China's dollar-bond default rate may exceed 4.7%.

China's offshore default rate may trend higher from the current level of 4.7%, if at least one of the 580 issuers miss an interest or principal payment. Fifteen face debt-payment tests, according to data compiled by Bloomberg News. In the domestic market, chengtou, or local government financial vehicles, will continue to receive support for new issuances as China goes back to its traditional driver of economic growth, infrastructure investment, with the real-estate sector weakening.

We continue to believe the default rate in real estate will peak in 2H with the relaxation of restrictions on developers' cash holdings, which should help restore investor risk appetite.

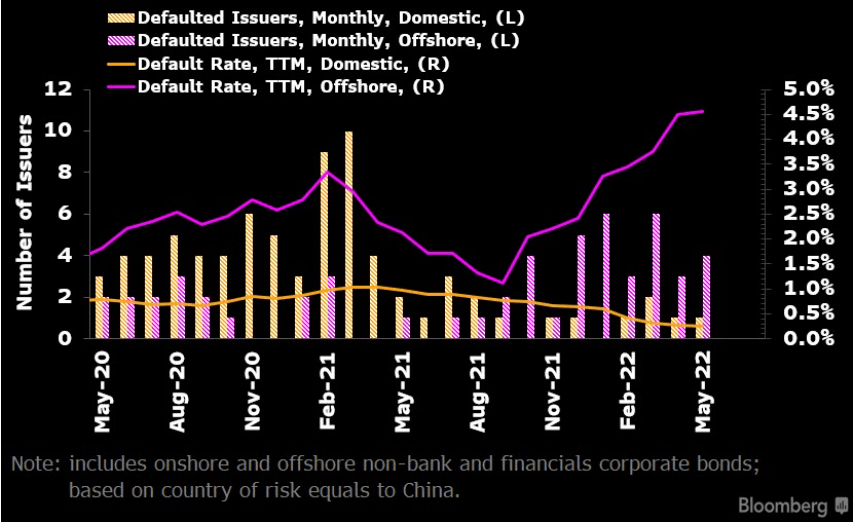

Record-breaking default rate

Source: Bloomberg Quant Platform (BQuant) , Bloomberg Intelligence

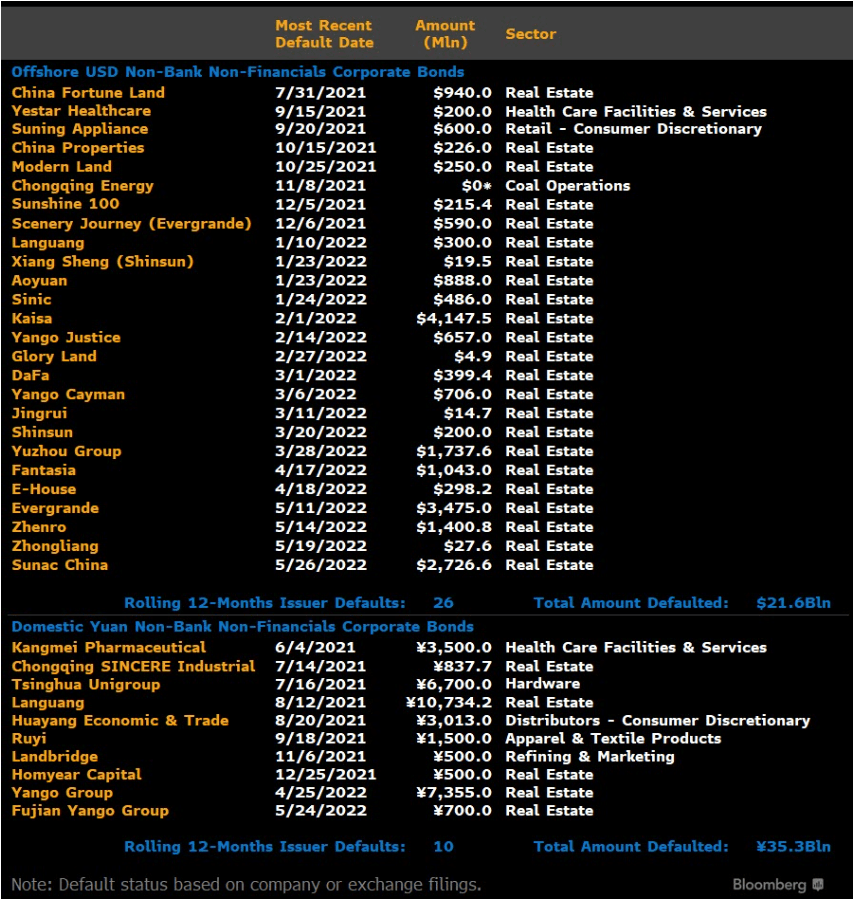

Monthly bond-default data show recent credit events were dominated by the real-estate sector, and we expect the trend will continue. As of May 31, we recorded $21.6 billion of offshore dollar-bond defaults and 35.3 billion yuan ($5.3 billion) of domestic bond defaults based on bond amounts outstanding in the last 12 months, involving 26 offshore dollar issuers and ten domestic yuan issuers. In the dollar-bond market, defaulted bonds issued by 23 real estate firms in the table comprise over 96% of all defaulted bonds.

Kaisa continues to be the largest single defaulting issuer in the offshore market, based on bond amount outstanding, accounting for 19% of the total defaulted amount outstanding in the last 12 months. China Evergrande is the second-largest defaulting issuer, followed by Sunac China.

Rolling 12-month defaults as of May 31

Source: Bloomberg SRCH <GO>, Bloomberg Intelligence

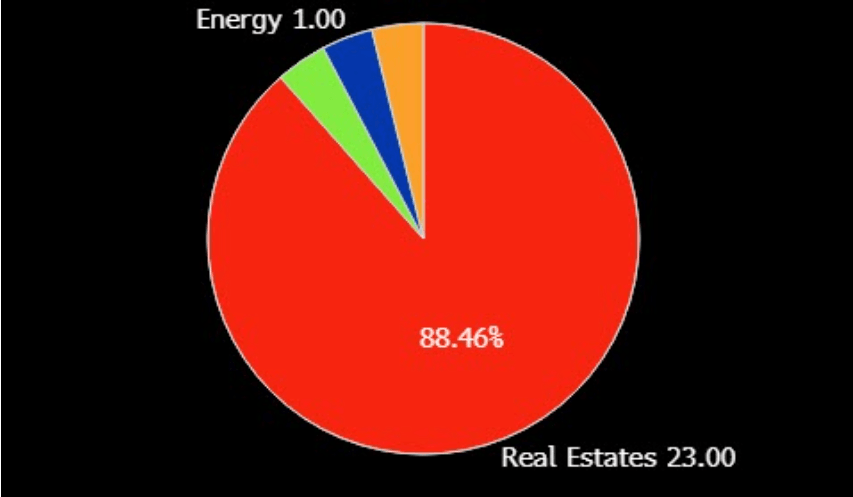

U.S. dollar issuer-based default distribution

Source: Bloomberg Quant Platform (BQuant)

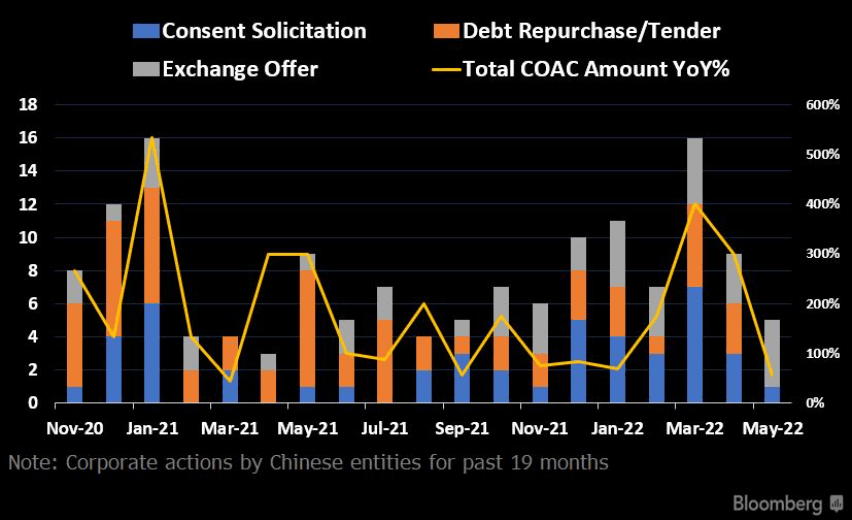

The number of consent solicitations, tender offers and exchange offers by Chinese issuers dropped to a 2022 low. At the same time, the year-on-year corporate action volume is growing at a decreasing rate. It was the first month with no tender offer conducted by the Chinese issuers. Similarly, consent solicitations continued to decrease over the past quarter, making exchange offers the major action conducted. Exchange offers are expected to remain the dominant corporate action that issuers seek based on the current trend.

CACT<GO> keeps you updated on all the corporate actions.

Corporate actions by Chinese issuers

Source: Bloomberg CACT <GO>, Global Data

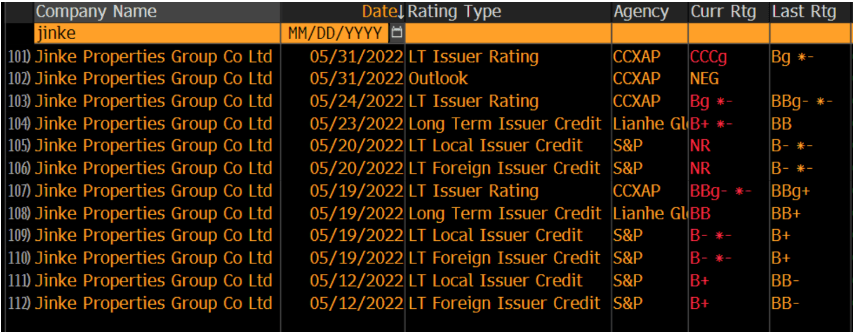

Credit rating change: 48 Chinese issuers were downgraded in May

Rating change: Jinke Properties Group Co

Source: Bloomberg RATC <GO>

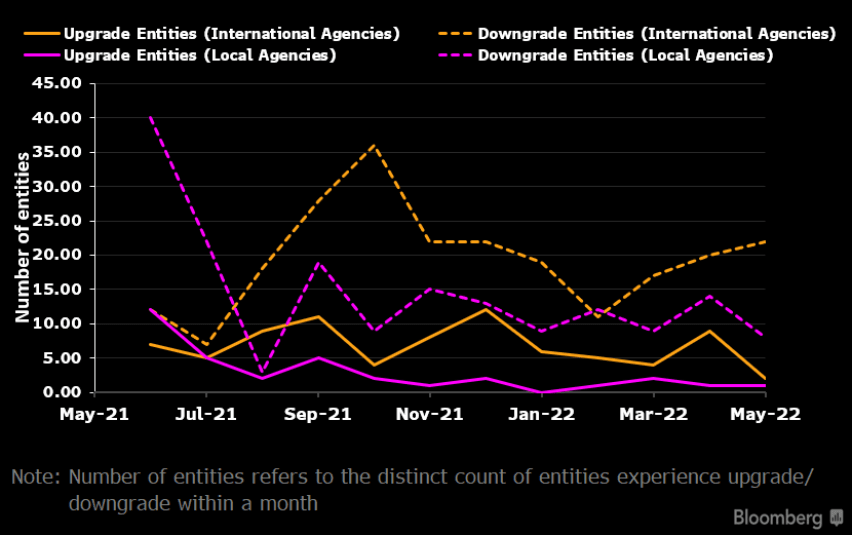

Entities experiencing rating changes

Source: Bloomberg Quant Platform (BQuant), Global Data

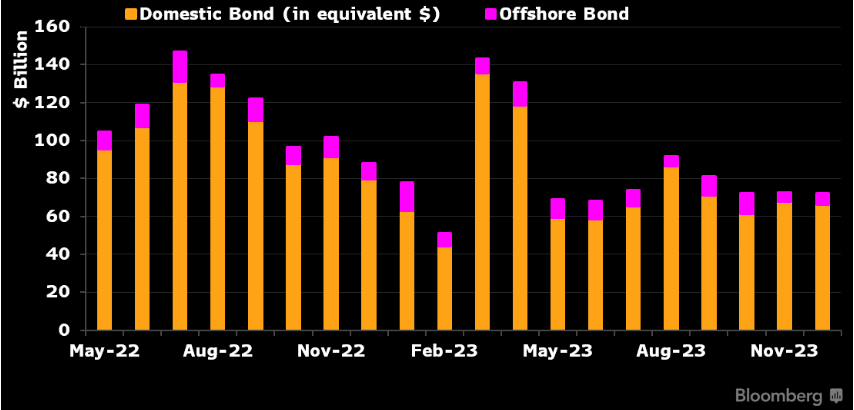

Chinese issuers face $162 billion maturities

Refinancing risk arising from maturities and put options in China's corporate-bond markets, onshore and offshore combined, further reduced in June compared to previous months, potentially lowering market volatility. In June, 726 non-bank, non-financial issuers face a combined $162 billion of principal payments, equivalent to 3.6% of the market's amount outstanding. But this is still higher than the $135 billion (3.3%) of maturities in the same month last year. On a sector level, real-estate issuers have $23 billion of maturities in June, or 3.1% of the sector's total amount outstanding, up from 2.7% in May 2022.

Investors may need to pay closer attention to distressed issuers which are or were due to pay interest or principal in June, especially issuers that have proposed debt exchanges.

Chinese bond market debt maturity profile ($)

Source: Bloomberg DDIS <GO>, Bloomberg Intelligence