EU industrials hit by energy prices, US remains resilient

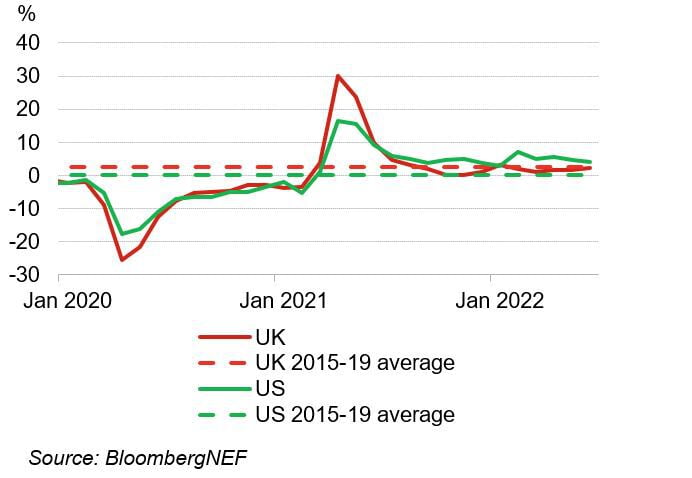

UK and US industrial production year-on-year

Recession risks and cost inflation have all taken a toll on European industrials. The outcome is that industrial demand for carbon allowances is lower for 2022-23 – at levels below those predicted by the market. US industrials appear to be resilient so far.

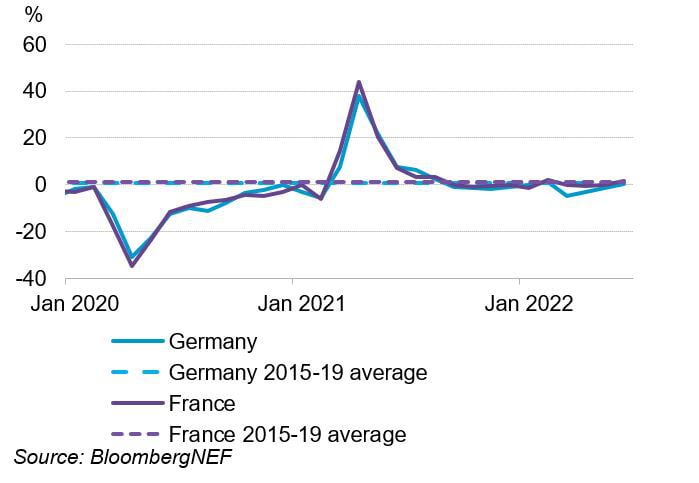

Year-on-year growth in industrial manufacturing production is hovering around the 2015-19 average for Germany, the UK and France. Meanwhile, US industrial production remains above the 2015-19 average

Germany and France industrial production year-on-year

Lower industrial production is bearish for the carbon price in the near term, as fewer allowances are needed. In the longer term, the outcome is typically bullish as investment into longer-term decarbonization is put on hold.

Fears of industrial demand destruction and the impact on emissions unleashed a plunge in European carbon prices in July. However, that price movement appears to have been an overreaction, as indicators are not yet showing high levels of demand destruction – ‘high’ is considered to be around 15% or more. In addition, EU countries still have state aid in their arsenal to support industries in emergency situations. That said, industrial demand remains a key risk for the European carbon market in 2022-23.

Created with Sketch.