Contrarian positioning may start to form in China property space

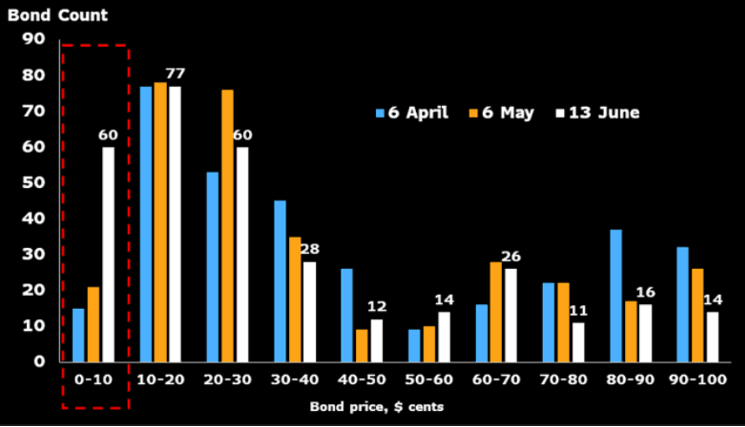

China's property bonds have continued their slump, with the median price dropping to 22 cents from 40 cents in March. As the recovery cannot be calculated using 2021 financial metrics -- several developers haven't released their numbers -- downward pressure on the bonds may persist. This may create contrarian relative-value opportunities.

Overly pessimistic expectations Most property bonds are trading at 10-20 cents, with prices possibly determined by news from developers rather than estimated recovery rates. Several key institutional investors such as UBS and BlackRock have reduced their positions as offshore creditors could be at a disadvantage in any potential recovery, taking into account recent incidents.

Yet for every bond seller, there is a bond buyer. The wide range of prices for the bonds of defaulted developers, from 3 cents to 20 cents, may signal overly pessimistic expectations that they won't recover. It's also possible that some buyers of these distressed bonds view them as similar to options.

Property bonds' distribution curve

Source: Bloomberg Intelligence

Barbell strategy may generate alpha Some recent incidents have raised concerns about the lack of recognition of offshore creditors' seniority and communication with these bondholders. Evergrande prioritized homebuyers over other creditors, Shimao rapidly fell from investment grade to distressed, Zhenro didn't pay the coupon on its bonds as promised, Evergrande Services had cash missing, Logan announced private debt and Sunac repaid onshore bondholders before offshore ones.

With contracted sales gradually recovering, we prefer stronger developers such as Country Garden, CIFI and Seazen. They can be combined with a highly diversified portfolio of low-priced bonds, say below 10 cents, for recovery prospects for a barbell portfolio with potential upside and reasonable carry.

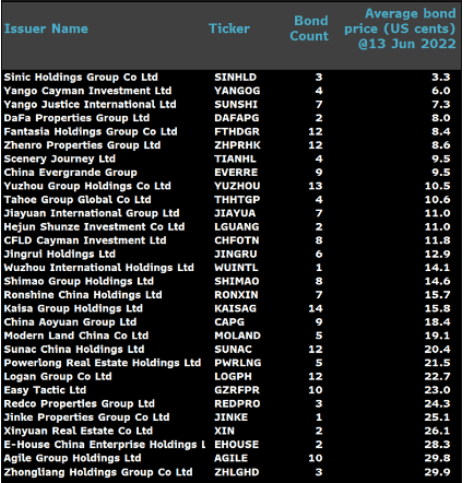

List of bonds trading below 30 cents on the dollar

Catalysts for distressed developers We continue to be cautious about weaker developers as relative value may emerge only when there is greater transparency, a better indication of recovery levels or a strong positive catalyst. Some firms still haven't released 2021 results. Evergrande's restructuring plan, slated to be announced in July and now postponed, could have been a potential catalyst for distressed developers should the offshore-bond recovery come in higher than expected or above the current price. Also, there are reports suggesting that Evergrande's offshore assets -- stakes in its HK-listed companies -- could be paid in kind to bondholders.

China Fortune Land is going through debt restructuring and should the recovery turn out to be higher than the current average bond price of 13 cents, then it could be another catalyst for the distressed sector.

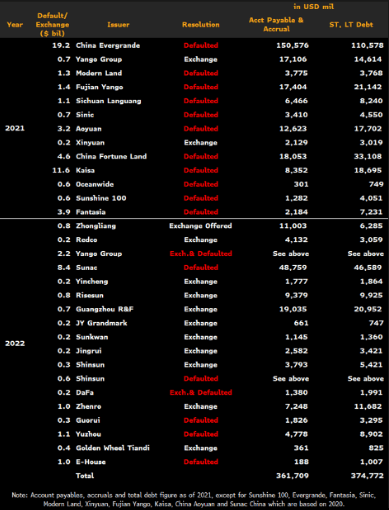

List of exchange offers/Defaulted issuers

Source: Corporate announcements, media reports