Global balance

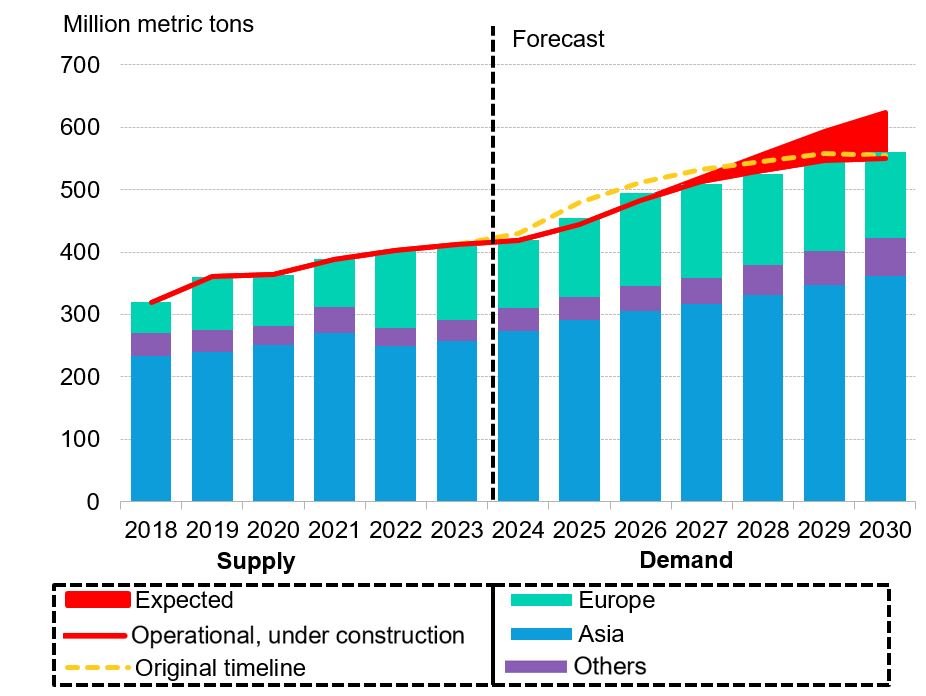

Global LNG supply and demand

Source: BloombergNEF. Note: ‘Others’ includes the Middle East, Americas, Africa, other markets, bunkering and operational/voyage LNG losses (such as boil-off).

*See BNEF’s Global LNG Supply Outlook 2030 for list of expected projects.

Demand projections based on 10-year average weather and average June 2024 futures prices.

Supply estimates based on operational, under-construction and expected* projects.

The global LNG market is on track to see more supply than demand from 2027 onwards. It is poised to become increasingly oversupplied by the end of this decade in the base case, with expected supply 63 million tons higher than demand in 2030, as new liquefaction projects are commissioned. However, project delays and sanctions have decreased the extent of the oversupply anticipated towards the end of this decade.

The global balance will still be tight in the next two years despite a record number of projects reaching a final investment decision (FID) in 2019. BNEF analysis suggests supply would be 20 million to 36 million tons higher than the base case over 2025-27 if under-construction liquefaction projects adhered to the original timelines announced during their FID. If projects currently under construction get further delayed by six to 12 months, 15 million to 43 million tons of supply in 2025-26 could be shifted to later years.

Current sanctions on Russia and buyers’ resulting reluctance to renew Russian supply contracts expiring near the end of decade have removed roughly 21 million tons of supply by 2030 in the base case, compared to a no sanctions scenario.

Operational and under-construction LNG projects will be able to push total available supply above demand estimates over 2027-28, but additional supply will be needed to cover demand from 2029 onwards in the base case. Such supply is expected to come from a long list of projects from Qatar, the US and Mexico, as well as floating LNG projects.

LNG demand is set to see fast growth over the next two years thanks to decarbonization efforts across the world prompting a shift away from coal, and infrastructure expansion in Asia. Growth is likely to slow afterwards as Europe’s LNG demand declines due to lower gas burn for power.

Less than a third of the expected demand increase from Asia over 2023 to 2030 is covered by contracts, with South Korea and emerging Asian markets driving most of the difference between demand and contract levels. Europe’s uncontracted demand will also increase by roughly 40% over 2023 to 2030. European buyers are likely to have a lower appetite for additional long-term contracts than Asian counterparts due to a stronger policy emphasis on reaching net-zero emissions, which weakens the outlook for gas demand beyond 2030.