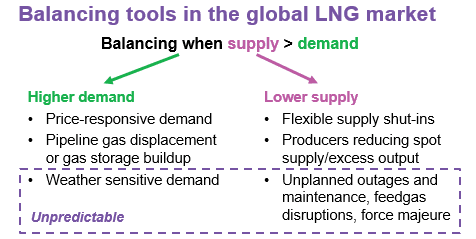

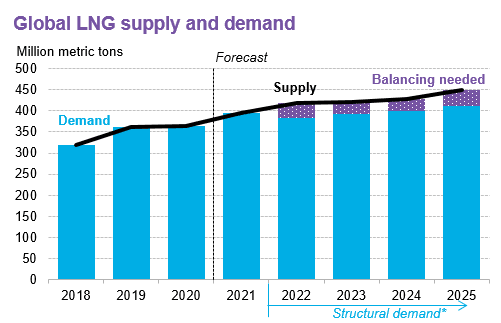

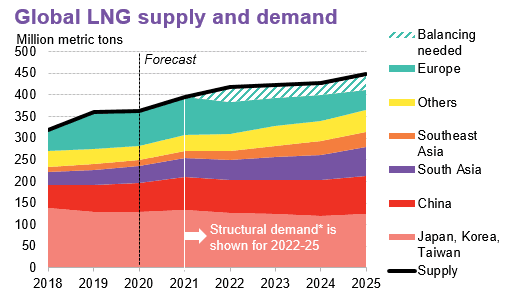

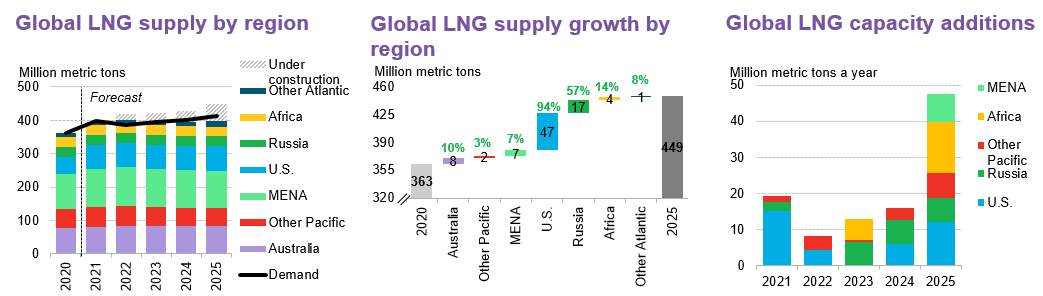

The global LNG market is likely to be oversupplied until 2025. Supply growth exceeds the increase in LNG demand, with a new wave of projects expected to be commissioned over the next five years. Europe will continue to be a key balancing market, but demand from Asia could respond to prices and other factors.

Source: BloombergNEF. Note: *Structural demand is the demand based on current prices and 30-year weather average. For 2021, demand forecast assumes Northwest Europe and Italy takes all volumes, or excess supply, needed to balance the market after non-European demand is met.

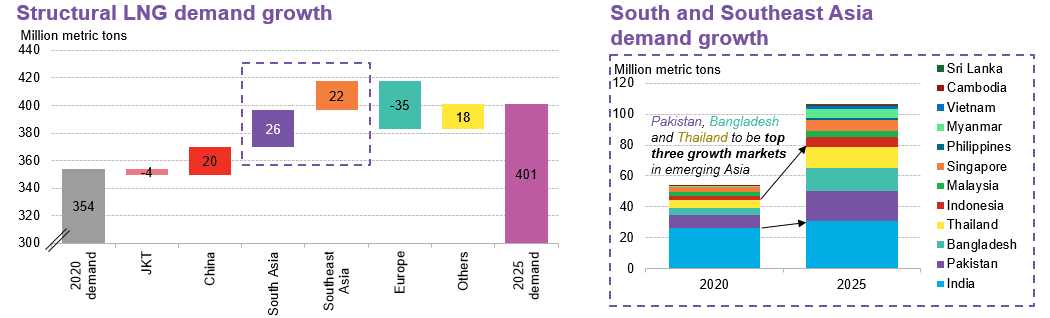

Source: BloombergNEF. Note: ‘Others’ include Middle East, Americas, new markets, bunkering, and operational/voyage LNG losses (such as boil-off). *Structural demand is based on normal weather (30-year averages) and current futures prices.

Source: BloombergNEF. Note: JKT is Japan, Korea and Taiwan. ‘Others’ include Middle East, Americas, new markets and bunkering. *Structural demand is based on normal weather (30-year averages) and current futures prices.

Source: BloombergNEF, Bloomberg Terminal’s AHOY JOURNEY . Note: MENA refers to Middle East and North Africa, Refer to the appendix to see countries in region groupings. Percentages shown represent growth from 2020 levels per region (middle chart). Capacity additions show full nameplate capacity in commissioning year.