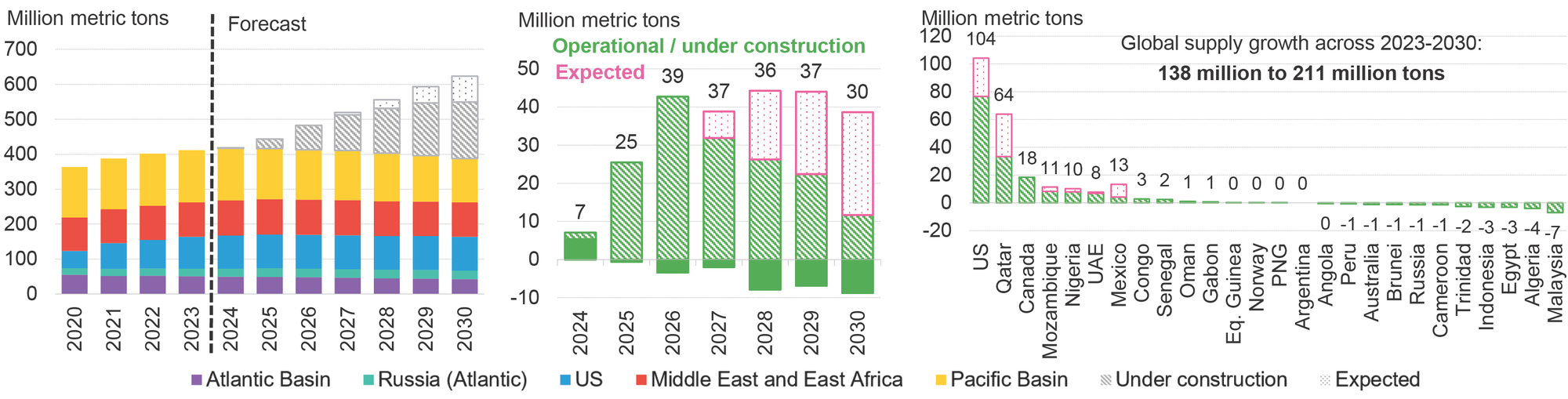

Global LNG supply

Global LNG supply Outlook

Annual change, by region

Supply change from 2023-2030, by market

Source: BloombergNEF, Bloomberg Terminal’s AHOY JOURNEY . Note: PNG refers to Papua New Guinea, Eq. Guinea refers to Equatorial Guinea, UAE refers to United Arab Emirates.

BNEF expects global LNG supply in 2030 from operational and under-construction projects to grow by 33% from 2023, to 550 million tons. A long list of projects aiming to take a final investment decision could provide an additional 74 million tons of LNG in 2030, bringing total expected supply to 623 million tons. Some of the anticipated supply growth will be offset by declining feedgas flows to aging plants across the Pacific and Atlantic Basin, amid depleting reserves.

Under construction: About 162 million tons of LNG supply in 2030 is estimated to come from projects currently under construction, with the majority of the capacity in the US and Qatar. A third of under-construction projects are expansion projects. The timely completion of projects under construction is crucial for the global LNG balance. Five projects in the US are currently being built, which will add 61 million tons of supply in 2030. The North Field East expansion will boost Qatari supply by 42% by 2030 from last year’s levels. Russia will see limited growth as only Train 1 of Arctic LNG 2 is assumed to start, with reduced utilization levels. See the next slide for sanctions-related scenarios for the supply of Russian LNG.

Expected: Projects that have the best chance of a place on the approved list include expansions by reputable LNG developers, smaller, faster development options, and projects that have secured firm buyers. Qatar will top such additions, followed by the US, Mexico and floating LNG projects, based on BNEF’s evaluation.