By Maggie Kuang, BloombergNEF

There will be increase in demand in response to low LNG prices, largely from North Asia and Europe. Other smaller markets will see little demand response when spot prices are low due to infrastructure and structural constraints.

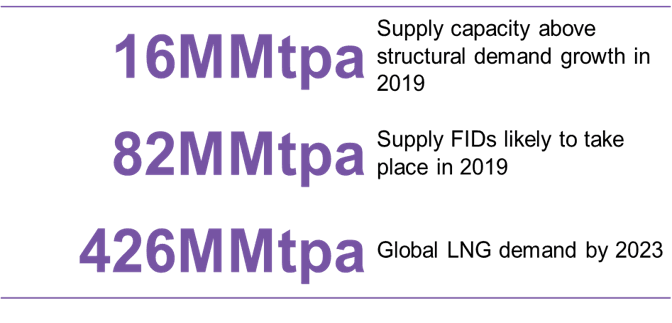

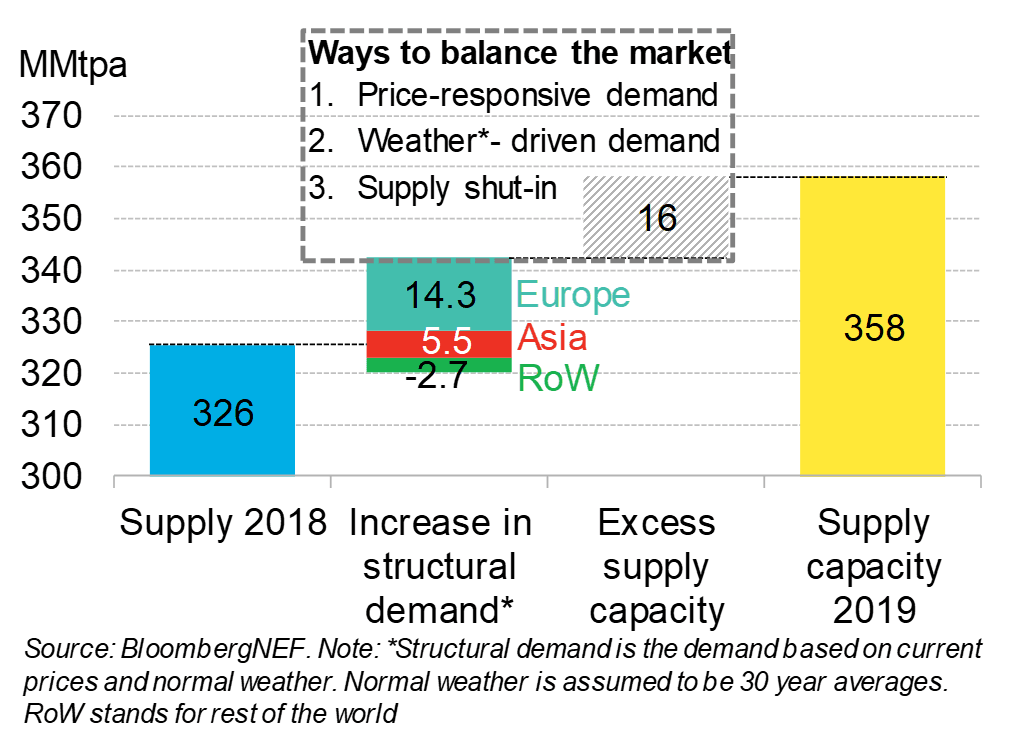

According to the report Global LNG Outlook 2019-23, the structural LNG demand* is set to reach 342MMtpa in 2019, up by 17MMtpa from 2018. Europe will surpass Asia in terms of demand growth in 2019 from 2018.

BloombergNEF expects Europe’s LNG demand to expand by 14.3MMt whereas Asian LNG demand will rise only by 5.5MMt in 2019 as compared to 2018. The structural demand growth however will not be enough to take all the additional supply capacity, of 33MMtpa, anticipated for the year.

*Structural demand is the demand based on current prices and normal weather. Normal weather is assumed to be 30 years averages.

Oversupply may start in 2Q 2019 and persist until 1Q 2020. Two types of demand response can help to absorb the 16MMt excess supply – 1) price-responsive demand which will come from power and industry sector when prices are low, and 2) weather-driven demand which will be created if weather is warmer or colder than normal weather. If demand response to price and weather is not sufficient to absorb the LNG supply surplus, U.S. supply would need to be curtailed.

The global LNG market faces oversupply in 2019