Global supply scenarios

Global LNG supply scenarios

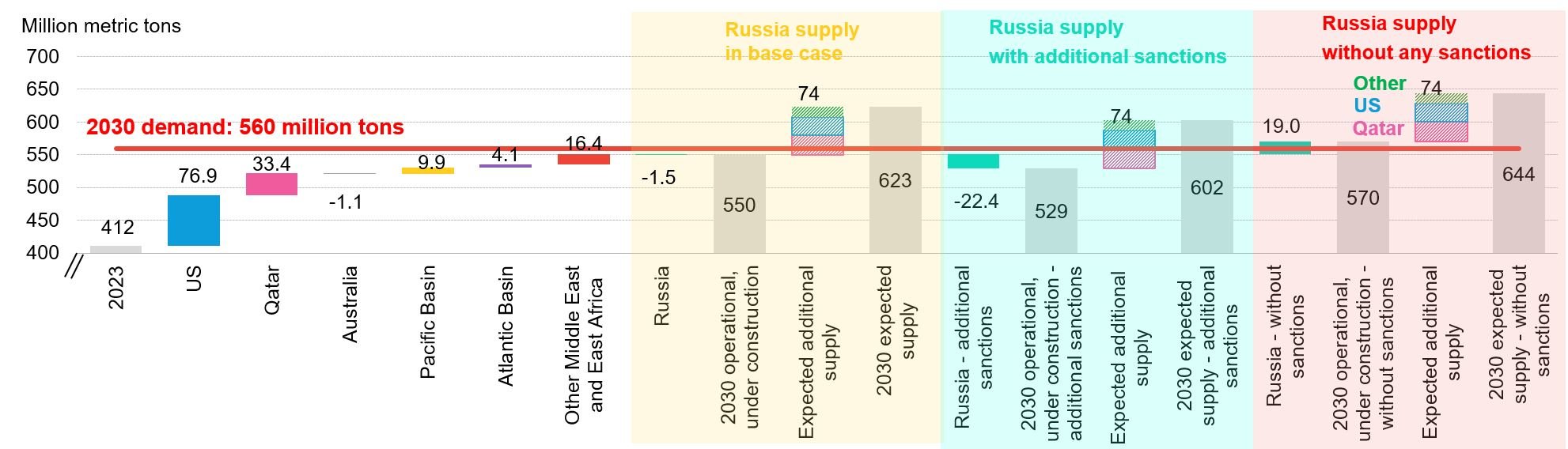

Source: BloombergNEF, Bloomberg Terminal’s AHOY JOURNEY . Note: Russia here includes all Russian projects.

The extent of the impact of sanctions on Russian projects will play a key role in shaping the global LNG balance. Additional sanctions may help expected US LNG projects get approved if they successfully reduce LNG loadings from Russia, bringing 2030 global supply estimates from operational and under-construction projects below our LNG demand projection of 560 million tons. However, if Russian projects were to operate normally without any sanctions, BNEF sees a lower probability of new supply coming from the expected projects list, as supply in 2030 from operational and under-construction projects would exceed our demand estimate.

Under the base case, LNG supply from Russia drops by 1.5 million tons by 2030 from last year’s levels, reflecting current sanctions on Arctic 2 LNG and a decline in Sakhalin volumes post-2028 as contracts expire with existing offtakers. For detailed assumptions on Russian supply, see BNEF’s Global LNG Supply Outlook 2030. Total global supply from operational and under-construction projects will reach almost a similar level as global demand at the end of the decade. This means limited additional new supply capacity from the US is needed in 2030, assuming Qatari expansion has a higher chance of approval than US projects due to state backing.

The additional sanctions scenario assumes an outright ban on Russian LNG to Europe, which will take out more than 20 million tons of Russian supply from the balance. The latest EU sanctions to ban transshipments from the bloc’s ports from March 2025 to third countries outside the region will impact Yamal deliveries to Asia. More new supply, apart from Qatar’s expansion project, needs to be in place by 2030, raising the approval chances of US projects.

The scenario without any sanctions assumes the normal operation of all Russian plants, including uninhibited trade flows from Yamal, unaffected contract activities and a normal production ramp-up in the Sakhalin and Arctic 2 projects. Russia, together with other existing and under-construction projects, will be able to satisfy global demand for LNG, lowering the approval likelihood of US projects.