Though the resurgence in Covid-19 cases is a risk, we believe biotech could see a gradual normalization of the operating environment in 2021, assuming meaningful vaccine deployment. Low-single to double-digit revenue growth and modest margin contraction is possible, with outliers such as Seagen seeing strong launches and Biogen and Lundbeck facing generic-drug drags.

Biotech well-positioned for 2021; Virus a wild card

While some drugs, such as Biogen's Tysabri and Ipsen's Dysport, have been more affected than others by the pandemic, commercial-stage biotechs have held up well and, for the most part, are in solid positions headed into 2021, in our view. In general, 2020 guidance was at least reaffirmed, suggesting the recovery is on track, while new patient starts and visits are going in the right direction. Virtual launches, including Gilead's Trodelvy and Seagen's Tukysa, have proven viable as companies pivot to digital promotion. We expect Covid-19 vaccines from Pfizer, Moderna and others to be deployed in 2021, with a gradual return to normalcy in 2H, including a potential rise in operating costs.

A surge in cases poses near-term risk, but the introduction of therapeutic antibodies from Eli Lilly and Regeneron may mitigate the impact.

Seagen Top-Line Growth Masked; Biogen Faltering

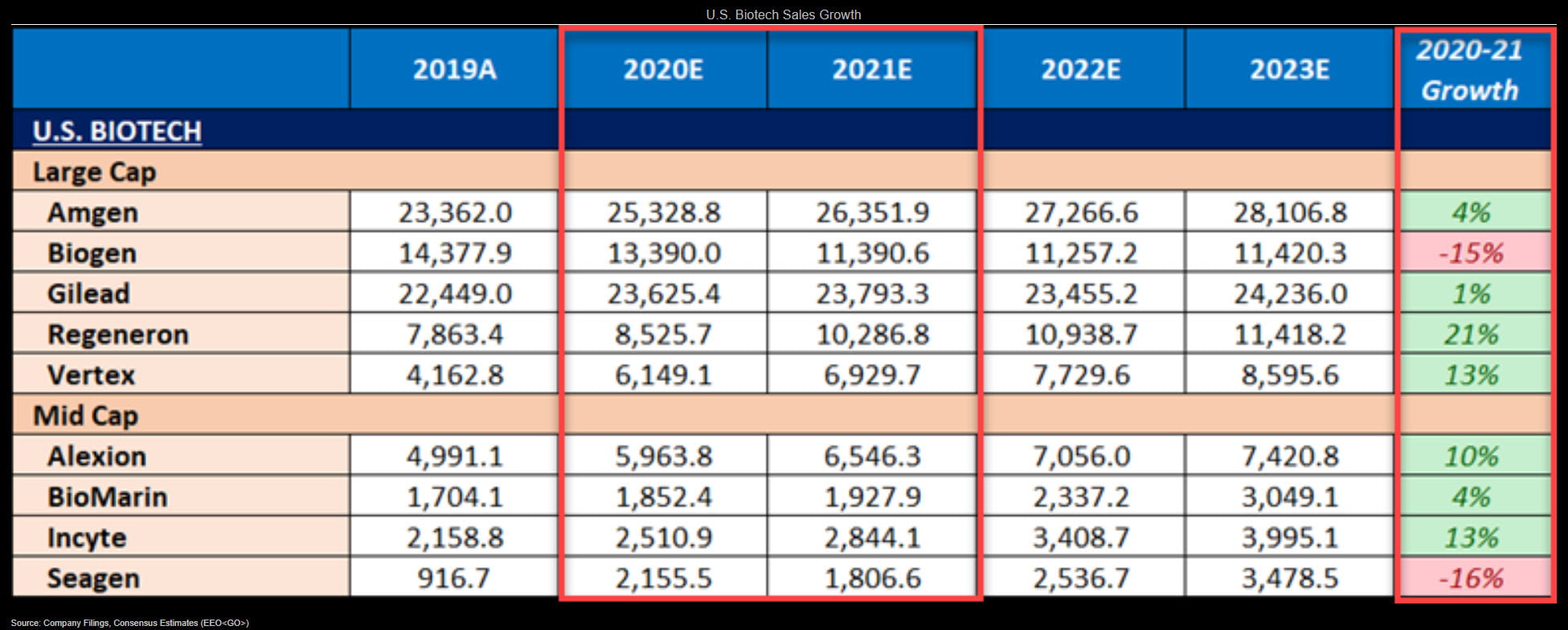

Revenue growth for large and midcap U.S. biotechs looks like a mixed bag in 2021, with Seagen poised for a potential group-leading 26% rate, based on consensus, if $725 million in upfront payments from two Merck deals is backed out of its 2020 numbers. Biogen may slip by 15%. Ongoing launches of Padcev and Tukysa are Seagen's main sources of top-line growth. Incyte, Regeneron and Vertex could see respectable double-digit gains. Continued growth for Jakafi and contributions from Monjuvi and possibly ruxolitinib cream may drive Incyte sales, while Regeneron and Vertex will be aided by mainstays Dupixent/Eylea and Trikafta. Regeneron might also be given some credit for its newly authorized Covid-19 antibody cocktail.

Biogen could be hurt by U.S. generics competition to its former top seller, Tecfidera.

U.S. Biotech margins may contract in 2021

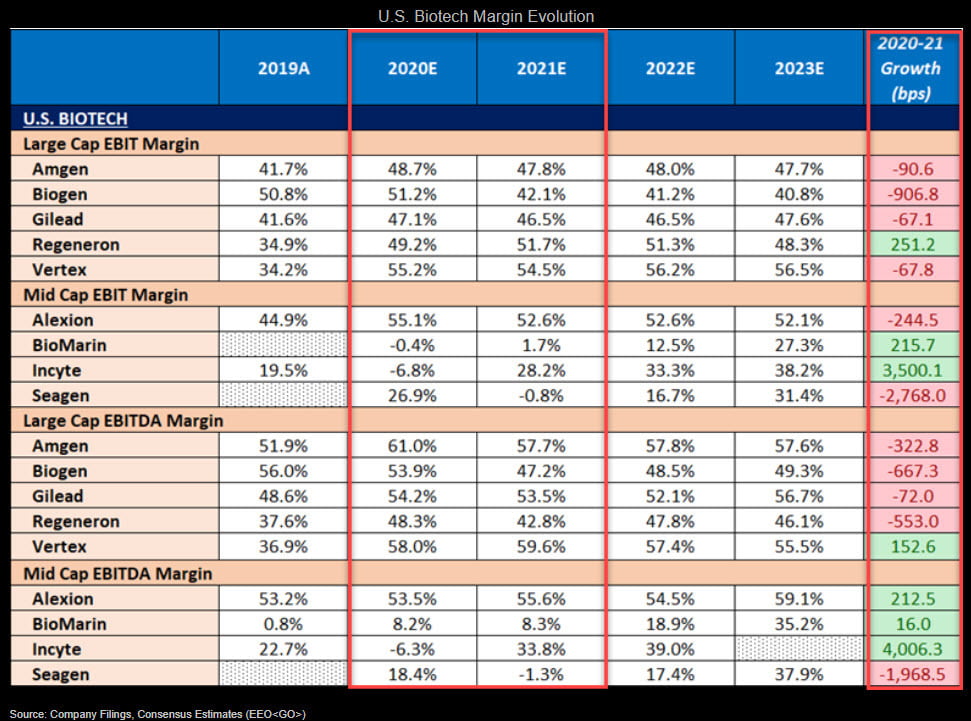

Margins for the U.S. large and midcap commercial-stage biotechs are expected by consensus to contract in 2021 as their pandemic-delayed spending normalizes. Amgen touts its industry-leading operational efficiency, and consensus Ebitda margin of 58% could remain at or near the top with Vertex and Alexion close by. Incyte and Seagen continue to invest heavily in their pipelines. If aducanumab isn't approved or receives a restrictive label, Biogen may need to ramp up R&D spending as well as consider larger-scale business development deals. Vertex may follow suit if its pipeline doesn't begin to produce. Guidance for 2021 coming in early 1Q will help to clarify the margin trajectories for individual companies.

Incyte's apparent margin expansion is magnified by a $750 million upfront R&D payment to partner MorphoSys in 1Q20.

Launch may boost UCB; Generics risk for Lundbeck

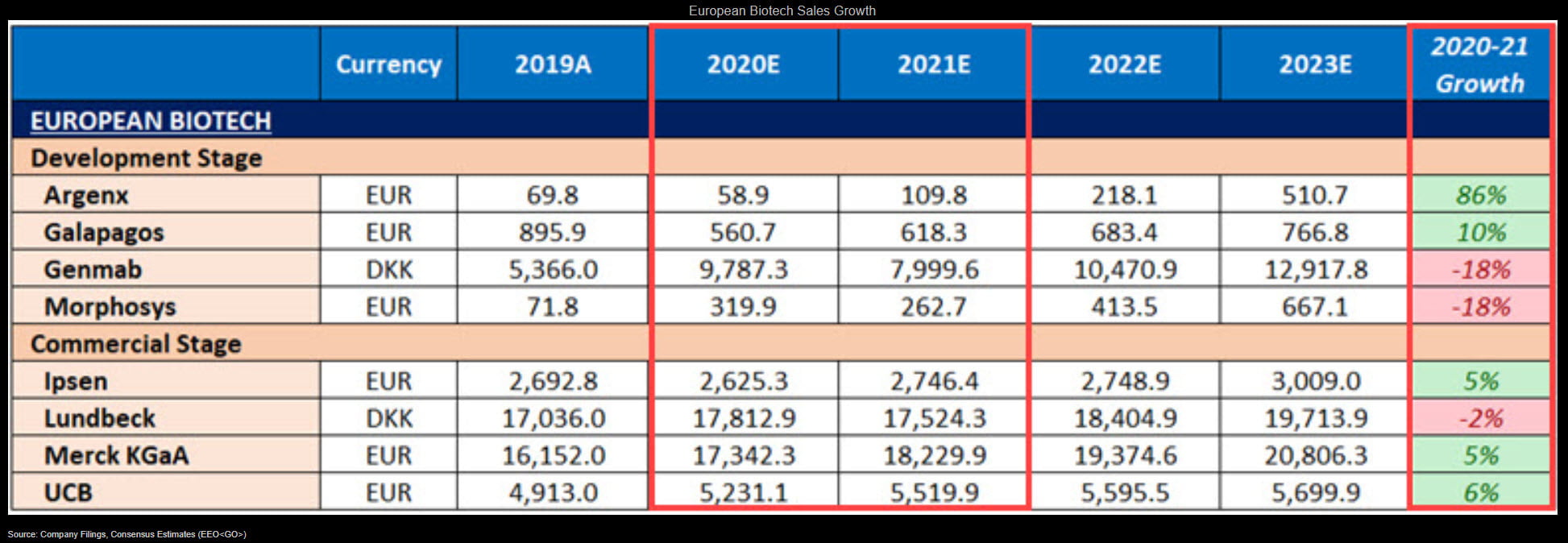

European commercial biotechs under our coverage could deliver mid-single-digit revenue growth in 2021. Momentum for UCB's Briviact, Cimzia and Vimpat may be sustained, with the core franchise bolstered by Evenity and the likely launch of best-in-class bimekizumab. Dysport, which had a weak 2020 due to Covid-19, along with cancer drugs, underpin Ipsen's gains in 2021, while the timing of somatostatin analog generics is a key swing factor. Mavenclad, Bavencio and the recovery in fertility are the pharma drivers for Merck KGaA, whose top line may also benefit from trends within Life Sciences and semiconductors. Lundbeck sales could slip on the Northera patent expiration.

Launches may boost Argenx and Galapagos' revenue, while Genmab and MorphoSys face tough prior-year comparisons following upfront payments in 2020.

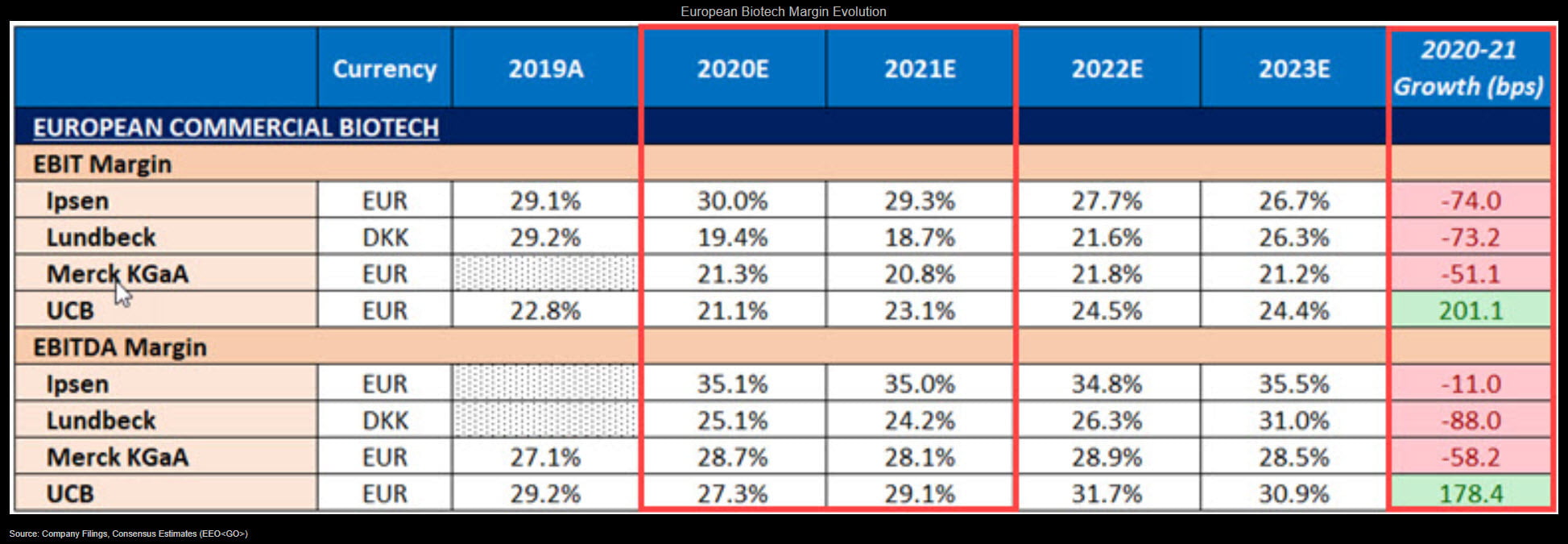

EU Biotech 2021 margin moves may be modest

Ahead of guidance, we believe flat to slight declines in 2021 margins are possible for European biotechs under our coverage, in part due to a normalization in operating costs as pandemic disruption eases. Lundbeck's pressures stem from investments in Vyepti and the pipeline, and the pending loss of exclusivity of Northera, which could lose 50% of its sales that year. Merck KGaA may need to invest to expand capacity to address robust demand in Life Sciences, and drags in Pharma include pricing in China and lower Rebif contribution, which may be partly offset by new launches and a rebound in fertility. Product-mix effects could boost UCB's profitability.

Generics developments faced by Ipsen's top seller Somatuline seem limited for now. Long-term guidance, likely due on Dec. 1, could help frame competitive and margin dynamics.