China may revive home sales after substantial leverage was likely removed from the system with over 30 developers defaulting or exchanging their offshore notes. It may be nearing the last stage of an adage which describes cycles as: easing leads to disorder, disorder leads to tightening, tightening leads to demise, demise leads to easing again.

Removed leverage may trigger turning point Over $69 billion of offshore notes have defaulted or been exchanged and this doesn't include onshore borrowings, which may or may not need to be restructured, nor does it cover smaller developers' defaults. Several of China's largest developers -- such as Evergrande, Sunac and Shimao -- have already defaulted yet haven't released their 2021 financials, so their total indebtedness is still uncertain.

Previously, President Xi Jinping was concerned about disorderly capital expansion and high leverage in the property sector, with the state implementing the "three red lines" policy. With the latest defaults, the country may potentially be at an inflection point. The next step could be to control fallout from these defaults and revive home sales, which the government has been doing via various policy-easing measures.

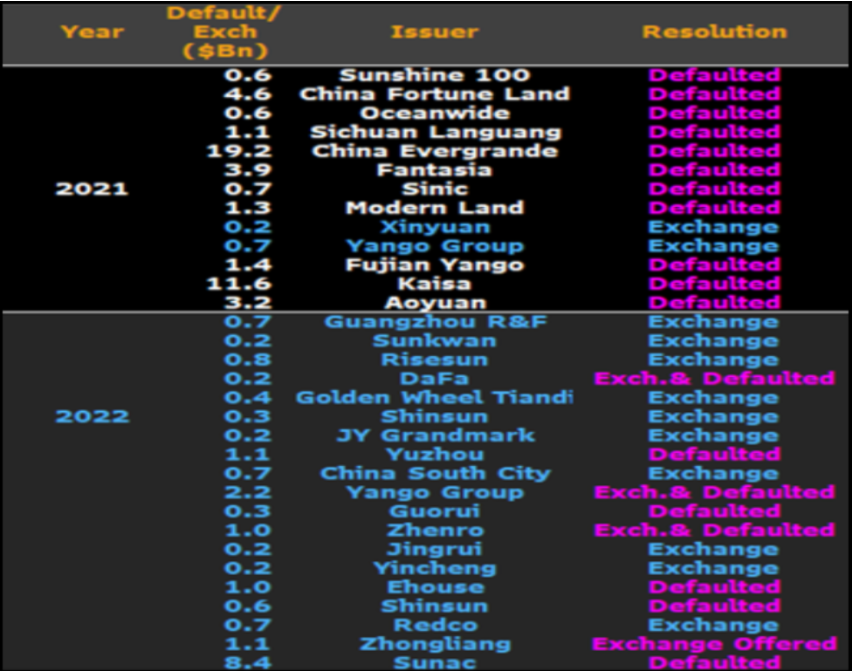

High-yield developers' bond resolutions

Source: Bloomberg Intelligence

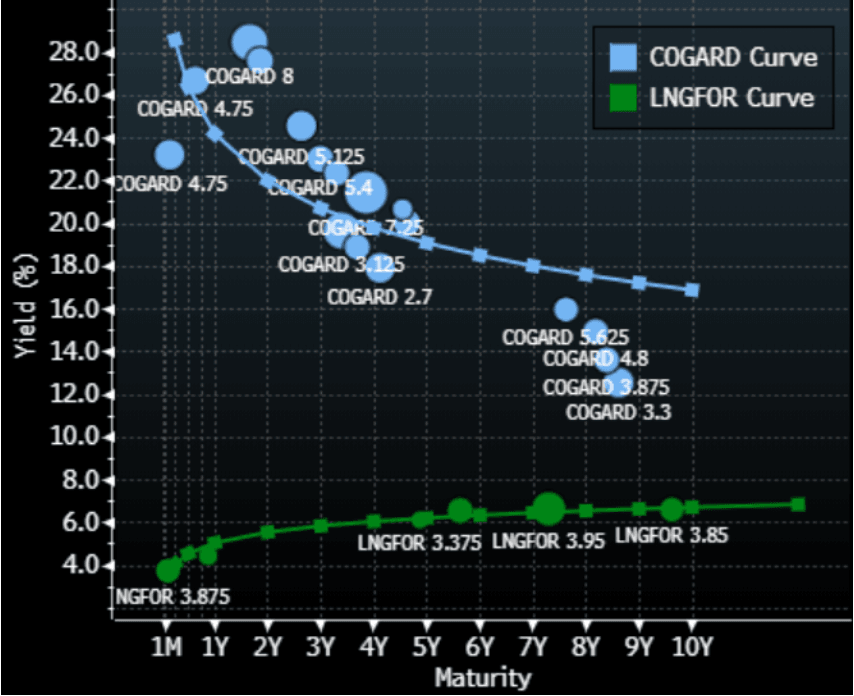

Vicious liquidity cycle could be ending Chinese regulators may have identified sector survivors with their selection of Country Garden, Midea and Longfor to spearhead the issuance of fresh yuan bonds and their encouraging Chinese banks to subscribe to them. This could help shore up their liquidity, boost confidence in the sector and prevent any further fallout. Should this be successfully executed, it could be conceived of as a form of state-backed liquidity.

Longfor doesn't seem to need the extra capital as its 2023 dollar bond is trading close to par. Midea doesn't have dollar bonds outstanding. Whether Country Garden needs onshore issuance is debatable as we previously calculated it can self-generate sufficient liquidity. Nonetheless, boosting its liquidity can only improve its credit profile and may reassure even offshore bondholders.

Yield curves of 'selected' survivors

Key question is scale and use of proceeds The targeted issuance amount for this first stage is only around 2 billion yuan for all three companies which is still relatively small compared to their aggregate total debt of over 580 billion yuan. Yet, should the issuance amount further increase and become a consistent part of these companies' respective funding channels, this could be positive for their long-term operating outlook as they may be able to buy assets cheap in the downturn and possibly become sector consolidators.

Depending on the eventual scale of this new funding channel and the use of proceeds, China could also encourage more M&A in the property sector, as we saw in 2008 in the US with the banks, which may turn out to be positive for offshore bondholders of other defaulted developers.

Draft onshore issuance details

Source: Corporate announcements, media reports