This article was written by Tasneem Brogger. It appeared first on the Bloomberg Terminal.

ESG investing, you may have noticed, has become a political lightning rod in the US. To liberals, it’s slowing global warming and fighting social injustice. To conservatives, it’s spoiling the economy and the American dream. So is it saving the world or destroying it? Truth is, it’s doing neither. But left to its own devices, the lucrative ESG fund industry is doing a pretty good job at destroying itself.

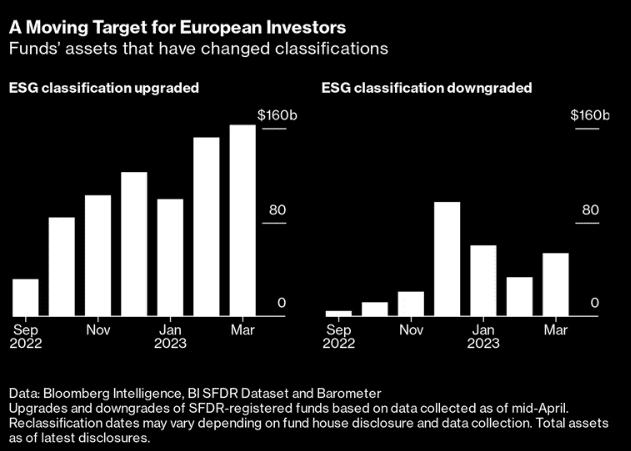

Bloomberg Intelligence has estimated that global ESG investment could hit $50 trillion in 2025, triple the amount in 2014. But without a common definition of what makes for good environmental, social and governance investments, fund companies have been free to slap the ESG brand on just about anything. Trusting investors often put money toward companies they might otherwise wish to avoid. Even ESG adherents sometimes have a hard time defending the label, in part because of disagreement over what it’s supposed to measure.

Companies that score ESG investments seem equally confused. By the end of April, 31,000 funds were set to have their ESG ratings downgraded by a unit of MSCI Inc., which created its first ESG-like index in 1990 and is today one of the largest firms scoring funds and companies on ESG. (Bloomberg LP, the parent of Bloomberg Businessweek, also provides ESG scores.) The changes mean that only 0.2% of MSCI-graded funds will have the highest rating in the future, compared with about 20% now, raising questions about the value of such scores.