Summer LNG trade flows Europe LNG scenarios LNG supply risks

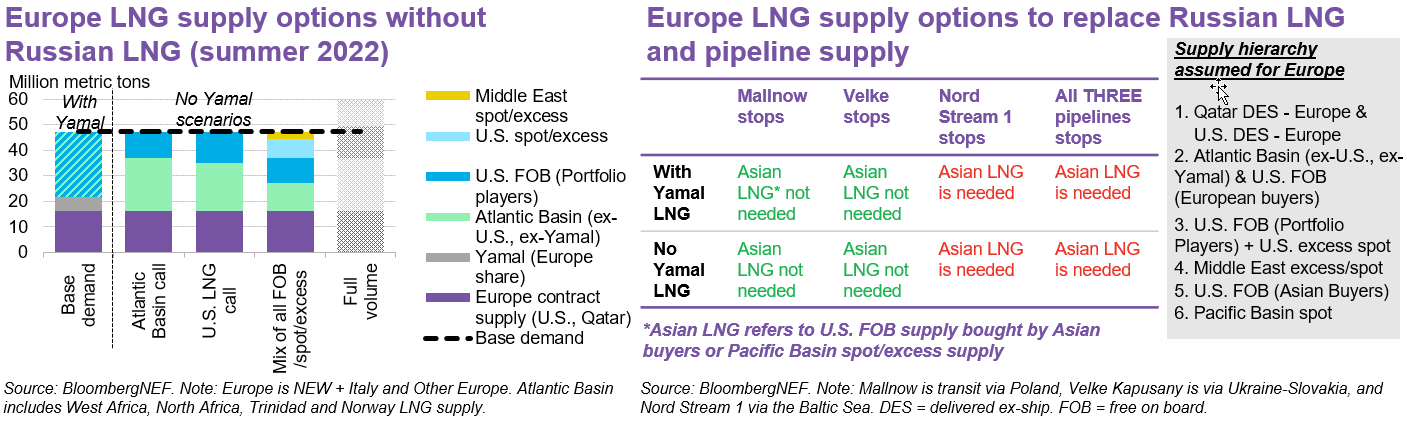

If Europe decides to stop allowing Russian LNG shipments to arrive, it would need to tap into a mix of Atlantic Basin supply, U.S. LNG FOB supply from portfolio players and spot/excess supply from the U.S. and Middle East. This scenario is manageable, but not necessarily cheap.

The situation turns dire if Europe needs to backfill pipeline flows. Nord Stream 1 is assumed to provide more than half of Russian pipeline imports to Europe in BNEF’s base case. As such, Europe will need Asian LNG* supply to backfill gas if flows via Nord Stream 1 stop, regardless whether Russian LNG shipments continue to arrive or not. If flows via Ukraine or Poland grind to a halt, there may not necessarily be a need to see Asian LNG supply diversions to Europe, as there would be enough supply within the Atlantic.

There is no situation where Europe wouldn’t need to encroach on Asian LNG supply if Russia turns off all the taps. However, BNEF analysis indicates that there isn’t enough Northwest Europe LNG import capacity to cover a three-pipe backfill or even a Nord Stream 1 halt at certain periods.

Asian buyers are unlikely to relinquish their supply amid fast depleting LNG inventory levels in Japan and Korea, where utilities are heavily tapping LNG stockpiles to meet demand as spot LNG prices remain prohibitively high. Hence, in a scenario where Russia halts flows through Nord Stream 1, it would send Asia and Europe into an intense competition for LNG, which would see even more gas price volatility than in 1Q 2022.