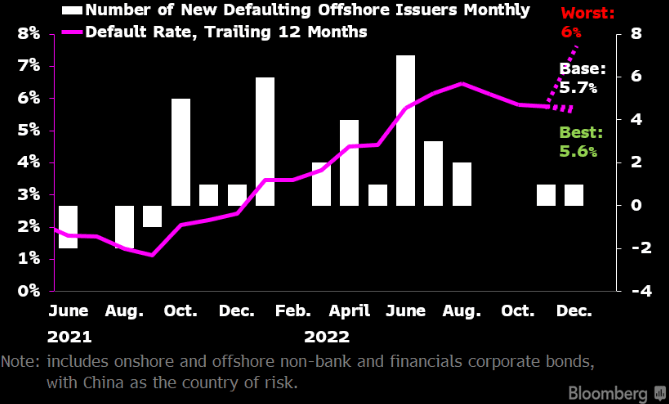

China's default rate could further improve in December

China's offshore trailing 12-month default rate might further drop to 5.72% from the current 5.75% in our base case, assuming one of the 594 issuers misses an interest or principal payment in December. The dollar-bond market has established a trend of improvement in the number of new defaulting issuers in the last five months. The number of new defaulting issuers dropped to 1.2 per month on average in the recent five months compared to 2.25 per month, based on the trailing 12-month trend. Although this trend was driven by the base effect (i.e. fewer surviving issuers), rather than an improvement in credit fundamentals, we expect this could continue.

Looking further into 1H23, the default-rate trend hinges on the effectiveness of policy support from the government's 16-point plan when refinancing demand increases.

U.S. dollar issuer-based default distribution

BI default rate scenario

China's Default Rate Could Further Improve in December

The dollar-bond default rate has dropped for the third consecutive month since September to 5.75%. China's latest 16-point plan to rescue property developers could spur new fundraising in equity and domestic bond markets and cap bond defaults in 2023. One caveat is that November's default rate could be revised to 5.92% as we wait for an update from CIFI after the issuer was reported to miss its 2025 dollar-note interest payment by the grace period on Nov. 19.

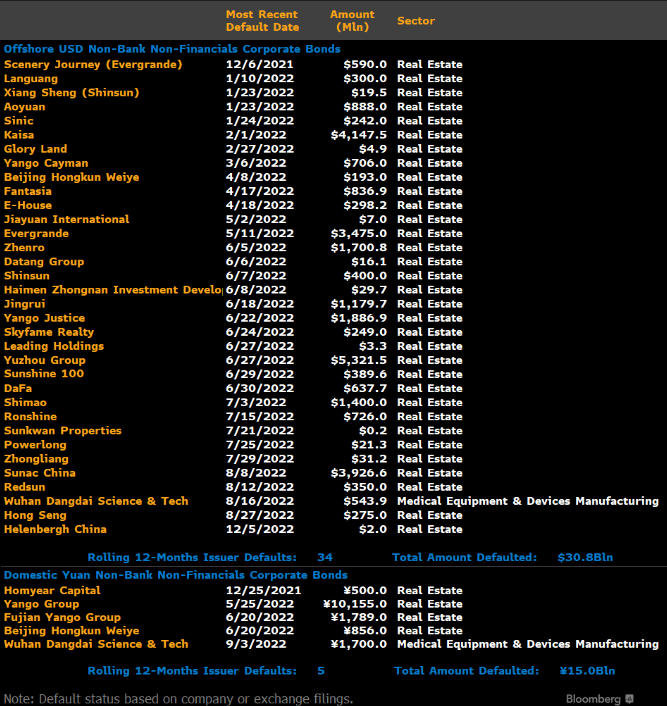

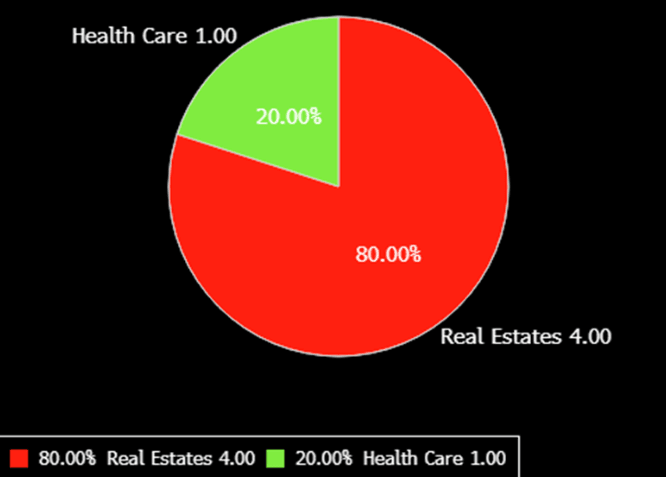

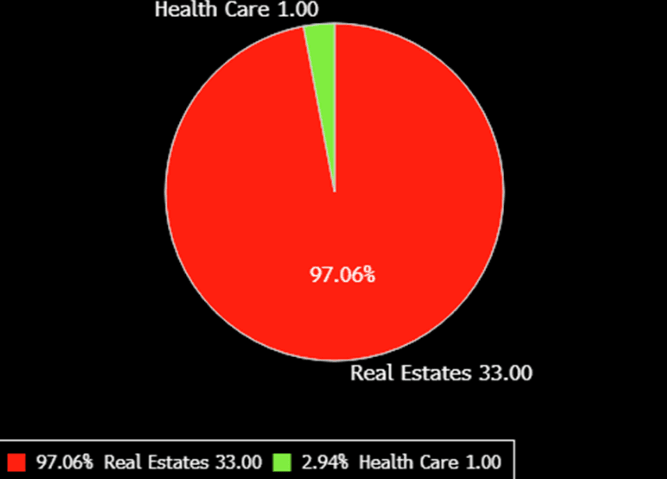

As of Nov. 30, trailing 12-month default volume marked $30.8 billion with 15 billion yuan ($2.1 billion) of domestic bond defaults, based on bond amounts outstanding, involving 34 offshore dollar issuers and five domestic yuan issuers. -- Jason Lee

Rolling 12-month defaults as of Nov. 30

Chinese yuan issuer-based default distribution

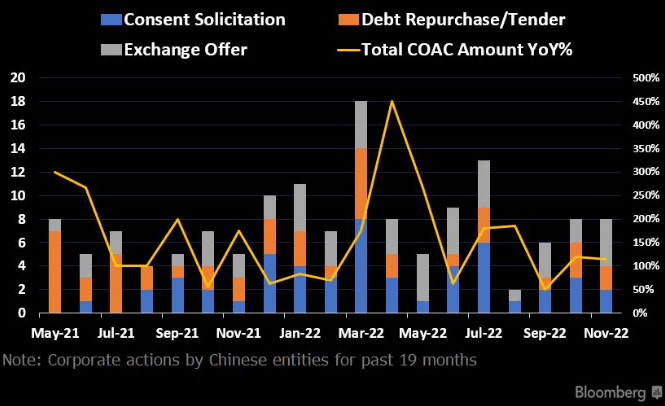

This was the third month in a row that Jiayuan executed exchange offers and Helenbergh continued to seek consent for outstanding notes.

The aggregate number of new consent solicitations, tender offers and exchange offers by Chinese issuers remained steady in November from the previous month; exchange offers increased while tender offers and consent solicitations decreased. Beijing State-Owned Assets Management Hong Kong and Pterosaur Capital conducted tender offers for the first time, while RongChangDa Development Ltd. conducted a consent solicitation for the first time in 19 months.

CACT<GO> keeps you updated on all corporate actions.

Corporate actions by chinese issuers

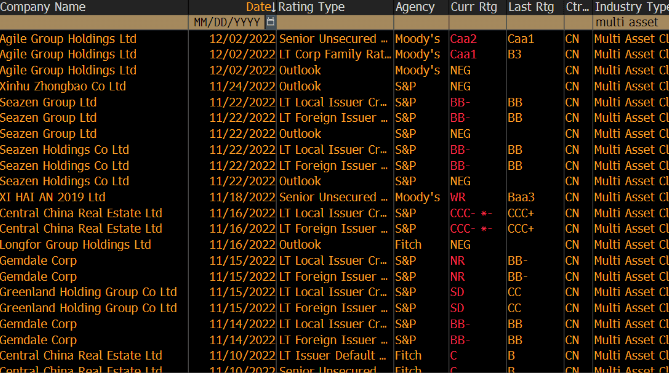

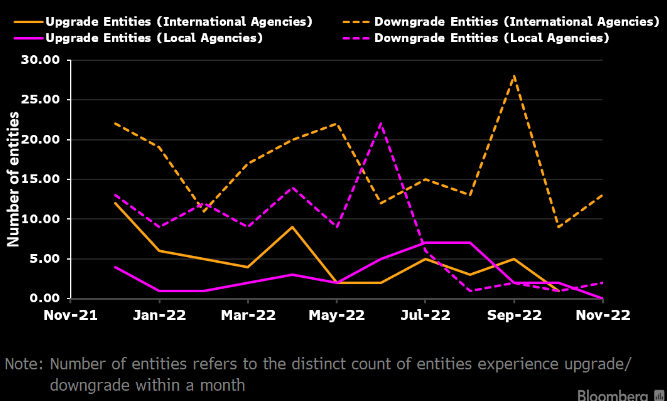

Credit Rating Change: 19 Chinese Issuers Downgraded In November

Rating change: Multi asset class owners and developers

Entities Experiencing Rating Changes

Monthly Dollar-Bond Maturity Shrinks to $7.4 Billion

Refinancing risk arising from maturities in China's corporate-bond markets is decreasing in December compared with previous months, potentially reducing market volatility. 28 non-bank, non-financial dollar-bond issuers face a combined $7.4 billion of principal payments in December, equivalent to 1.3% of the amount outstanding in the market. This is lower than the the $8.4 billion (1.4%) of maturities in the same month last year and $9 billion (1.7%) of maturities in November this year. On a sector level, real-estate issuers have only $810 million of maturities in December, or 0.4% of the sector's total amount outstanding.

Chinese bond market debt maturity profile ($)