China's treasury inflows lasted thanks only to index inclusion

Although global investors net added China Treasury bonds again in August, against the headwind of the widening discount in the China-US 10-year Treasury yield gap, this might be driven by passive inflows amid index inclusion by FTSE Russell during this month only. Otherwise, other global investors might still be actively selling China Treasuries. The People's Bank of China (PBOC) might refrain from delivering policies with strong monetary-easing signals in September, to help control market volatility ahead of the Party Congress. Although another surprise policy-rate cut is unlikely, the PBOC could still lower the required-reserve ratio by 25 basis points. On the yuan, the PBOC may be more receptive toward further depreciation in the yuan against the dollar, as long as this is led by a broad dollar rise when the market prices in more Fed hawkishness, with the yuan staying broadly stable against China's trading-partner currencies.

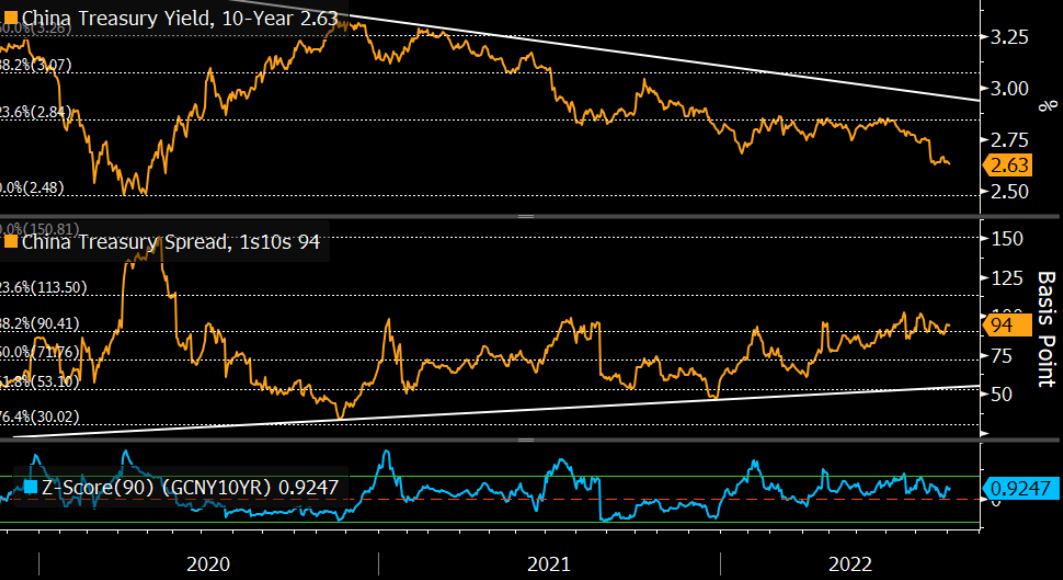

China treasury curve's bull steepening bias intact China's Treasury curve has further bull steepened in early 2H, somewhat in line with our midyear outlook, and this trend might continue until China's slowing economy starts to return signs of stabilization. For instance, there has to be progress in containing the Covid resurgence and hence rising likelihood of lockdowns loosening, which could then facilitate transmission of existing fiscal and monetary support. An anticipation of macro recovery would also ease rate-cut expectations and might back a higher 10-year yield. Furthermore, rising credit demand could tighten interbank liquidity and cause the Treasury curve to switch to a bear steepening or flattening trend.

Technical analysis: China treasury bond curve

Source: Bloomberg Intelligence

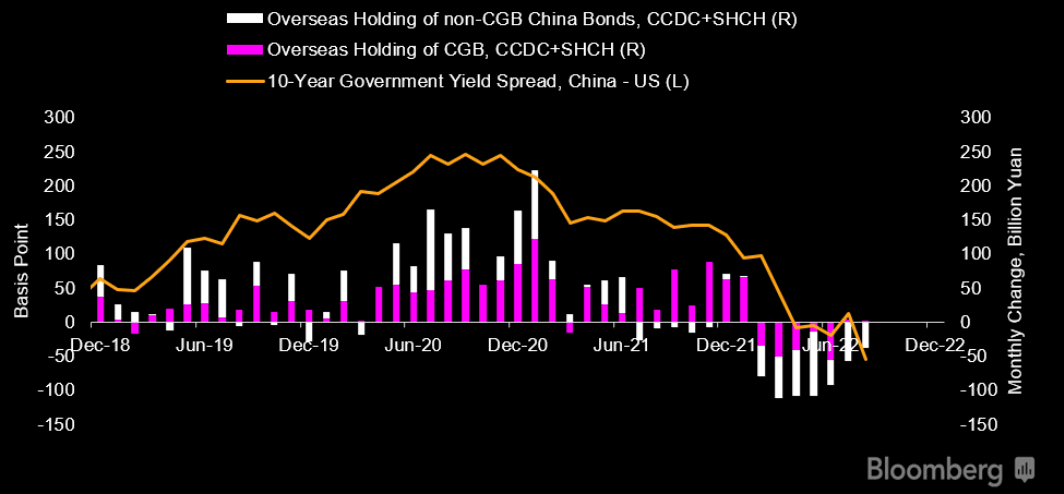

CGB-UST yield gap: Index inclusion might have eased active selling Global holdings of China Treasury bonds (CGBs) rose 2.3 billion yuan in August, another rise after holdings fell for five straight months before July. That said, deducting estimated passive CGB inflows due to FTSE Russell index inclusion, other overseas investors might have actively trimmed CGBs in August. According to the factsheets, the CGB's share in the World Government Bond Index (WGBI) rose by 0.33 percentage point to 2.47% in August and this might imply 56.1 to 68.2 billion yuan of inflows, based on the original assumption that index inclusion could lift the CGB's share in the WGBI to 5.25% over 36 months starting from October 2021. The wider discount in the China-US 10-year Treasury yield gap might have prompted active outflows.

Global investors' share of CGB holdings fell again to the lowest in 20 months, at 9.8%.

China bond flows vs. China-US yield spread

Source: CCDC, SHCH, Bloomberg Intelligence

PBOC FX RRR cut might not stop yuan's drop toward 7 per dollar

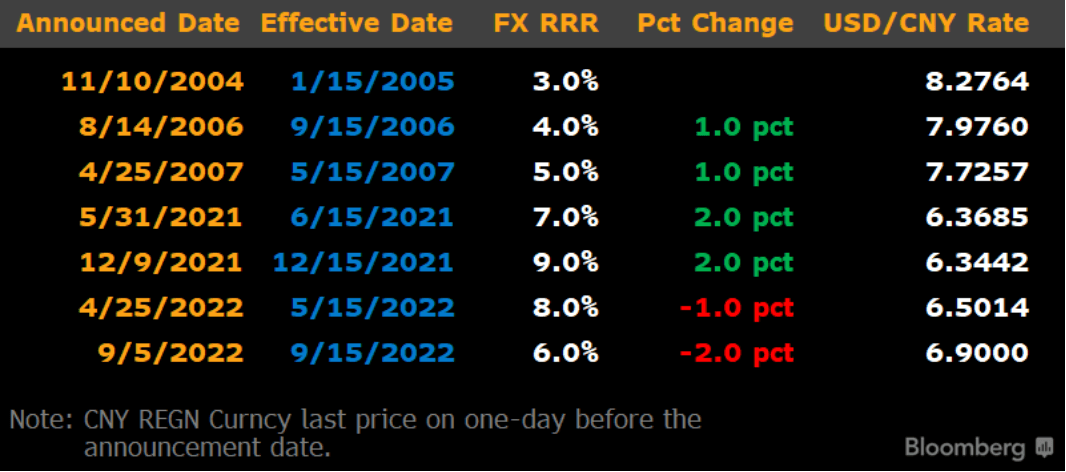

The People's Bank of China latest announcement to lower the reserve-requirement ratio of financial institutions' foreign currency deposits (FX RRR) from 8% to 6%, effective on Sept. 15, might at best slow the yuan's drop in the near term but should not reverse its original direction, judging from previous experiences. The yuan might continue to drop toward 7 per dollar this year if the Fed persists with its hawkishness and China's macro slowdown continues, let alone factoring in escalation in cross-Strait uncertainties. The PBOC may announce additional policies, like charging yuan shorts via onshore FX forwards or draining offshore yuan liquidity, if the yuan continues to weaken against a basket of currencies.

The latest cut might release $19.1 billion of liquidity, according to end-July FX deposits data.

History of PBOC FX reserve-requirement ratio

Source: PBOC, Bloomberg Intelligence

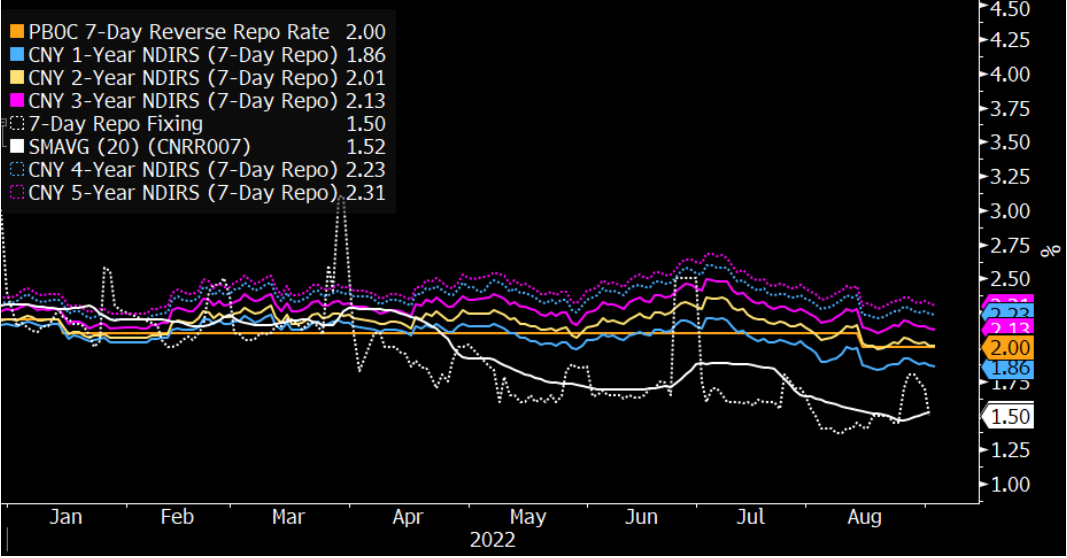

NDIRS: Yuan swap receivers' carry backing tapers

Although receiving positions in offshore non-deliverable interest-rate swaps (NDIRS) based on the seven-day repo rate still offered positive carry and rolldown as of Sept. 5, tenors below three years now offer relatively low carry compared to a month ago after the surprise PBOC rate cut in August. In particular, the one-year and two-year tenors are trading below the 7-day reverse repo rate of 2%, and the PBOC may be increasingly unlikely to rely on policy-rate cuts to revitalize its slowing economy. Therefore, rates traders might opt to square their receiving positions or convert them into a bear-flattening spread using the one-year swap as the front leg.

Please refer to the CARY <GO> function for the carry and rolldown analysis of various interest-rate swaps.

Seven-day repo NDIRS vs. PBOC reverse repo

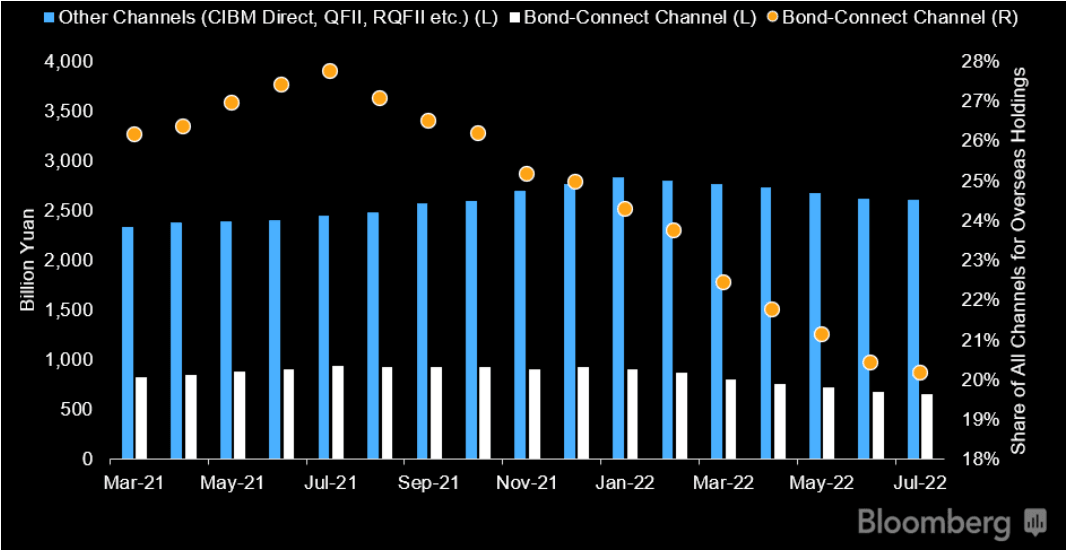

Bond Connect holdings ink record low again

Overseas investors' holdings of China bonds at CCDC via the northbound Bond Connect channel further dropped to 20.10% in August, the lowest in the 18 months since CCDC started reporting the data, from 20.15% in July. Nonetheless, average daily turnover rose to 34 billion yuan from 32.9 billion yuan in July, and trading tickets also rose to 7,185 from 6,798, according to data from the Bond Connect website.

Bond Connect Company Limited and China Foreign Exchange Trade System jointly launched the Northbound primary service for China Interbank Bond Market (CIBM) on July 4; the service allows offshore investors to participate in the subscription of CIBM new issuances.

Overseas investors bond holdings by channel