Biotech indexes have outperformed the S&P 500 since the start of the pandemic, and this trend may continue in 2021, given the sector's defensive nature and coronavirus vaccine and therapeutic news flow. The best earnings growth is coming from Regeneron and BioMarin. A high-profile FDA decision on Biogen's aducanumab is a wild card for sector sentiment.

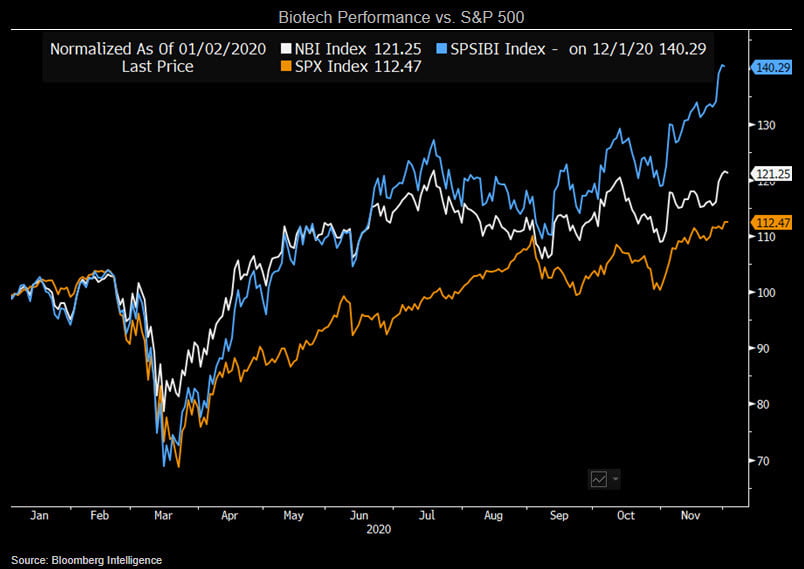

Biotech outperformance may continue in 2021

Biotech outperformed the S&P 500 in 2020, starting with the onset of the pandemic, and this may continue into the new year, given its defensive status, a steady flow of drug development news and a broad economic recovery skewed to 2H. Positive momentum on the Covid-19 vaccine front is predominately a large-pharma story, but Moderna is a notable exception. Wide-scale deployment of vaccines may diminish the need for Covid-19 therapeutics, including those from Gilead and Regeneron, but the consensus on these products has been reined in, appropriately, in our view.

An FDA decision on Biogen's aducanumab, expected by March, may have significant implications for sector sentiment. In the U.S., proposed drug-pricing plans would pressure biotech companies that rely heavily on biologics, but procedural and political obstacles exist.

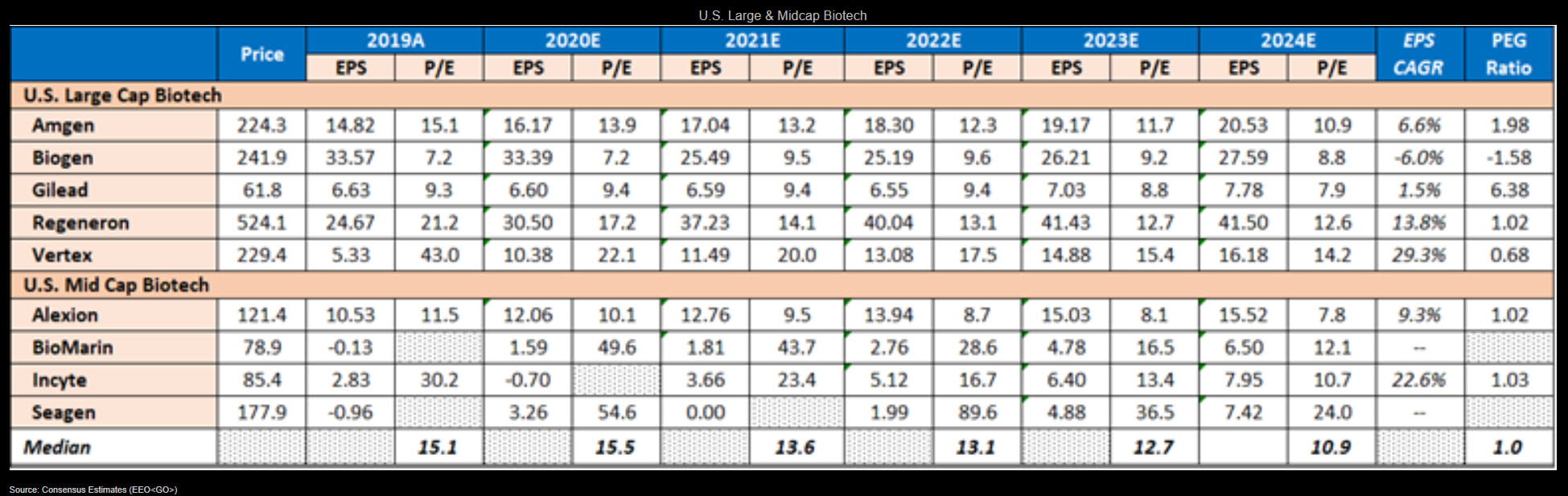

Vertex PEG ratio trails U.S. Biotech peers

Based on consensus annualized earnings gains over 2019-23 and 2021 EPS, Vertex has the lowest P/E-to-EPS growth (PEG) ratio among U.S. large and midcap biotechs, while Gilead has the highest. Vertex's dominant cystic fibrosis franchise is expected to continue to perform over this period while its pipeline needs more time to mature. Gilead's Covid-19 therapeutic Veklury is expected to decline after $1.9 billion of sales in 2021, but consensus still looks for close to $1 billion in 2023. A more pronounced fall-off is possible if vaccines take hold, in our view. Earnings growth is expected to be strong for Regeneron and Incyte over the medium term, based on continued uptake for existing drugs and, for Incyte, new-product launches.

Biogen's weakening earnings underscore the need to replace Tecfidera's U.S. revenue.

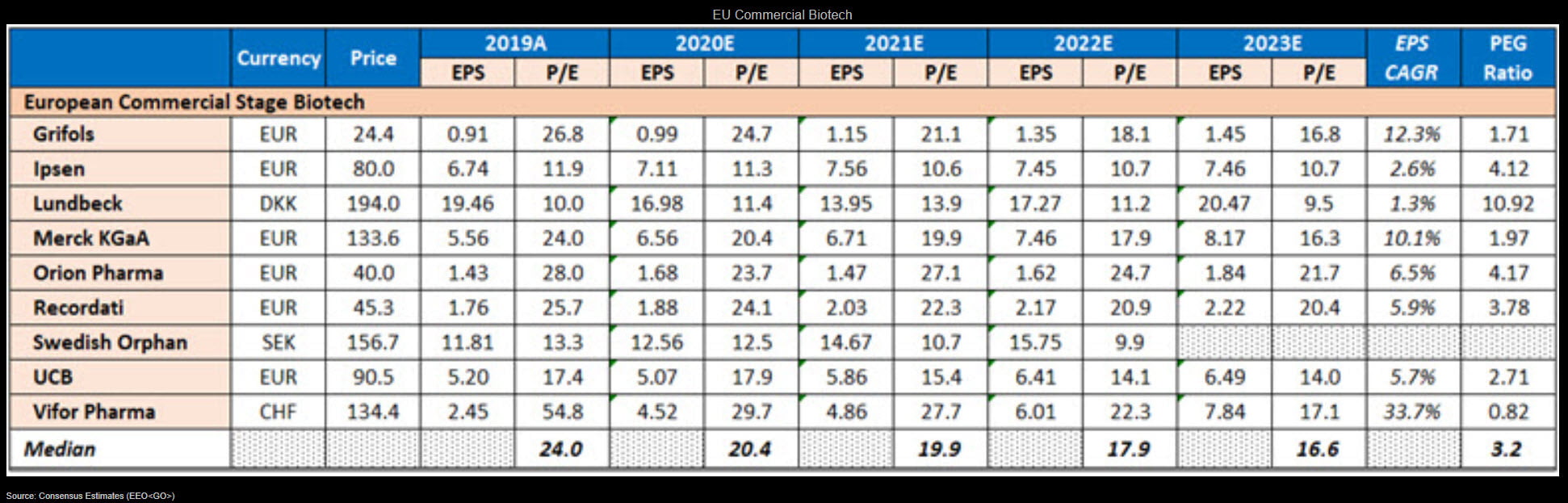

Merck KGaA PEG trails European peer median

Using consensus annualized earnings gains over 2019-23 and 2021 EPS, Merck KGaA has one of the lowest P/E-to-EPS growth ratio (PEG) among commercial EU biotech peers, with contributions likely stemming from all three of its business units. UCB's PEG ratio is also below the median, with upcoming launches outweighing patent expirations and driving earnings gains. The timing of direct and indirect competition and the potential approval of rare-disease drug palovarotene are key swing factors for Ipsen, whose ratio sits just above the median, while Lundbeck has the highest among peers. Patent expirations and investments into the Vyepti launch and its pipeline will weigh on Lundbeck's earnings growth over the medium term, with Ebit margin only expected to return to historical levels in 2023-24.

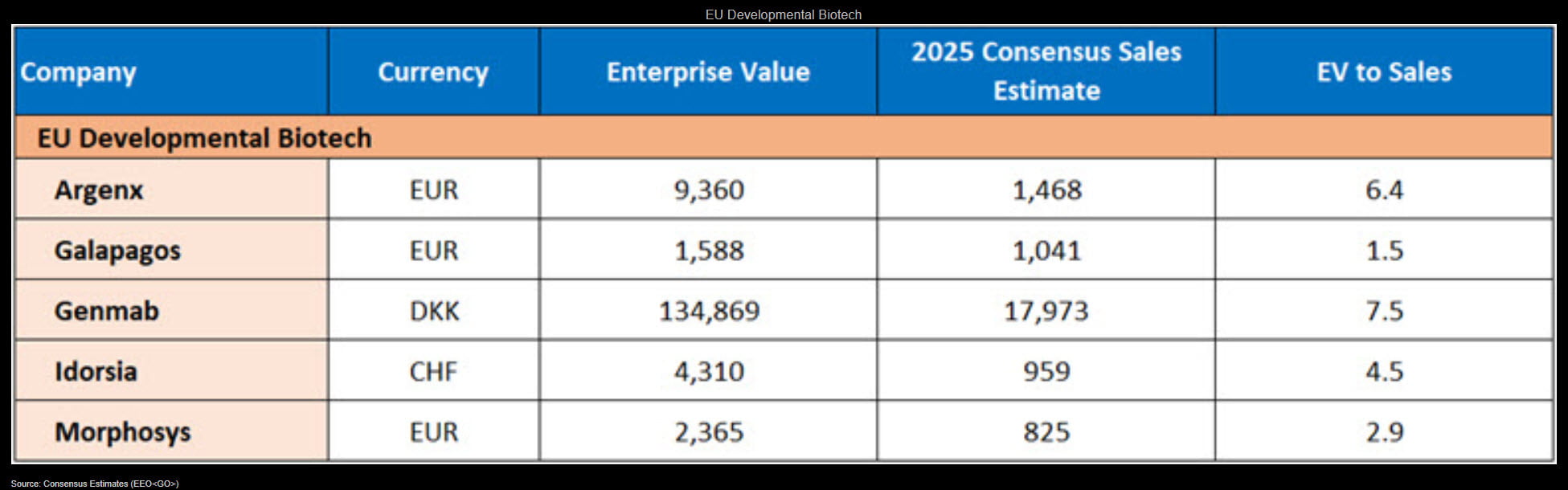

Argenx, Genmab valuations at top end vs. peers

Relative valuations of Argenx and Genmab, based on the ratio of enterprise value to 2025 sales, are at the top end of European developmental-biotech peers. Genmab's near-term prospects seem bright, based on royalties from Darzalex sales and strong recent launches, while its robust pipeline holds long-term potential. Argenx' valuation is driven by efgartigimod in myasthenia gravis, and possible label expansion into other indications where the drug has shown promise isn't fully reflected. Galapagos' multiple is at the low end of peers, following setbacks in 2020, but the company has several catalysts in 2021. MorphoSys' valuation reflects Monjuvi's efficacy in lymphoma and mounting royalties from J&J. The Incyte pact could enhance Monjuvi's launch, while new indications and pipeline advancements may aid Morphosys' prospects.