Right now, passive mutual funds and exchange-traded funds (ETFs) that buy U.S. equities hold 48 percent of assets and are expected to top 50 percent soon. It’s a dramatic rise for passive investments, which represented only 20 percent of retail equity flows as recently as 2007. These trends hold globally. In Asia, 47.6 percent of assets are in passive equity funds. In Europe, index funds have grown from 13.2 percent of equity AUM in 2007 to a third of equity AUM in 2018.

It is clear why passive funds are seeing such strong growth. They typically offer more transparency and far lower fees than active funds. They have tax advantages, using buy-and-hold strategies that minimize capital gains taxes. They can also quickly capitalize on sectors with trending appeal, such as cannabis, vegan food or video games, which active funds can’t replicate as easily.

Most critically, passives have delivered better returns due to strong U.S. equity market performance. Passives are designed to match the market, whereas large-cap funds failed to outperform the S&P 500 benchmark more than 92 percent of the time from 2001 to 2016. Mid- and small-cap funds did even worse, and even large-cap value funds did not hit their benchmark 78.5 percent of the time.

As a result, retail and institutional investors alike have enthusiastically embraced passives. This is not welcome news for the buy side, for a variety of reasons. Increased passive AUM delivers limited revenue to asset managers. Passive assets represented $16 trillion in total, or 20 percent of all AUM in 2017, but produced revenues of just $17 billion, or 6 percent of the industry total. On top of this, active fund managers are under more pressure to lower fees, reducing revenues even further.

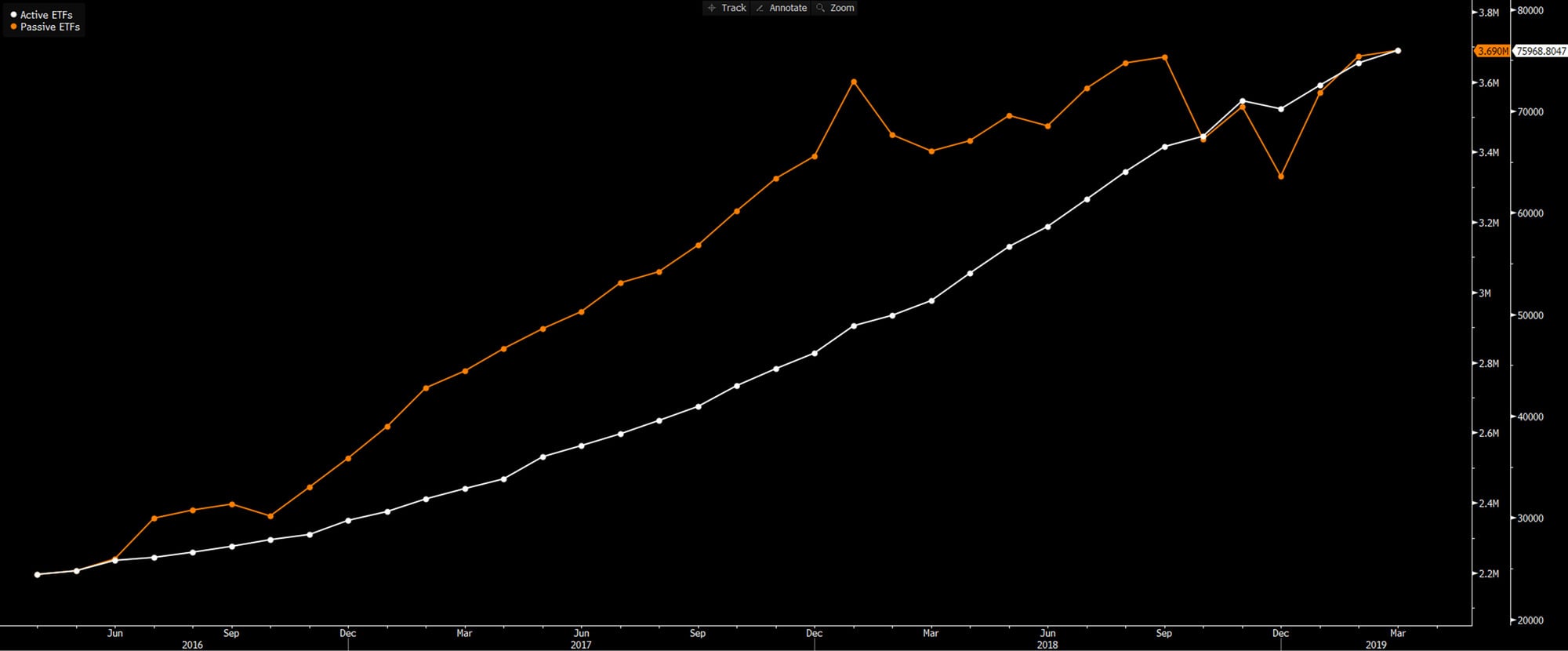

Active vs Passive ETF flows based in USD (US market only)

Obstacles to passives

Like all other investments, passives have shortcomings. Keep in mind that while passive funds are adding market share, their flows for 2018 fell short of their record-setting contributions of $700 billion in 2017.

One potential drag on passives is increased competition — spurred by their popularity — in a space where it is difficult to differentiate except by reducing prices. Fees for passives are already very low, but PwC predicts they will go lower, declining 20 percent or more to reach 0.12 percent by 2025. In fact, some passive managers have dropped their fees to zero to ward off competition. This does not mean fees are disappearing. Rather, zero-fee funds may be used to attract investors and then cross-sell other products and services, including active strategies in ETF wrappers that do have fees. These dynamics give an advantage to larger players that can scale enough to reduce margins and still maintain profitability.

Another potential barrier for passives is the risk of becoming top-heavy because most index funds are market-cap-weighted. This well-known risk has given rise to a subgroup of passives called smart beta.

The threat of smart beta

Smart beta mutual funds and ETFs combine passive index tracking with an active, rules-based component that increases diversification by weighting on specific factors such as value, growth or momentum.

Smart beta is still a relatively small category with $430 billion in AUM or 0.5 percent of the global total. But it has grown 30 percent a year since 2012 and Boston Consulting Group believes these products “pose a substantial threat to traditional active players—potentially even greater than that of the overall shift to passives.” The reason: smart beta attempts to produce active management results at lower costs.

The smart beta space itself is growing in diversity with the introduction of multi-factor funds, which offer exposure to more than one factor. Adding to the complexity is the reality that not all funds define factors in exactly the same way.

“What I like about factor funds is they are rule-based, so you know exactly how they are constructed and rebalanced,” says Lars Kalbreier, CIO, Vontobel Wealth Management. “Having said that, if you use the name ‘value’ you will see people have different understandings of what value is. It’s very important not to buy any value ETF or value index fund without looking at how it is built. You will see big discrepancies in value products.”

Whether you are an active or a passive manager, Bloomberg Indices offers a fresh perspective on the traditional world of indexing, providing comprehensive solutions to fulfill their benchmarking needs, including Bloomberg Barclays Indices, BCOM Commodity Indices, Strategy Indices, AusBond Indices and more.

Learn more about Bloomberg Indices.

Another issue that affects smart beta growth is the split between “authentic” or “pure” factor ETFs that use academic research, concentrated portfolios, high turnover and, at times, short positions and “watered-down” factor ETFs that dilute factors so much that they deliver market returns. So-called watered-down funds took in $55 billion over the past three years while “pure” value ETFs had almost no inflows.

Vitali Kalesnik, partner, Research Affiliates, explains the difference between pure and watered-down funds with an interesting analogy.

“The difference in these vehicles is like the difference between a motorcycle and a train,” he says. “The motorcycle is a nimble vehicle, and if you know what you’re doing, you can move very quickly from one place to another. But a train is going to be cheaper and more reliable. If you don’t know how to use it, it won’t hurt you. Most people prefer the train.”

Is passive domination inevitable?

Passives overtaking actives is not a given. This isn’t the first time passives were predicted to reach a tipping point. Trends in 2017 pointed to 2018 as the year passives would take over, but it didn’t happen. The end of the bull market in the U.S., should it arrive in 2019, could hamper passive growth. One thing is clear: given the rapidly evolving relationships among passives, actives and smart beta products that fall somewhere in between, the story is likely more complex than a simple choice between one approach or the other.