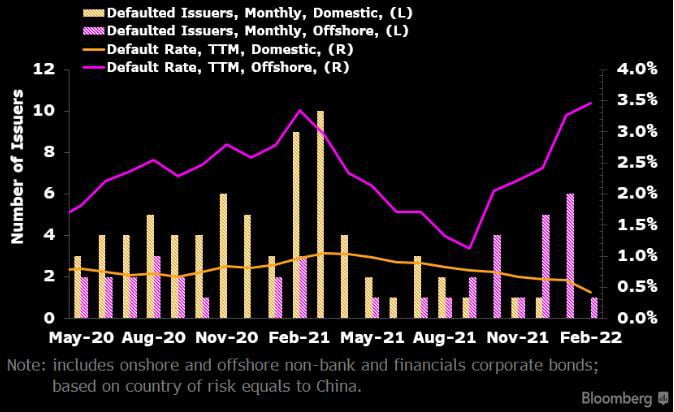

Default rate hasn't lost its rising momentum

China's March default rates may continue to trend higher as we face the largest maturity wall in 2022. This could add to what is already a record 3.45% offshore dollar-bond default rate. The default rate may reach 3.58% or higher if one or more names among the 559 issuers in the offshore market misses interest or principal payments this month -- Zhenro, Shimao, and Logan are among the high-profile issuers in the real-estate sector. The sector may continue to see default rates deteriorate in the short term as distressed issuers need to rely on asset disposals, amid a pullback in contracted sales of Chinese property, to obtain liquidity for debt repayment.

Default rates at 3.45% in February

Source: Bloomberg BQNT <GO>, Bloomberg Intelligence

The involvement of bad debt asset managers (AMCs) may help to avoid failures in the asset disposal process, and lead the default rate to improve in the next few months.

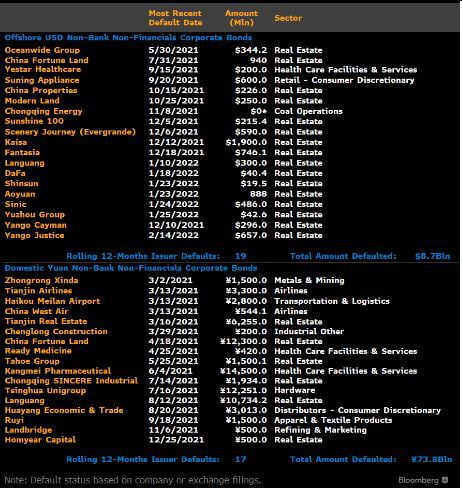

Monthly bond-default data shows recent credit events were dominated by the real estate sector, and we expect the trend will continue. As of Feb. 28, we recorded $8.7 billion of offshore dollar bonds and 73.8 billion yuan ($11.7 billion) of domestic bond defaults based on bond amounts outstanding in the last 12 months, involving 19 offshore dollar-bond issuers and 17 domestic yuan issuers.

Actual bond defaults (Mar 21 - Feb 22)

Source: SRCH <GO>, Bloomberg Intelligence

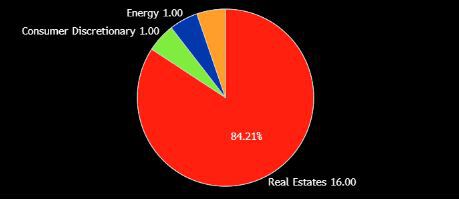

U.S. dollar issuer-based default distribution

Source: Bloomberg BQuant <GO>, Bloomberg Intelligence

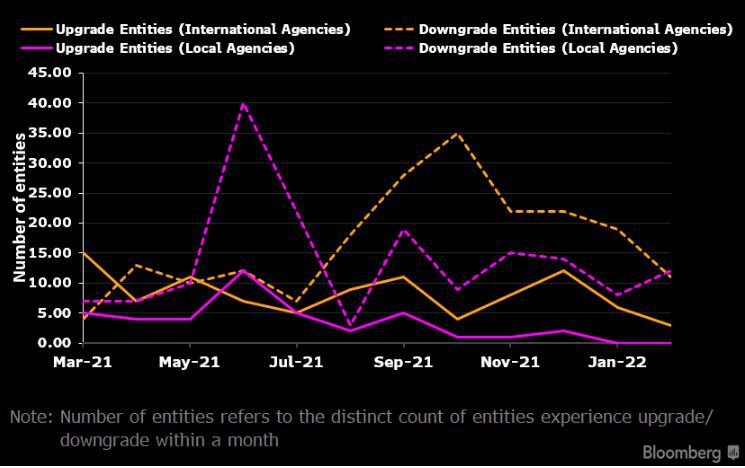

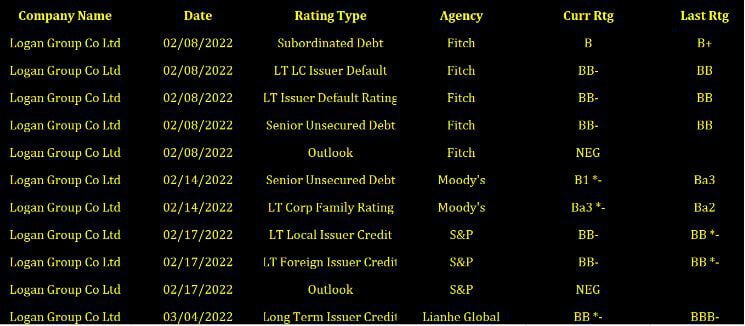

Credit rating change: Real estate had lowest upgrade-downgrade ratio in 10 years

Logan Group Ltd is downgraded by four rating agencies

Source: Bloomberg RATC <GO>

Entities experiencing rating changes

Source: Bloomberg Quant Platform (BQuant), Global Data

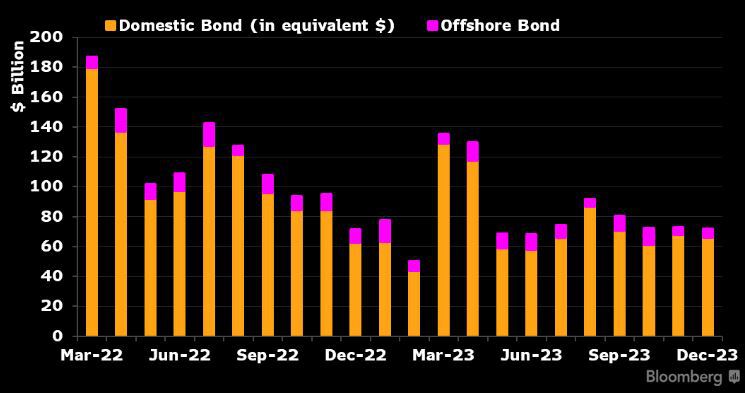

Chinese issuers face $186.6 billion maturities

China's corporate-bond markets, onshore and offshore combined, may face more refinancing risk arising from upcoming maturities and put options due, pointing to higher market volatility. In March, 898 non-bank, non-financial issuers face a combined $186.6 billion of principal payments, equivalent to 4.2% of the market's amount outstanding. This is slightly lower compared with the $191 billion (4.9% of the total) maturities in the same period last year. On a sector level, real-estate issuers have $29.5 billion of maturities, or 4% of the sector total, down from 5.6% in March 2021.

Investors may need to pay closer attention to distressed issuers who were due to pay interest or principal in March, especially issuers that have proposed debt exchanges. Click on the data tab for a list of bonds that have interest or principal due.

Chinese bond market debt maturity profile ($)

Source: DDIS <GO>, Bloomberg Intelligence

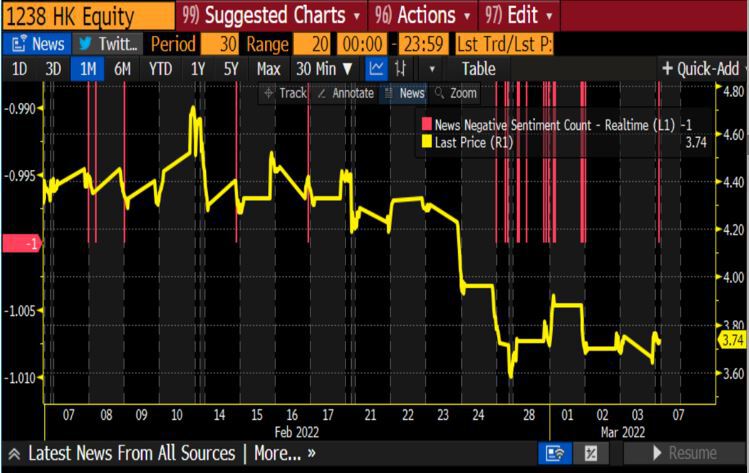

Most negative news sentiment in December

Most negative news of China offer issuers

Source: BBG TREN <GO>

Powerlong real estate news sentiment and equity price

Source: BBG GN <GO>