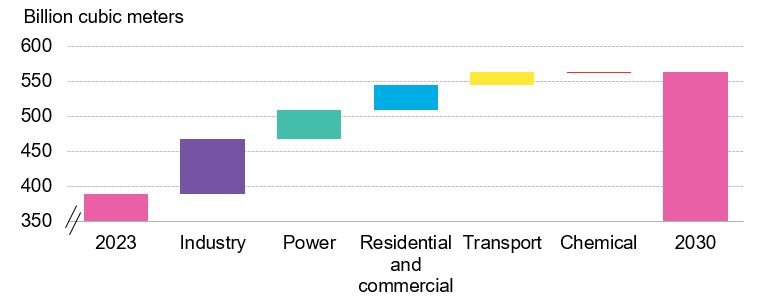

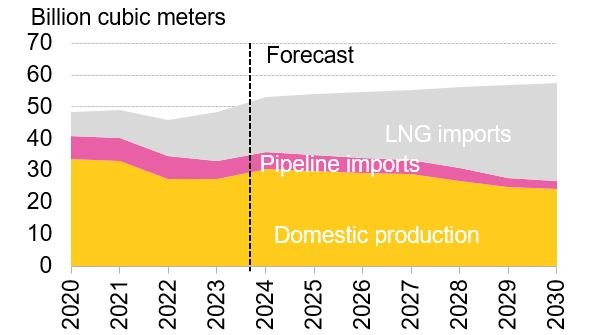

Natural gas demand in mainland China is estimated to remain on an upward trajectory, rising 45% from 2023 to reach 563Bcm in 2030, mostly boosted by emission reduction efforts.

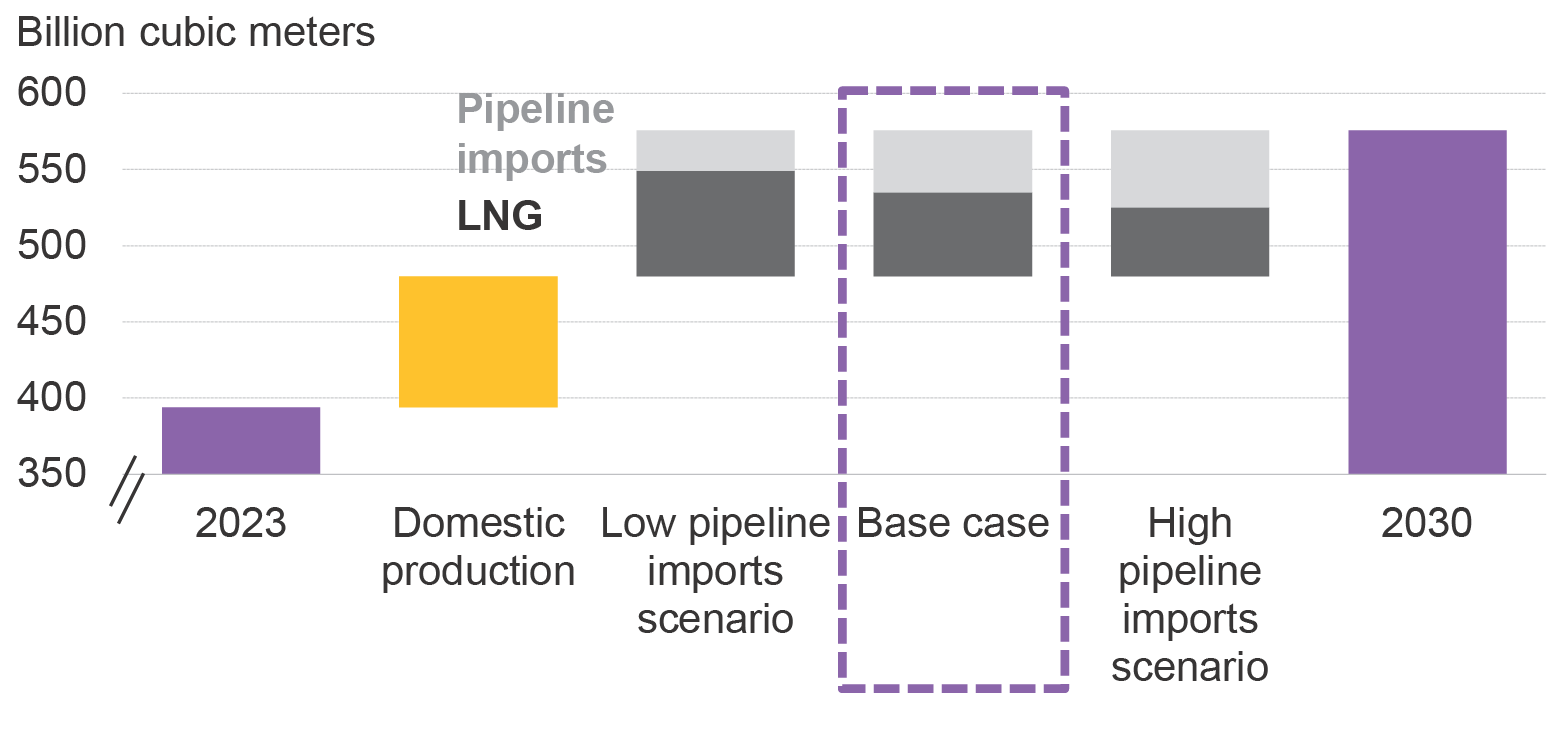

Mainland China is on track to source 576Bcm of gas in 2030, with additional supply from steadily growing domestic gas output and fast-expanding imports with new pipeline supply and LNG contracts.

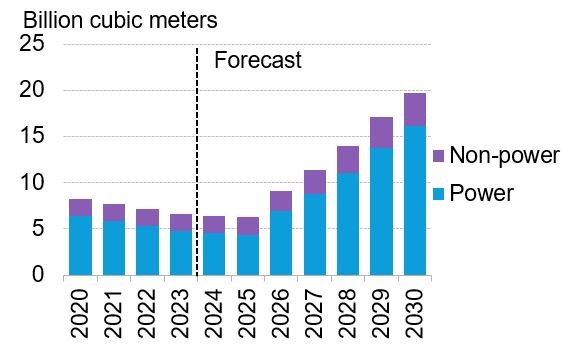

Industry is likely to be the main growth driver due to potential coal-to-gas replacement opportunities to target the government’s goal of peaking emissions by 2030.

The power sector’s demand will follow and is set to grow fast until 2026, as capacity buildout accelerates to decarbonize the coal-heavy electricity supply, meet growing electricity demand and provide flexibility for increased penetration of renewables in the power system.

Residential and commercial sector gas use is set to rise steadily as the gas grid expands amid a higher urbanization rate.

The transport sector is on track to see a spike in gas demand from commercial vehicles thanks to the favorable economics of LNG compared to diesel. Uncertainties remain, however, as an extended property sector downturn could weigh on further overall gas demand growth.

Domestic production will continue to provide most gas supply, with increased exploration and production investment under a strong government push to ensure supply security.

Pipeline imports could vary by between 94-118Bcm in 2030, depending on the commissioning timelines of new Central Asia and Russian pipelines. The Far Eastern Route is expected to be commissioned around 2027 and Central Asia Line D is assumed to be operational around 2029 in BNEF’s base case.

LNG imports may increase by 40 million to 110 million tons from 2023 to 2030 with increasing LNG contracts, infrastructure expansion and more market players. But volumes will stay highly dependent on the progress of planned pipeline import projects.

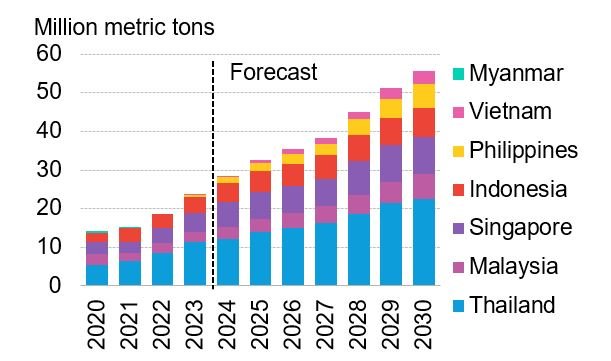

Southeast Asia’s LNG imports are set to reach 55.7 million tons by 2030, more than twice last year’s levels. Thailand is on track to be the top growth market by volume, followed by the Philippines. BNEF expects Vietnam’s growth to be constrained by the slow progress of planned LNG-to-power projects.

Thailand’s LNG imports will increase as gas demand for power and industry rise, while other supply sources, such as domestic output and pipeline imports from Myanmar, fall. Gas production is likely to stay relatively flat over 2025-27 as state-owned PTT aims to maintain output at the Erawan, Arthit and Bangkot fields. Output may then decline as Chevron’s production license for the Pailin field expires in 2028. PTT’s contract with the Yadana field in Myanmar will expire in 2028, lowering pipeline imports. If it extends this contract, Thailand’s LNG needs will be below our base-case forecast.

The Philippines’ LNG imports will rise as it will run out of domestic gas by 2027, whereas gas demand for power is set to increase. A joint venture between Meralco PowerGen, Aboitiz Power and San Miguel Global Power is planning to build a new 1.3 gigawatt LNG-fired plant. Meralco PowerGen is separately working on another 2.4 gigawatt gas power plant in Atimonan, Quezon.