The estimate for GHG emissions outlined above is on a per tonne basis. How can benchmark investors incorporate this into their portfolios? One approach is to convert the intensities into a US dollar metric. The conversion per tonne to US dollars can be handled by dividing the intensity per tonne by the spot metal price per tonne. For metal i at time t, we have:

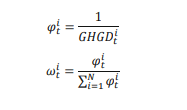

Since the numerator is estimated using a long history while the denominator is a spot measure, the time variation in the measure is from the denominator — similar to a dividend yield measure for equities (Figure 9).

Figure 9: GHG per US dollar

Source: Bloomberg

Changes in GHG per US dollar (GHGD) is implicitly an inverse function of price trends; a negative trend in a metal’s price translates to an increase in the GHGD. This can be explained in the following terms: a cheapening of an asset (in this case the commodity future) translates to a greater number of futures purchased—indirectly resulting in holding more physical assets. Given this relationship, tilting exposures based on GHGD will introduce trend-based tilts.

In this study, portfolios are rebalanced on a monthly frequency; weights are calculated at each month-end and applied in the upcoming month. It is important to note that for all three models presented, the results are not point-in-time since the GHG estimate encompasses the full sample. From September 2020 onwards, results will contain no forward-looking data.

Weights are allocated to commodities inversely proportional to the GHGD value. This approach seeks to equalize the marginal contributions to GHG emissions per commodity. The methodology is identical to an inverse volatility portfolio and is a 2-step process. For commodity i at time t, the weight allocated (ω) is given by:

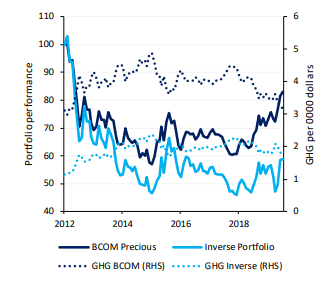

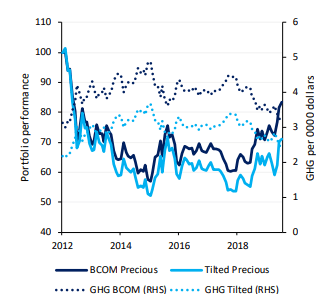

Figure 10: Precious metals

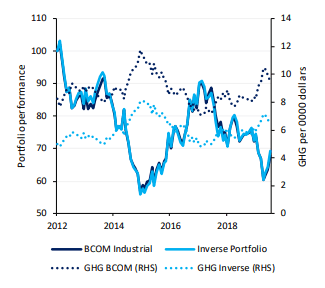

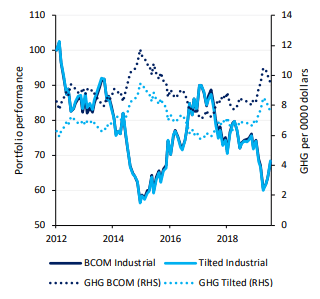

Figure 11: Industrial metals

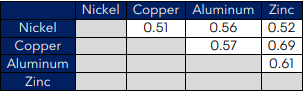

The results for precious metals and industrial metals are strikingly different. With precious metals, there is a trade-off between the GHGD of the portfolio and the annualized portfolio return (Figure 10). In the case of industrial metals, a lower GHGD is not accompanied by any performance degradation (Figure 11). This can be explained by (1) the number of constituents per portfolio and (2) the relationship between metal prices.

Figure 12: Industrial metals: similar pairwise correlations

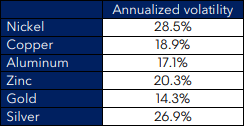

Figure 13: Annualized volatility of returns

While the correlation between gold and silver is high (0.8 over the period 2012 – June 2020), silver volatility is approximately twice that of gold (Figure 13). An increase in the weight of silver leads to higher portfolio volatility. Furthermore, during the recent past the correlation between gold and silver has fallen (0.6 over the period 2018 – 2020) with inflationary concerns and the use of gold as a store-of-value asset. From Figure 9, we see the GHGD for silver is approximately 1/5th that of gold. As a result, the precious metals portfolio consists of 70-80% silver and 20-30% gold; which is a reversal of the weights in the BCOM precious metals index. The average reduction is 2.1 tonnes of GHG per 10,000 dollars in exchange for a reduction in returns of 4.4 % per annum.

The similar performance of the inverse GHGD weight industrial metals portfolio and the BCOM Industrial Metals benchmark can be attributed to the similar correlations (Figure 12) and volatilities (Figure 13) between the four industrial metals. In the portfolio context, the impact of the relatively high volatility of nickel is mitigated by the modest pairwise correlations. In effect, this makes the

constituents of the industrial metals portfolio interchangeable—leading to the result of lower GHGD with little impact on portfolio returns.

The inverse GHGD weighting provides a route to lower the value of GHG associated with a commodities portfolio. However, it does not control—either implicitly or explicitly—the degree to which the ESG portfolio deviates from the BCOM benchmark. This unconstrained portfolio might not suit those seeking to both incorporate elements of ESG investing while continuing to track the broad benchmark. To account for this, we modify the model above in two ways; the first is by applying a rules-based tilt on BCOM weights and the second is to use an optimization-based approach.

We combine the GHGD scores and the BCOM benchmark weights. Once again, we maintain a monthly rebalancing frequency. At a given time t, the modified score for commodity i is given by τ:

Here β and ω refer to the BCOM benchmark weight and inverse GHGD weight, respectively. The degree to which weights are tilted based on GHG scores is controlled by γ (tilt factor). For illustration purposes, we set γ = 1 for the remainder of this section. The final weight is given by:

The results over the period 2012 – June 2020 are shown in Figures 14 and 15. With respect to the precious metals portfolio, lowering the impact of the GHGD score relative to the inverse GHGD approach moderates the underweight in gold (relative to the BCOM benchmark). Over the sample period, the average allocation to gold was 48 %. Relative to the BCOM Precious Metals benchmark, a reduction in 1 tonne of GHG (per 10,000 dollar) is accompanied by a corresponding decline in portfolio returns of 2% per annum (Figure 14).

In the case of industrial metals, the results are similar to that of the inverse GHGD portfolio. There is little-to-no impact on portfolio performance by introducing GHG-based tilts. However, the reduction in GHG per 10,000 dollars is smaller (but still meaningful) given the objective function is not solely GHG reduction (Figure 15).

Figure 14: Precious metals

Figure 15: Industrial metals

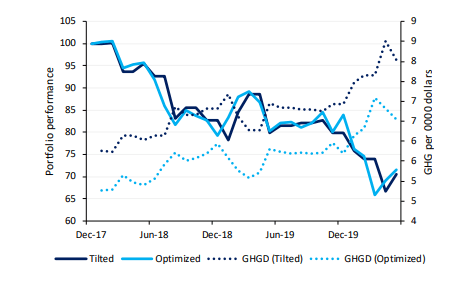

Finally, we turn to an optimization based approach to assign weights. The objective function is the minimization of (portfolio) GHGD while controlling for deviations in returns and constituent weights, from the benchmark. The weight constraints can be viewed as an additional layer of security in the event of a sudden change in the correlation structure. Weights are floored at 0.5x that in the BCOM sector benchmark.

For consistency purposes, we maintain the identical lookback window over which volatility and correlations are calculated. To ensure a sufficient window length for estimation stability, we use 36-monthly returns. In this example, we use a TEV constraint of 100 bps per month. Relative to the rules-based tilted portfolio, optimization offers a more significant reduction in GHG per dollar invested (Figure 16).

Figure 16: Performance versus GHGD: Optimization versus tilting