China focus

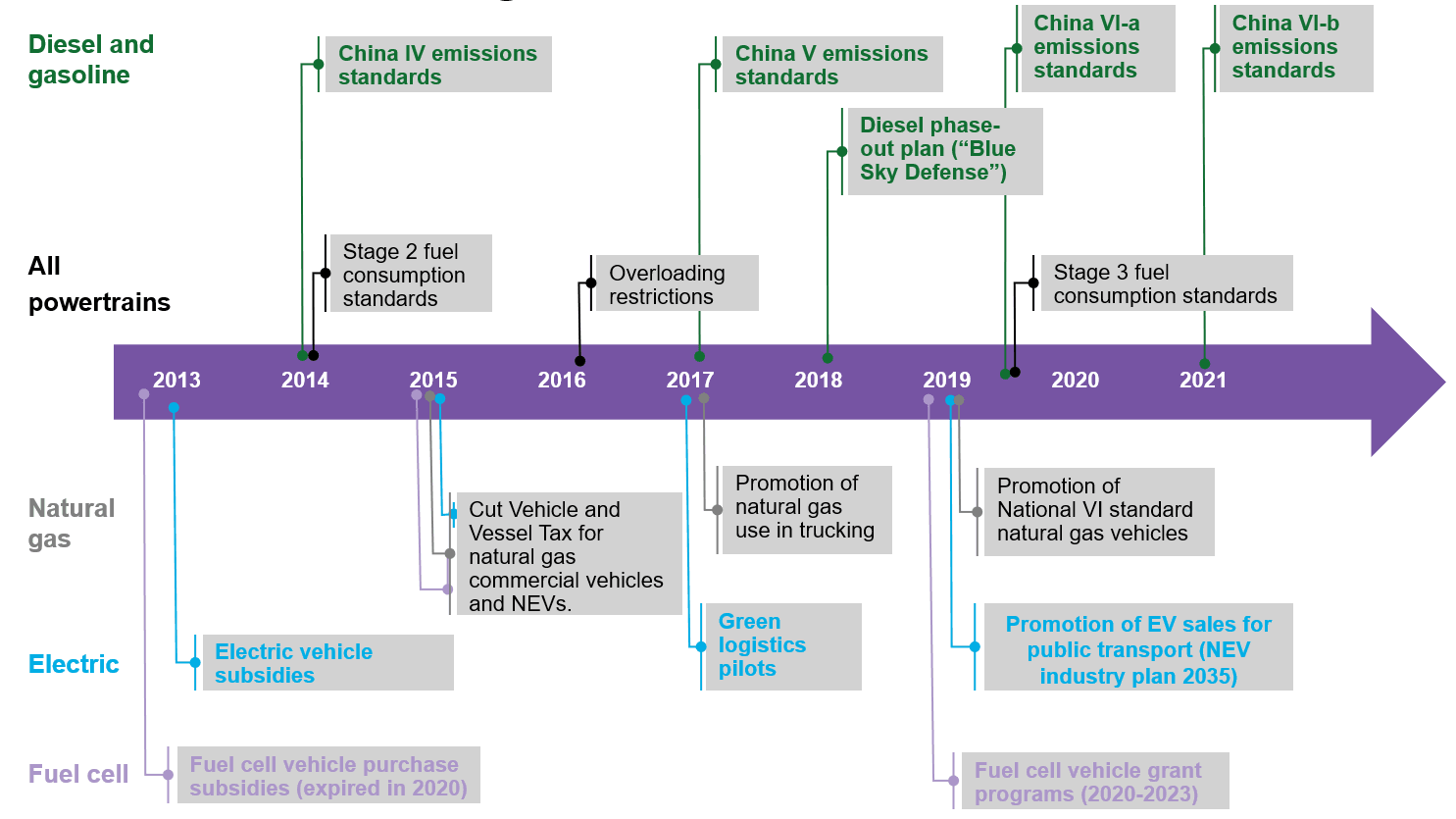

China’s heavy-duty commercial vehicle (HCV) fleet has been increasing the adoption of LNG fueled models at the expense of diesel over the last decade. Policy measures from local access restriction to provincial and national measures, such as emission standards, have helped drive up LNG HCV adoption.

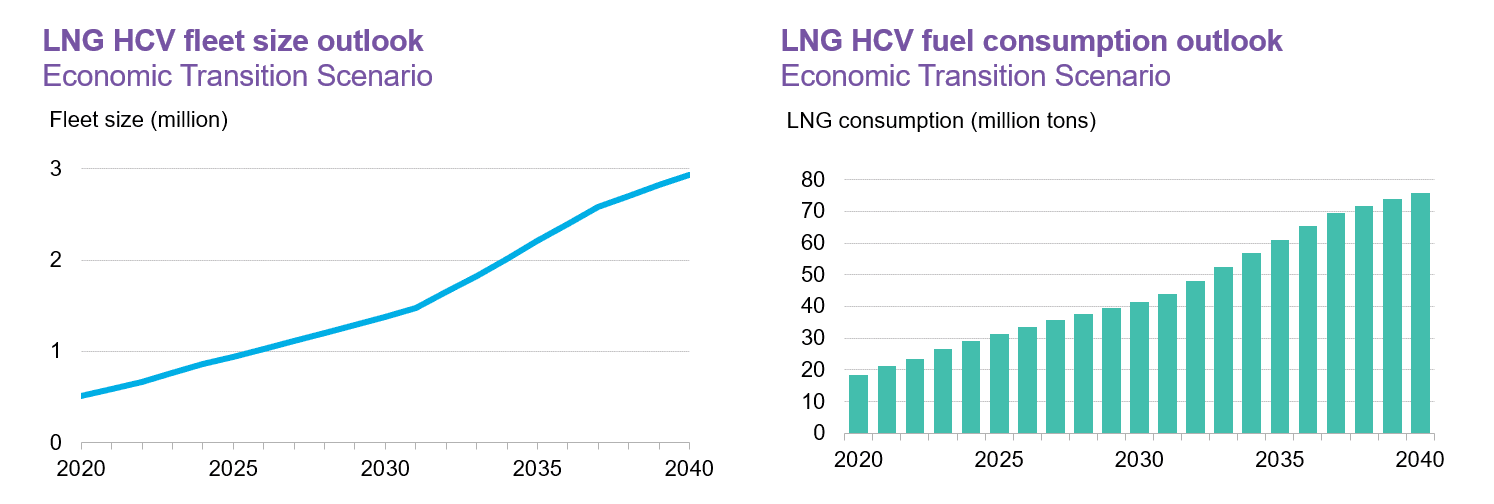

Source: BloombergNEF’s Long-Term Electric Vehicle Outlook 2021. Note: For the calculation of LNG HCV fuel consumption, average annual mileage of LNG HCV is assumed to be 12,000 km; fuel efficiency assumed to be 0.3kg/km with improvements over the two decades. See BloombergNEF’s EVO 2021 report for more details on the Economic Transition Scenario.

China’s national policies encourage natural gas as a fuel to replace diesel use by commercial vehicles. However compared to China’s comprehensive support for new energy vehicles (NEV) – which include battery electric, plug-in hybrid and fuel cell vehicles – there are fewer measures supporting LNG fueled HCVs.

Electric commercial vehicles: While policy measures for passenger electric vehicles in China have been very strong, there is currently limited direct support for electric commercial vehicles. The government is considering a NEV credit regime for commercial vehicles, setting annual NEV sales quotas.

Fuel cell commercial vehicles: Some municipal and provincial governments in China have provided incentives to fuel cell commercial vehicle manufacturers as well as subsidized deployment of hydrogen refueling infrastructure. The national government has non-binding targets for increased adoption of fuel cell powered medium- and heavy-duty commercial vehicles and buses by 2035.

Diesel: Several cities, ports and mines have restricted diesel trucks’ access. Overloading restrictions effective from 2016, have also led logistics companies to buy new trucks. Introduction of China VI emissions standards in 2020 has also forced replacement of China III diesel HCVs. All these factors have boosted demand for LNG HCVs at the expense of diesel HCVs.

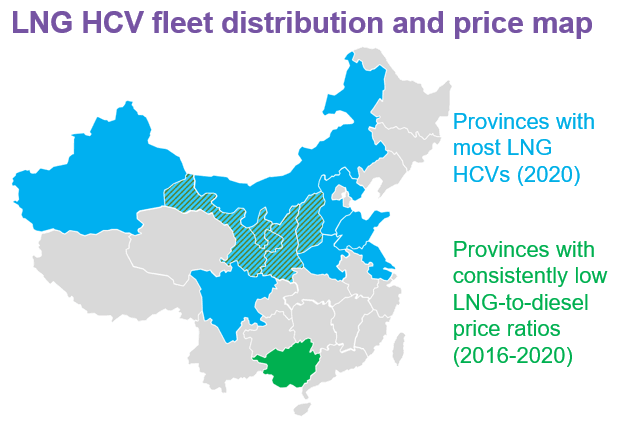

The top-10 provinces, accounting for more than three quarters of the total fleet, are mostly located in northern and northwestern China. Shandong, Hebei, Xinjiang, Jiangsu and Shanxi are the top five Chinese provinces in terms of number of LNG HCVs.

In most of these provinces, the retail LNG-to-diesel price ratio is lower than 70%. This threshold divides areas where LNG HCVs have been growing from the rest. The ratio will largely fluctuate with LNG prices as diesel prices are fairly stable or regulated. Northern provinces, however, consistently have lower LNG-to-diesel price ratios. These provinces either have abundant domestic natural gas, for example in the case of Xinjiang, or have a great need to transport local resources – for example coal in Shanxi – to elsewhere in the country.

It is difficult for LNG heavy-duty trucks to penetrate provinces in the northeast and the south due to scarcity of LNG supply and high price of imported LNG relative to diesel. Guangxi in Southwest China is an exception with relatively low LNG retail prices due to low demand.

Source: BloombergNEF. Note: Terminal capacity is existing and under construction.

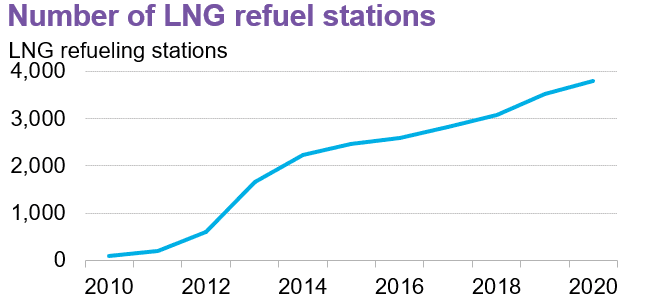

Source: China National Offshore Oil Corp., BloombergNEF.

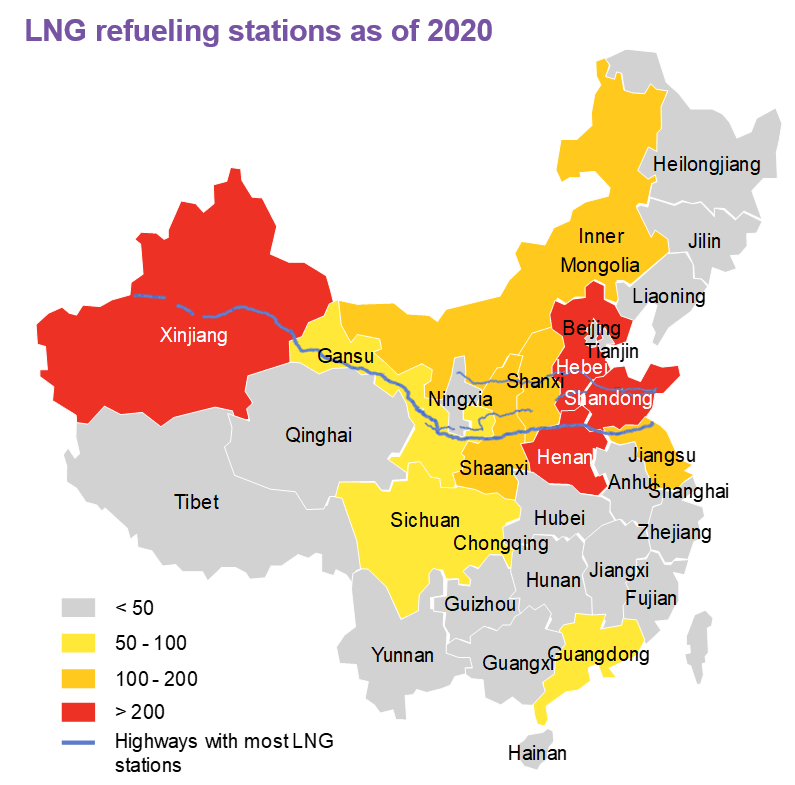

Source: China National Offshore Oil Corp., China Society of Automotive Engineering, BloombergNEF. Note: BNEF assumes station number to be the average of various industry sources.