Topics in this section: - Automaker R&D, capital-spending spiral seeks tech transformation - EU automakers' 650 billion-euro sales risk - German rivals set to spoil Tesla profit debut - VW, Audi and Porsche have EV scale, China - R&D expands to address changing technology - BEV, PHEV following similar trajectory, HEV wins - BMW electric sales on target; 25% German discount - BMW, Mercedes, VW face reputation risk on AD

These analyses are by Bloomberg Intelligence analysts Kevin P Tynan and Michael Dean, and contributing analyst Gillian Davis.

Tesla, Uber and Lyft have a total implied value of $133 billion, while EU automakers, that failed to gain recognition for electric-vehicle, autonomous driving and mobility efforts, languish at crisis-level multiples. EU automakers are nevertheless set to flex their balance-sheet muscles with an R&D and capex surge aimed at winning the tech race.

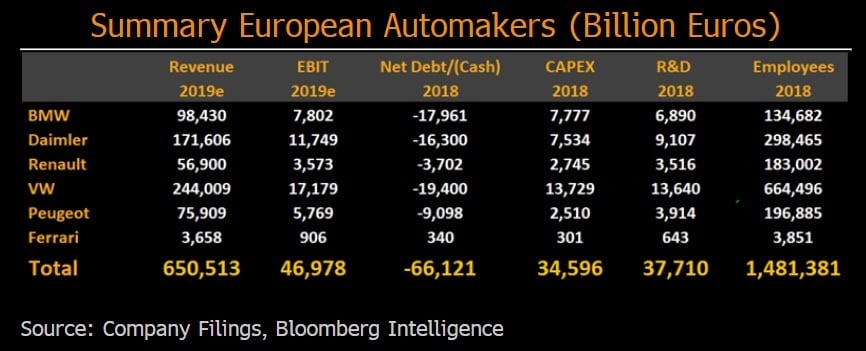

EU automakers' 650 billion-euro sales risk

EU automakers' combined Ebit of 47 billion euros is at risk, given tech uncertainty -- including the transition phase to electric vehicles -- and the threat from Tesla and other new entrants. Yet net cash of over 60 billion euros puts EU automakers in a strong position to invest in new technologies, and unlike Tesla, EV losses can be offset against profitable combustion-powered sales. Volkswagen and Daimler's credentials are being tested by the Audi e-tron and Mercedes EQC battery-electric-vehicle launches, but even Daimler's former CEO Dieter Zetsche said he has no idea what EQC demand will be in 2019. Targets for 25% EV market share by 2025 are largely in place to justify immense R&D budgets, rather than based on pent-up demand, in our view.

German rivals set to spoil Tesla profit debut

This analysis is by Bloomberg Intelligence analysts Kevin P Tynan and Michael Dean.

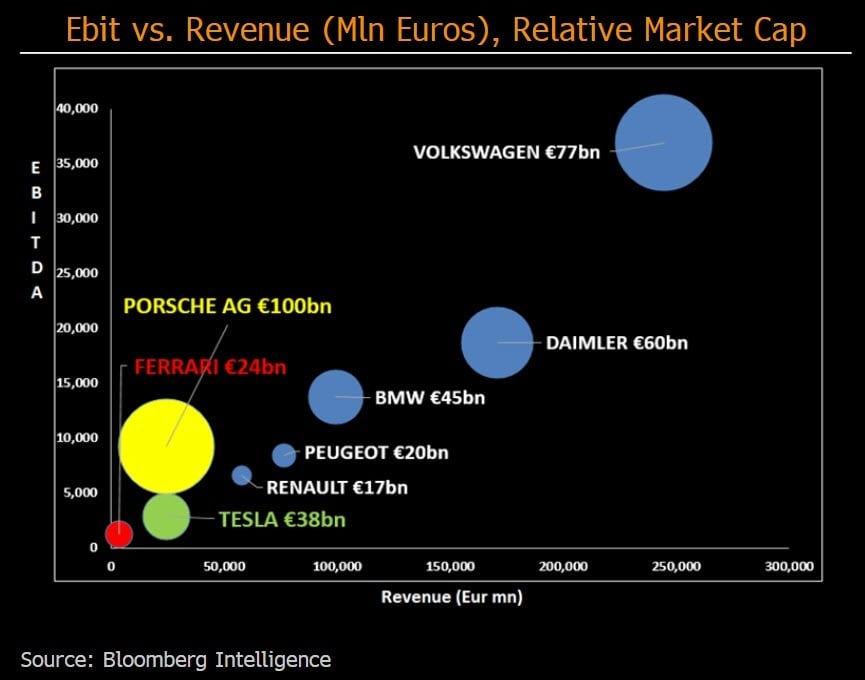

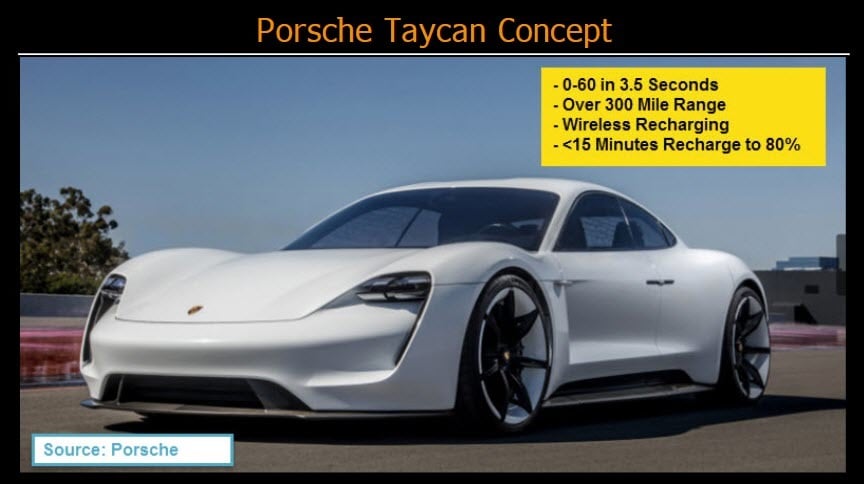

Tesla's first quarterly profit in 2018, while commendable, needs to be put into context given its $40 billion market cap, as venerable European rivals erode its monopoly on premium battery electric vehicles. Porsche is set to take the pole position in electric-car performance with its Taycan BEV, competitively priced at about $75,000, equivalent to Tesla's top-end Model S. Yet Porsche's 6.5 billion euros of Ebitda is barely recognized in Volkswagen's 77 billion-euro market cap. The Taycan and Mini E will follow Audi, Mercedes and Jaguar battery-powered cars.

While the latter failed to raise the tech bar, the carmakers are mindful that EVs lack scale and dilute margin. BEV capacity will take time to ramp up, with German carmakers waiting until 2020-21 for a volume and tech push, given more onerous emission legislation.

VW, Audi and Porsche have EV scale, China

Volkswagen appears well-positioned throughout its brands to benefit from the transition to electric vehicles and New Energy Vehicle rules in China starting in 2019. The company has a significant scale advantage, with prospects for more than 150,000 EVs in China alone from 2019, given its 18% market share. A leading electric-car position in the U.S. may arise by default, given a $2 billion forced investment into zero-emission infrastructure as part of the dieselgate settlement.

The Porsche Taycan is a threat to Tesla in 2020, with spyshots indicating styling as a smaller but better-looking Panamera. VW said 80 EV models, including hybrids, will be available by 2025. That will expand to 300 by 2030, with the whole range available as EVs.

R&D Expands to address changing technology

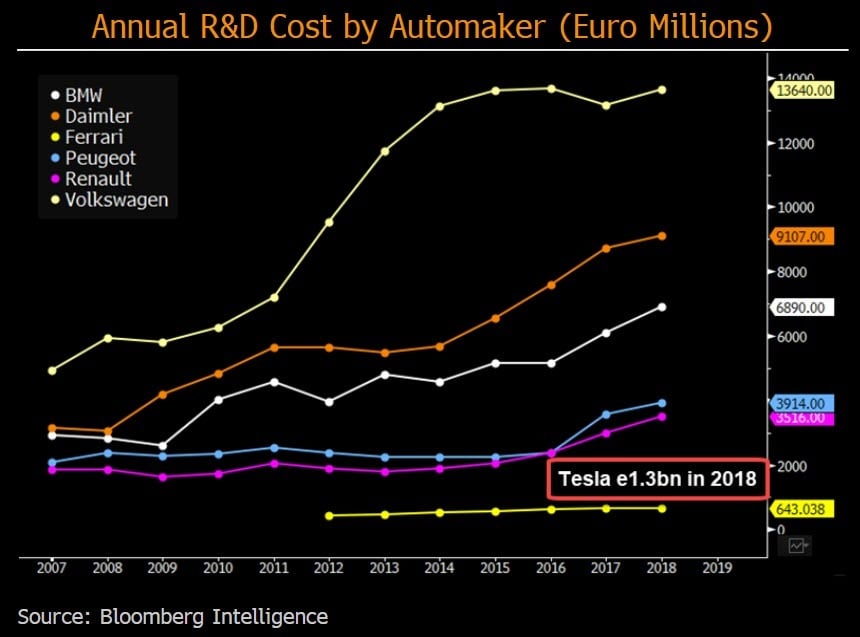

Daimler and BMW's R&D expense have doubled from 2007-08 levels amid expanding model ranges and onerous new emission legislation affecting cars and heavy trucks. An accelerated rollout of electric vehicles for BMW, Mercedes and Volkswagen, announced during the 2017 Frankfurt Motor Show, means this R&D trend will continue, along with increased spending on e-mobility, connectivity, digitalization and autonomous driving.

VW's R&D budget is the third-largest globally, behind Amazon.com and Alphabet, and the company had a 2018 R&D ratio-to-sales of 5.8% vs. Daimler's 5.4%. BMW ranks third among European automakers' R&D spending and will likely again exceed its target of 5-5.5% in 2019. Tesla's R&D ratio was 6% (from 11.7% in 2017). Ferrari's is 18.8%.

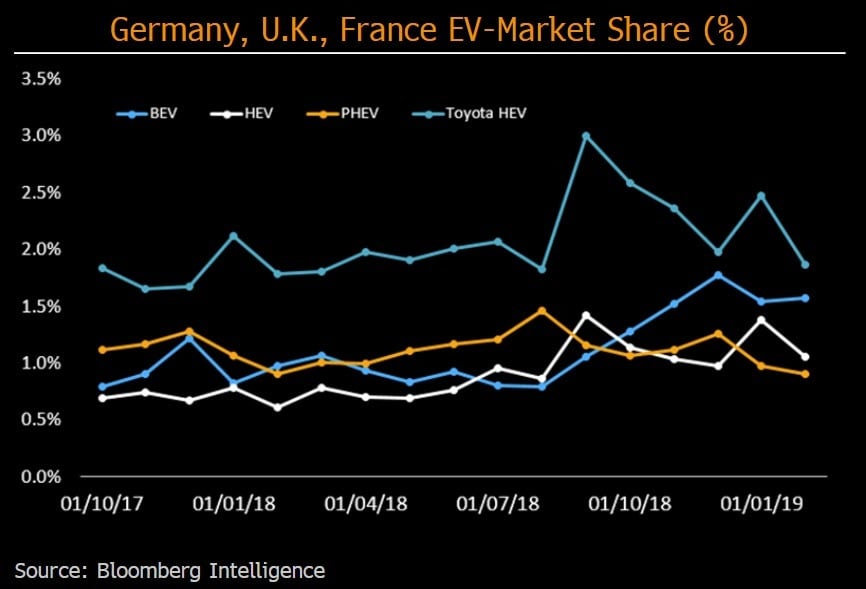

BEV, PHEV following similar trajectory, HEV wins

There's a clear distinction between demand for plug-in vehicles (BEV or PHEV) and gasoline hybrids (HEV), with the latter faring better and enjoying a 3.8% European market share in 2018, according to ACEA, given the lack of charging infrastructure. Toyota is the clear leader, accounting for 70% of HEV 2018 sales in Germany, the U.K. and France, according to JATO Dynamics. With 20 years of experience in this technology, selling more than 10 million units, the company has a significant scale and cost advantage.

The split of EV demand in the U.S. is similar to Europe's, with HEV dominating with 2.7% share of the overall auto market. Total U.S. EV sales made up a market share of 4% in 2018, below that of Europe at 5.8%. China's were 5.5% in 2018, with BEV accounting for 50% of total EV demand.

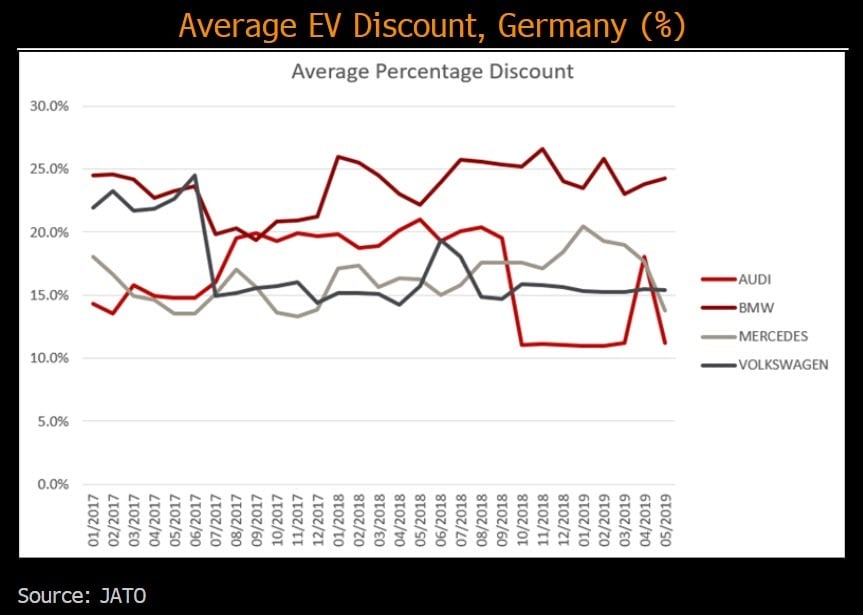

BMW electric sales on target; 25% German discount

BMW is the only traditional automaker to have an annual EV sales target and was the first EU premium brand to release a BEV with its i3 model in 2013 which continues to sell at a significant loss when including R&D costs. The company is well on track to sell over 140,000 EVs in 2019 with discounts running close to 25% in Germany, as a percentage of list price, according to JATO Dynamics.

Despite their unprofitable nature at current volumes and battery prices, German automakers appear keen on selling more EV's domestically with discounts averaging 18% with an aim to remove older diesels from the roads and avoid further city bans. This task is made easier in 2H with new Mercedes and Audi BEVs competing directly against Tesla sedans but with the benefit of being SUVs, the fastest growing segment.

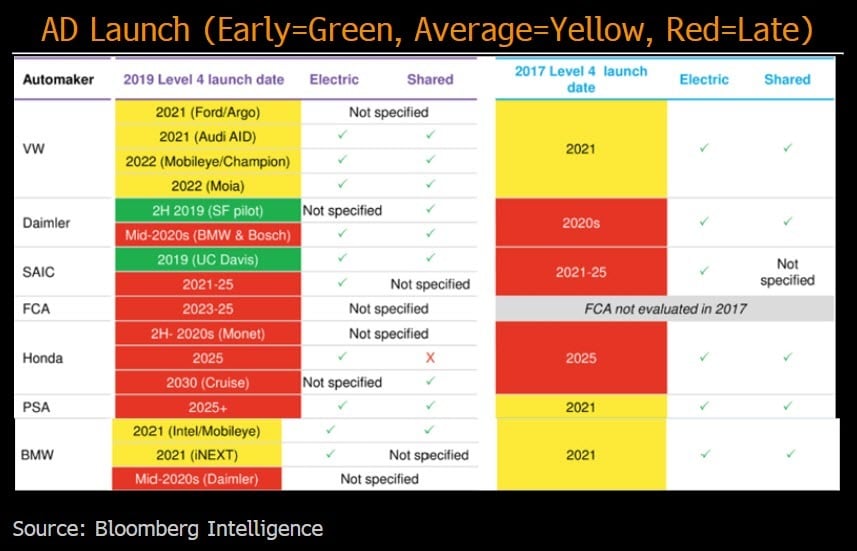

BMW, Mercedes, VW face reputation risk on AD

Fatal accidents involving Tesla's autopilot function made global headlines, and the reputational risk for BMW, Mercedes and Volkswagen after "dieselgate" means it's too risky for German brands to rush their autonomous-driving launches despite perceived rewards, in our view. This should mean an extended period of ring-fenced analysis and refinement before commercial launch, potentially trailing global peers. Artificial intelligence, high coded algorithms, sensors, mapping and computer power already allow numerous vehicles to be tested globally, with driverless types close to being safe 99.9% of the time. The risks still lie with the 0.1%.

Tesla hopes to top its autopilot with a camera-based image-recognition system that can achieve Level 4 vs. a peer group that favors a multisensor and light-detection-based (LIDAR) approach.