The European Union’s proposal this week to ban Russian coal imports puts further strain on the market, as power producers may need to turn more to gas to generate electricity.

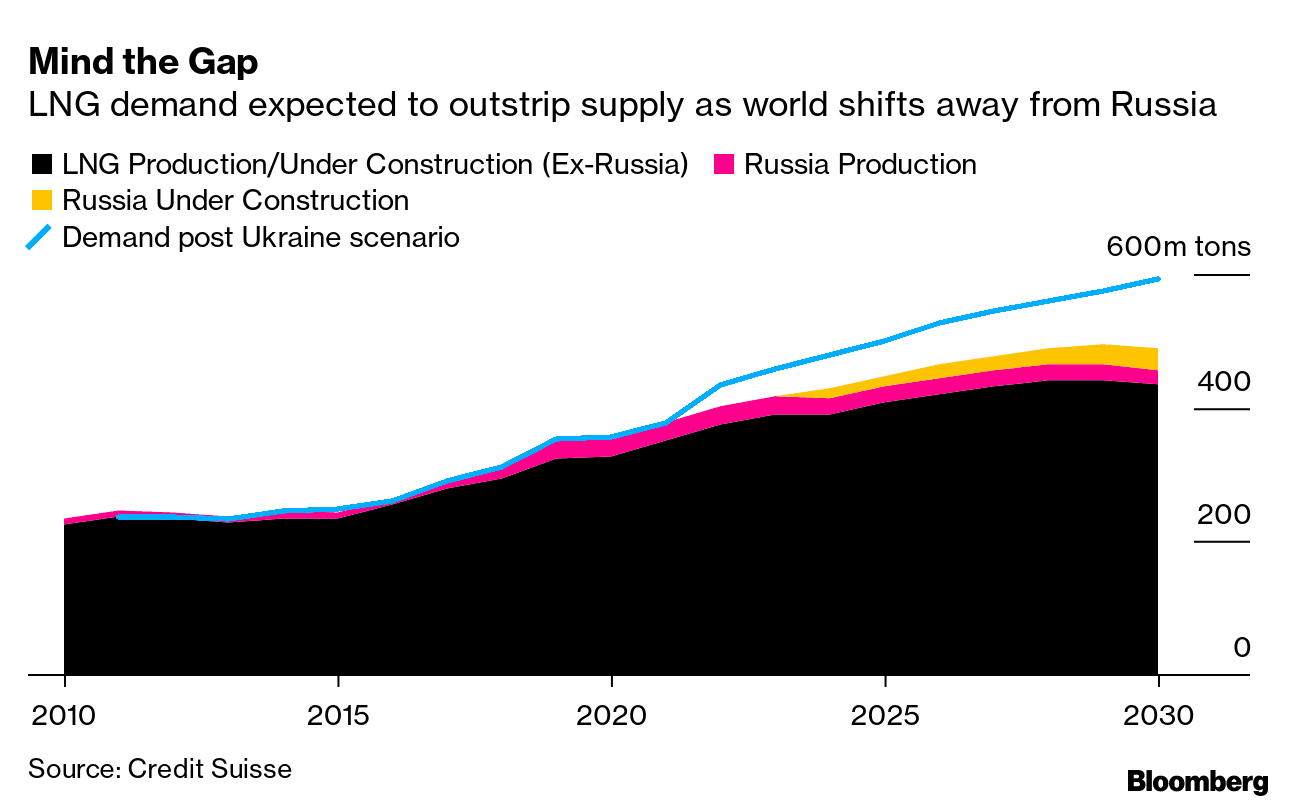

Longer term, the LNG demand-supply balance is expected to get more out of whack, especially if Russian gas is removed. The global market could be short nearly 100 million tons per year by the middle of the decade, according to a Credit Suisse report last month. That’s equal to more than the annual demand of China, the world’s top buyer of LNG.

“Even before the Russia-Ukraine crisis, the global LNG market was tight with record high prices,” said James Taverner, a senior director at S&P Global. “Market tightness is likely to persist over the next few years. Prices are likely to continue experiencing wild swings from day to day.”

Already, natural gas spot prices are so high that the world’s top buyers in North Asia are choosing not to refill inventories with additional overseas purchases. They’re instead gambling that this summer will be mild, or a peace deal between Russia and Ukraine will result in a price drop, said traders, who requested anonymity to discuss private details.

LNG importers in China and India have drastically cut back spot purchases, and are instead maximizing domestic supply and consuming gas in storage, traders said. This strategy will help to save money, but comes with an enormous risk that allows little room for surprises -- a bet that hasn’t paid off recently.

If there is a sudden spike in demand for gas, or if a contracted shipment isn’t able to be delivered due to a production issue, some of Asia’s top consumers may be short of gas this summer or next winter. They will be forced to go back into the spot market and buy very expensive shipments of the fuel, or curtail gas deliveries to customers at home.