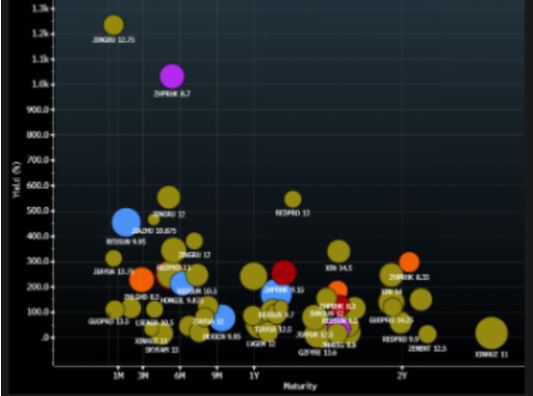

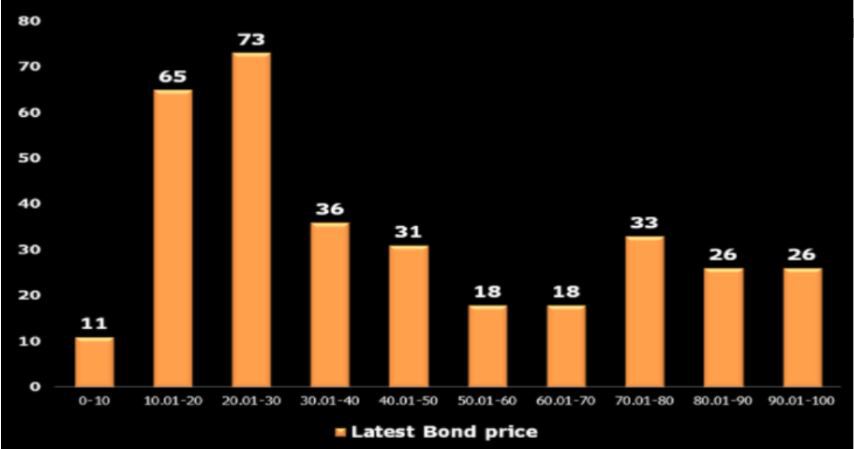

Over 50% of high-yield Chinese property developers' offshore bonds are trading below 40 cents on the dollar, which may be an indication of market sentiment more than an estimate of the issuers' recovery levels. Forty cents could serve as a guide to price levels for issuers that may be moving toward defaulting.

Middle-of-pack names remain most vulnerable Chinese developers are poised to release their 2021 results by end-March and this could allow estimated recovery levels to be updated, as the market is at present likely still using 1H21 results, which are pre-crisis financials. Defaulted issuers such as Aoyuan, Evergrande, Kaisa and Fantasia are trading at 20 cents or below. There's a wide price range for issuers that have conducted exchange offers, with Yango and Yuzhou below 20 cents while R&F trades around 30 cents.

The middle-of-the-pack names at 40 to 60 cents include Agile, Sunac, Central China, KWG, Powerlong and China SCE; they haven't defaulted. But due to the difficult conditions, we're concerned more private developers could choose to "lie flat" and default (see below), which could push their bond prices lower.

China HY bond-price distribution curve (March 1)

Source: Bloomberg Intelligence

Country garden, CIFI holding up Most bonds over 80 cents have strong fundamentals or will mature very soon, or their issuers are still perceived to have enough liquidity. Fundamentally strong names include Road King, Hopson, Dalian Wanda and China South City, possibly due to their strong recurring income, less reliance on offshore funding or potential to receive an equity injection from the state.

Country Garden and CIFI’s bond prices are still holding up relatively well; whether or not they return to par will hinge on the firms' liquidity buffers and whether their contracted sales can recover to pre-crisis levels. Due to fragile investor sentiment, we're concerned any unsubstantiated rumor or poor operating figure could create price volatility similar to the instability which accompanied Zhenro’s unexpected exchange offer.

High-yield developers' bond resolutions

Change in business model may pressure cash flow China developers' pre-sales business model may be more strictly regulated after recent incompletions by distressed developers jeopardized homebuyers. More restricted cash may need to be allocated or a certain percentage of construction may need to be achieved before sales can start. Creditor terms will also likely tighten after Evergrande's delaying payables for over 300 days ended up impairing several suppliers.

These factors will likely increase the amount of working capital required for new projects by surviving developers. As more cash will be needed for working capital, the IRR of a project will likely decline and may not be able to cover a private developer’s cost of capital.

China private developers' A/P Days (End 2020)

State-owned developers' heavy cost advantage Private developers' poor liquidity may weaken their ability to accumulate landbank during the current downturn, adversely affecting their development pipeline and future sales. Their SOE peers have a significant cost advantage as they can buy land at a lower cost in the current environment and have lower finance costs due to their state ties.

Private developers face higher risk premiums due to their off balance sheet debt, retail financial products and lax attitude dealing with creditors highlighted in this downturn. Rating criteria and audit work may need to be tightened further which could cause lower ratings and a rise in issuing yields. Single B names already generally needed to offer over 8% yields to raise debt.

China developer HY bonds (>8% coupon rate)

Source: Bloomberg Intelligence, FIW <GO>

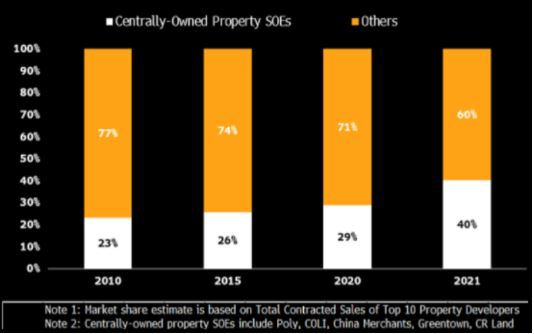

Common prosperity could influence housing prices more Chinese developers could afford high finance costs in the past partly because land they bought would increase in value, which may not continue. The government's "common prosperity" goal aims to alleviate worsened income inequality, to which rising home prices have contributed. The state also wants to raise birth rates and expensive housing has burdened couples who might want to have more than one child. This could explain why state-owned enterprises (SOEs) are increasing market share to align the property sector more closely with national objectives.

A bigger state role in housing prices or the types of projects to be developed could depress sector Ebitda margins and disincentivize private developers.

Top 10 gross contracted sales market share