond offerings points toward a longer downturn, it may indicate investors are becoming wary of whether some green bonds are truly green. China, for example, still uses these bonds to back “clean coal” projects, drawing criticism from environmental activists. This problem is not unique to China. The Climate Bonds Initiative is a de facto gatekeeper for the market, offering the option for green bond issuers to verify adherence to their principles. But many issuers choose not to and they are under no obligation to ensure that their projects meet specific standards for environmental impact. The lack of consistent classification criteria is also why different research providers have varying estimates for annual issuance.

3. More government issuance. For green bonds to move from the billions to the trillions, governments in Europe, the U.S. and Asia-Pacific will need to intervene. Generally speaking, there are three paths to follow: incentivizing growth, mandating growth or leading by example. If governments step up, green bonds could follow a path similar to that of clean energy a decade ago. At that time, governments used these same strategies, including subsidies and minimum renewable energy sales requirements of utilities, to help the market thrive.

4. U.S. utilities come on strong. One reason why the U.S. lags behind European countries in green bonds is the lack of issuance by non-municipal government agencies. Utilities dominate corporate green bonds in the U.S. and Europe, representing nearly 40 percent of total issuance. But while the total amount of utility bonds outstanding is equivalent (just under $570 billion), these bonds account for 8 percent of the market in Western Europe — but only 1.4 percent in the U.S.

5. No European slowdown. Market maturity combined with wider volatility may suppress growth in euro green-bond sales, following two years during which issuance more than tripled. At the same time, other green financing options, including loans or securitizations, may get more attention. Together, all of these factors could make it difficult for European green bonds to maintain their pace of growth in 2019.

Interested in learning more about how Bloomberg can support you in this area?

BloombergNEF (BNEF)'s Sustainable Finance coverage spans the Why (policy and frameworks), the What (strategic opportunities) and the Who (strategic landscape). We help you understand the regulatory environment and government incentives, the options available for access to capital to finance sustainability initiatives, and the opportunities for investors, financial services and corporations in the evolving sustainable finance landscape.

BloombergNEF (BNEF), Bloomberg’s primary research service, covers clean energy, advanced transport, digital industry, innovative materials and commodities. We help corporate strategy, finance and policy professionals navigate change and generate opportunities with a team of experts spread across six continents.

Contact BNEF to find out more from one of our specialists.