Gas storage levels Gas supply Gas demand

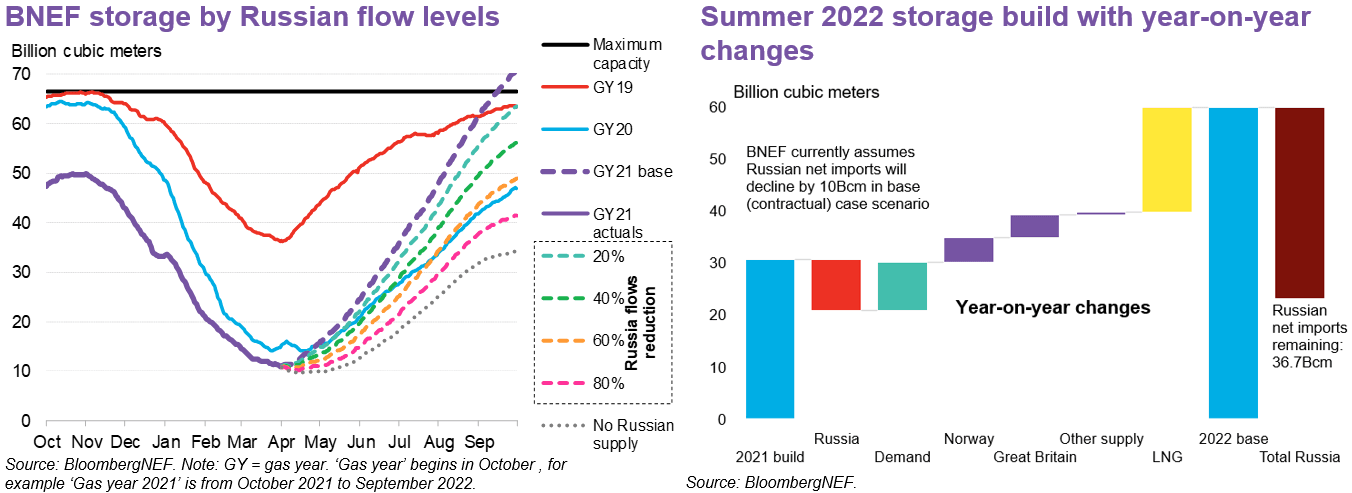

Under BNEF’s base case scenario, Europe could have more than enough gas to completely fill its storage by October 1, 2022. This base case is based on Russian flows into Europe being around likely minimum contracted levels. This represents an inflow to Europe on the three-pipe network averaging around 260Mcm/d – some 40Mcm/d below summer 2021 levels and around the average for March 2022 to date. The challenge Europe would face to build stocks would be even greater should net Russian imports in summer be significantly below 36.7Bcm.

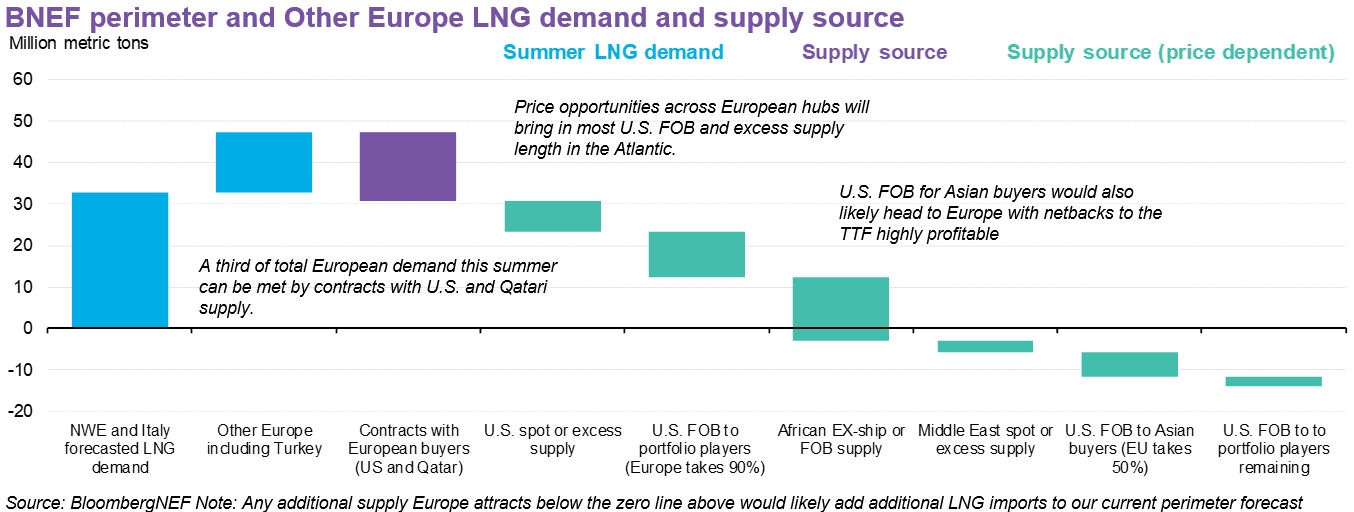

Additionally, this depends on the TTF maintaining a steady premium to the JKM throughout the summer and thus attracting significant volumes of LNG to Europe. BNEFs current LNG view is based on the high prices currently seen across the forward curve and requires significant Asian demand destruction.

Both of these assumptions come with significant downside risk. This is what the market has to price in if gas storage levels are to hit or exceed the 90% targeted by the EU under its RePowerEU plan. Furthermore, the risk that Russian flows are impacted next winter is what has driven the EU to set such a high storage target and what is keeping prices across the forward curve high.

In the event that storage levels in Europe fill at a rate on track to completely fill storage or above, there is significant risk of a downward price correction. The first way the market will likely balance is that the TTF will fall below the JKM, with LNG flows heading back toward Asia and lowering European supply.

Almost half of BNEF Europe perimeter summer demand could be met by contracts between European buyers and U.S. and Qatari sellers. However, a considerable chunk of this supply would also go to feeding large import markets such as Spain and Turkey.

Appetite for U.S. LNG from both Turkey and Spain has been substantial lately, with Turkey accounting for more than 45% of U.S. LNG shipped to other European markets outside of BNEF perimeter.

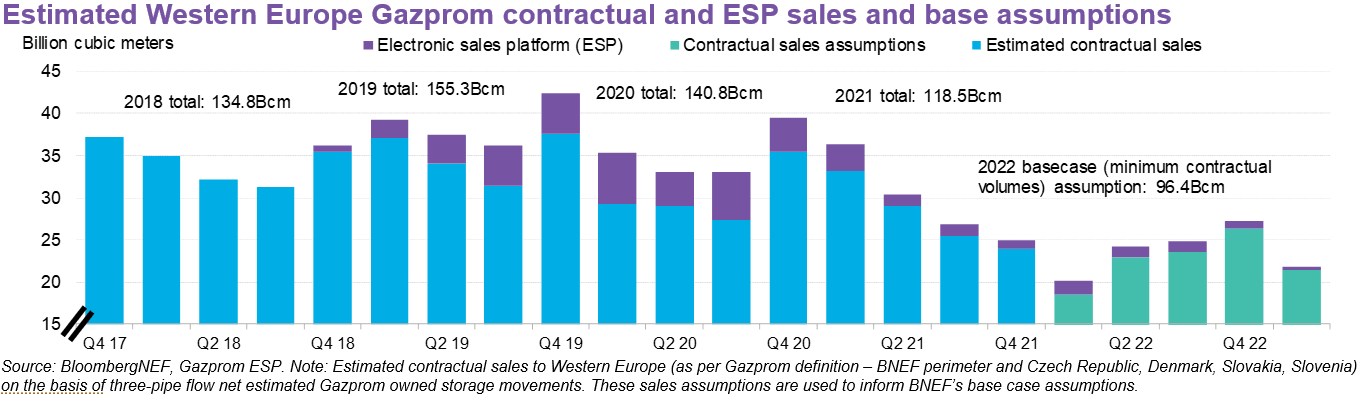

As the grounding for our base Russian flow forecast, BNEF assumes that contractual sales to Western Europe will total around 92Bcm in calendar year 2022 – likely around the minimum contractual volume. BNEF has previously argued that Gazprom will seek to stick to these minimum contractual obligations, as failure to do so would have negative implications for Russia and Gazprom being seen as reliable suppliers of natural gas. Additionally, as such minimum volumes are likely take-or-pay, European buyers also seem unlikely to go below these volumes unless a legal basis for not paying is found.

Sanctions: BNEF maintains it is unlikely that Europe will sanction the Russian energy sector directly given its reliance on energy imports. However, as measures to reduce reliance on Russian imports develop, the chance of this step being taken increases.

‘Self-sanctioning’ and price risk: Increasing sanctions or ESG risk in purchasing Russian gas may lead to reductions in offtake from buyers. There are reports of U.K. buyers seeking to withdraw from smaller contracts with Gazprom Marketing and Trading – a Gazprom subsidiary – to the extent that the subsidiary may go into special administration. BNEF has also highlighted how Gazprom contract sales pricing and price evolution might lead to lower-than-expected flows, especially if buyers have greater downward flexibility annually than assumed.

Physical disruption to flows: As the war in Ukraine continues, the chances of damage to transit pipelines increases. Gazprom does, however, have around 160Mcm/d of capacity on Nord Stream 1 and around 90Mcm/d through Kondratki (upstream of Mallnow), allowing for three-pipe flow of 250Mcm/d of gas into BNEF’s perimeter. This is most of the 266Mcm/d and 286Mcm/d of inflow assumed for the coming summer and winter, respectively.