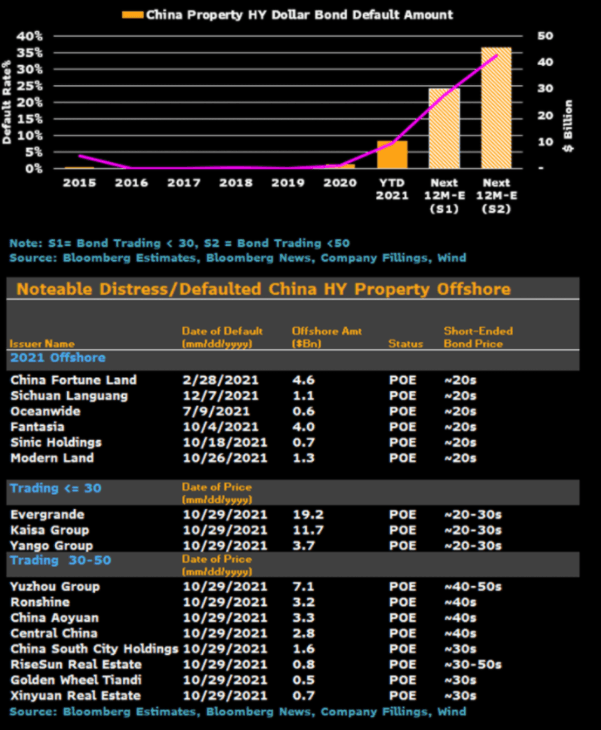

The market-implied default rate for Chinese high yield property bonds could be excessive, creating relative-value opportunities among issuers with better credit profiles or distressed names with assets to sell. A default rate of over 40% at end-October has been priced in, we calculate, using bonds trading at 50 cents or below. But even with no government or regulatory policy reversals, we believe actual defaults may be lower.

Mounting credit risk for high yield China property bonds has accelerated since the Fantasia default on Oct. 4, with almost a third since, excluding defaulted names, trading at a price below 50 -- indicating historically high credit stresses. China's property sector has seen a meaningful rise in dollar-bond defaults, with a default rate of about 8% at the end of October, and may reach as high as 25% in the next 12 months, we calculate. Refinancing channels deteriorated rapidly in 2H for the property sector, driven by credit events at Evergrande and subsequent defaults by Fantasia, Sinic and Modern Land.

We expect B category issuers are most exposed to credit events, as they rely heavily on bond markets and alternative funding mechanisms, including private debt, hidden debt via joint ventures and trust loans.