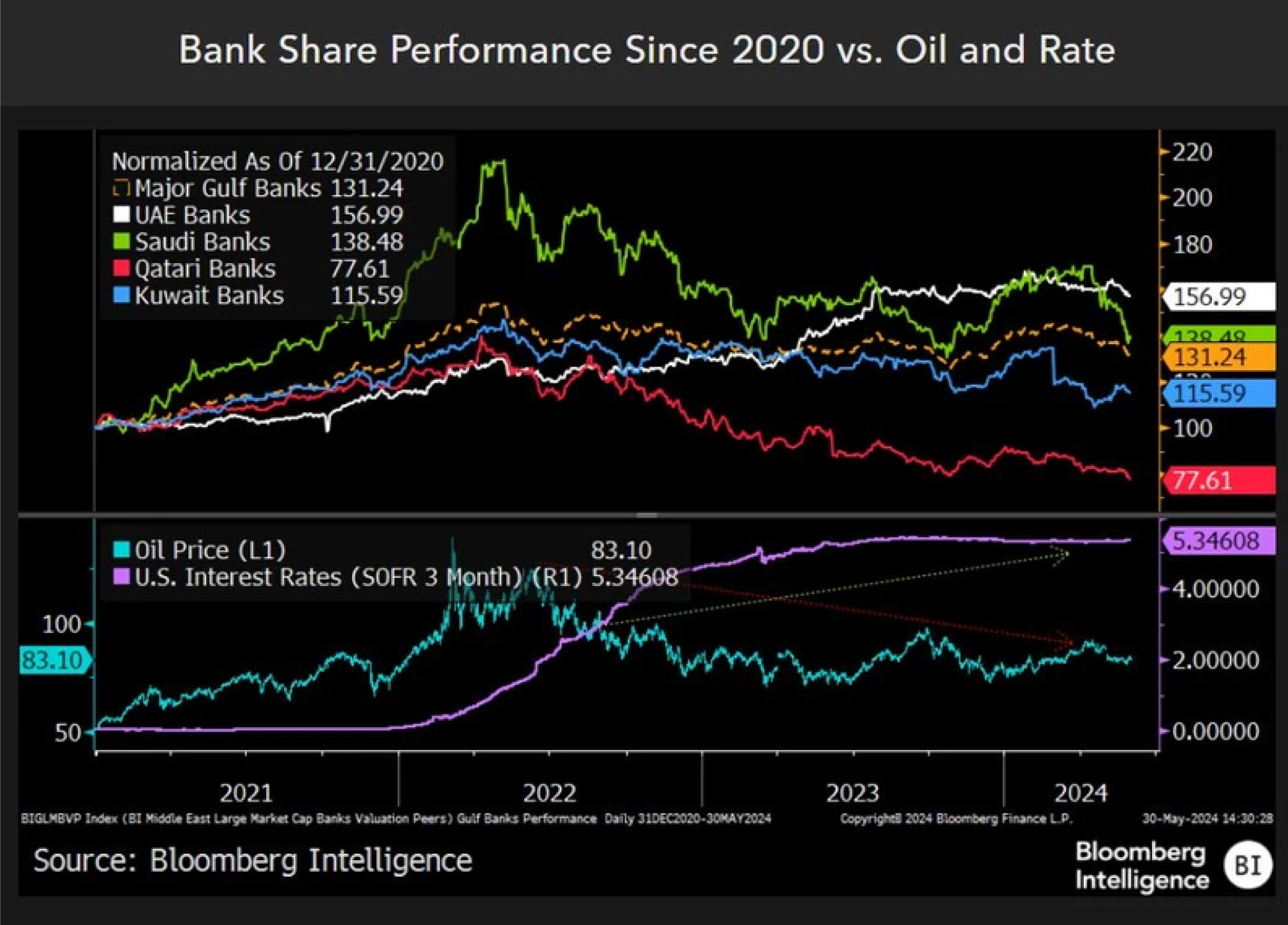

Closing NIM gap, strong oil prices could aid valuation

Qatari Banks’ relative valuation, currently trailing Gulf peers, could get a boost if cyclical factors, particularly net-interest-margin differentials, gradually diminish. Driven by relatively stable NIMs, the sector’s margin lags Gulf peers that have had a rate-hike boost, though this gap is likely to normalize over time.

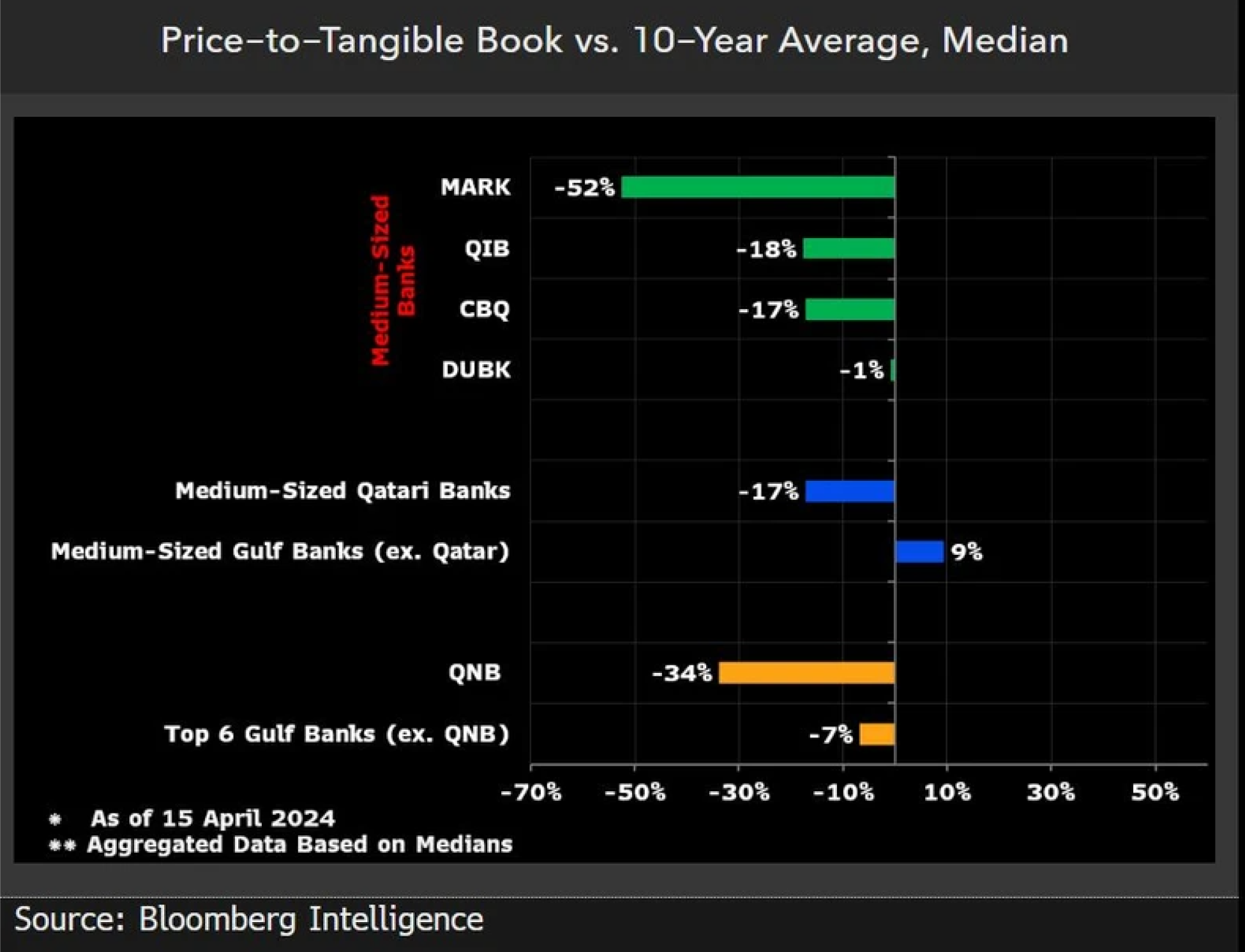

Lingering asset quality concerns, stemming from oversupplied real estate, also contribute to subdued valuations, with banks trading at a price-to-tangible book discount of 17% (median) vs. their 10-year average.

Geopolitical tensions and potential travel disruptions could heighten real-estate risks, with medium-sized banks (CBQ, QIB, MARK and Dukhan) more exposed. However, oil prices above $80 and the dominance of the public sector may help mitigate potential losses.