Valuations of Chinese biotech companies have outperformed Asian peers amid the pandemic, and we believe their robust oncology drug pipelines may widen their lead in 2021. Henlius has led sales growth in 2020, yet Innovent and Junshi Bio's quick ramp-up of PD-1 drugs may lead to larger sales gains in 2021.

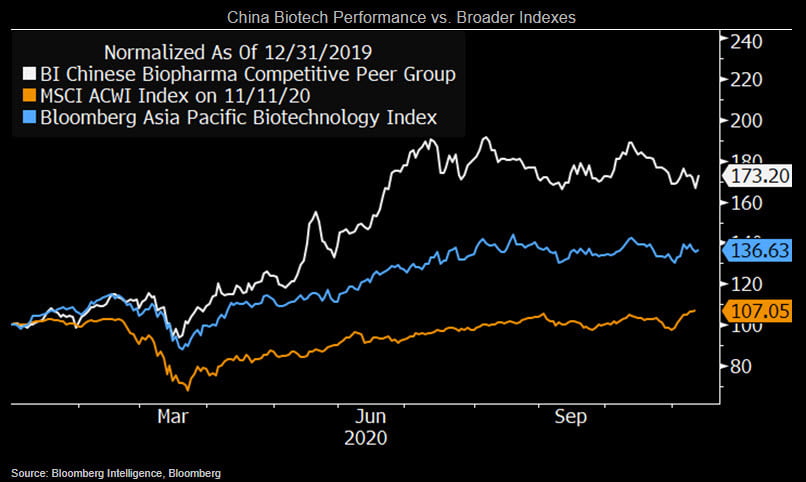

Covid-19 control aided Biotech sentiment

China's management of Covid-19 may have been the main reason its biotech firms' valuations have outperformed Asia peers this year. The government's tough measures shortened delays of clinical trials and allowed studies to resume recruiting. Shares quickly rebounded from the slump in March and outpaced gains in the Bloomberg Asia Pacific Biotechnology Index, in line with a recovery in hospital operations and sustained drug distribution and retail activity. Wuxi AppTec may help lift sentiment in the sector as its CDMO business' global networks helped manage risks from the pandemic, and as China's drug regulations continue to benefit outsourced service providers. CanSino Bio is carrying out phase 3 trials of its Ad5-nCov, which could compete as a Covid-19 vaccine.

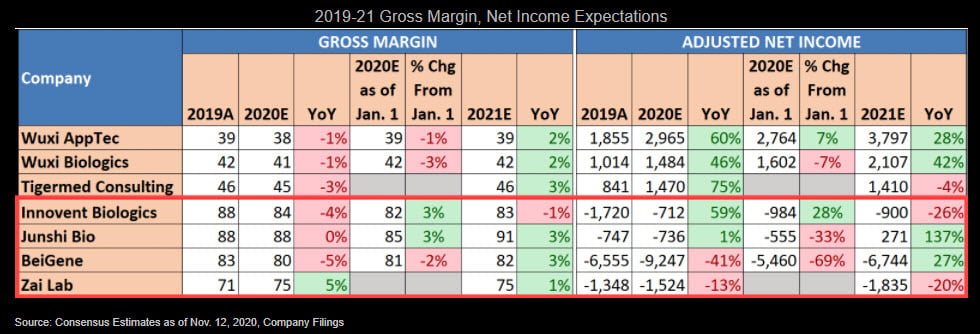

Innovent, Junshi may lead sales growth

Among China biotech firms with annual revenue above 1 billion yuan, Innovent and Junshi Bio may lead sales growth through 2021, given the country's high demand for PD-1 drugs and lower prices than global rivals. Junshi's first mover advantage gave it a slight lead time in label expansion and Innovent's first-line lung cancer therapy approved by Chinese regulators could further enhance sales prospects for Tyvyt, in addition to its inclusion in the national reimbursement drug list. Henlius' biosimilars of Rituximab and Herceptin may address China's sizeable patient pool and be more affordable than branded drugs, contributing to robust growth in 2021. Zai Lab's PARP inhibitor, Zejula, faces tough competition from AstraZeneca's Lynparza, which may impact its penetration -- NRDL inclusion will be key to accelerating growth.

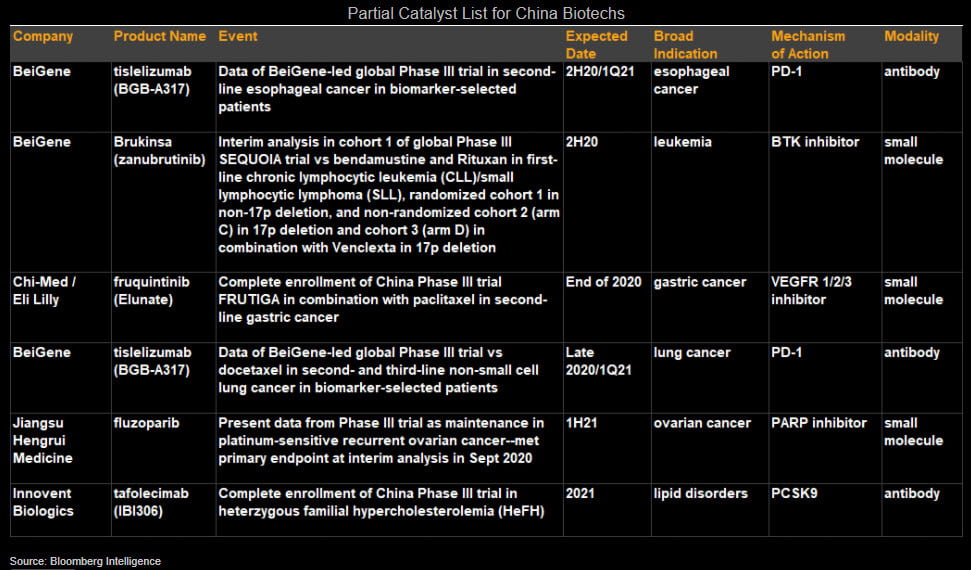

Oncology characterizes China Biotech catalysts

Cancer therapies such as PD-1/L1 drugs, CDK4/6 inhibitors and PARP inhibitors provide the most promise for China biopharmaceutical companies. The principle behind candidate selection is still to target the most sizable patient pool, though strategies may vary. Sino Biopharm's PD-1 drug, co-developed with Akeso Biopharm, shows potential for longer efficacy via a slower rate of antigen binding and dissociation, and is pending approval for classic Hodgkin's lymphoma, while Henlius' PD-1 candidate is still in early stages. Hengrui aims to seek regulatory approval for its self-developed CDK4/6 inhibitor as early as 1Q21, with Genor Bio's licensed-in CDK4/6 inhibitor following closely. BeiGene's PARP inhibitor, pamiparib, has shown preliminary efficacy in ovarian cancer, and could win regulatory approval next year.

Biotechs wrestle with R&D costs, sales delays

China biotech earnings may be less resilient than those of contract manufacturing organizations and contract development and manufacturing organizations as maturing biotechs mainly rely on milestone payments and single product sales. Soaring R&D expenses and delays in ramping up sales in 2020 may delay biotechs' earnings improvement to 2021 or later. Junshi Bio's consensus for 2020 profit fell 33%, and BeiGene's 69%, since the start of the year through Nov. 12. Even Innovent, which has shown exceptional revenue growth so far this year, may face profit pressure in 2021. Biotechs typically have higher gross margins than CROs and CDMOs even though both can be affected by price hikes of active pharmaceutical ingredients (APIs). Overcapacity in some generic APIs and a manufacturing recovery in China may moderate such increases.