By Abishek Rohatgi, BloombergNEF

In 2023, structural demand could exceed operational supply capacity. Much will depend on Northwest Europe. Projections of steady demand growth there are based on current LNG prices and ignoring that region’s swing buyer role. In reality, LNG prices will likely have to rise to ration supply amongst Europe and less price-sensitive importers in Asia.

China’s will drive demand growth over 2020-21 backed by coal-to-gas switching in inner provinces, pipeline expansion, and rising LNG bunkering demand. However, its appetite for LNG will start to reduce from 2022 as pipeline gas imports ramp up significantly from then.

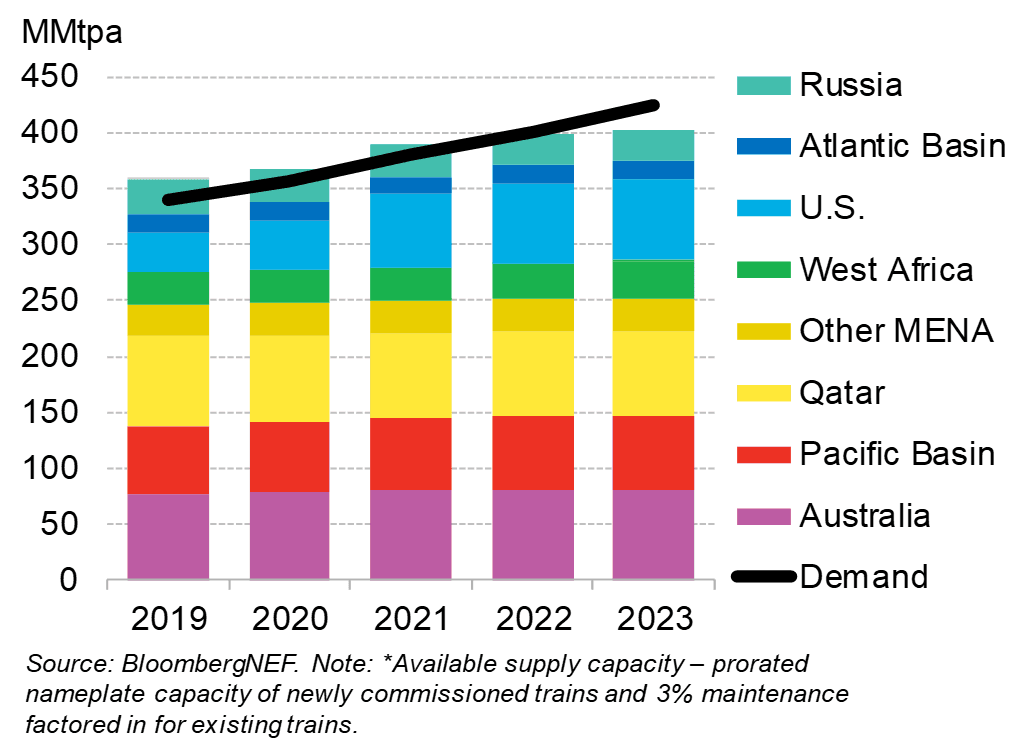

Global LNG supply and demand

Smaller Asian nations such as Thailand, Pakistan and Bangladesh will play increasingly important role post 2021 due to faster depletion of local gas and rising gas demand from power and industry.

The significant LNG demand growth expected in Europe in 2019 means very little upside potential in the region’s structural demand next year.

Lower gas production from U.K., Norwegian and the Netherlands will increase the dependency of European nations on LNG imports from 2021.

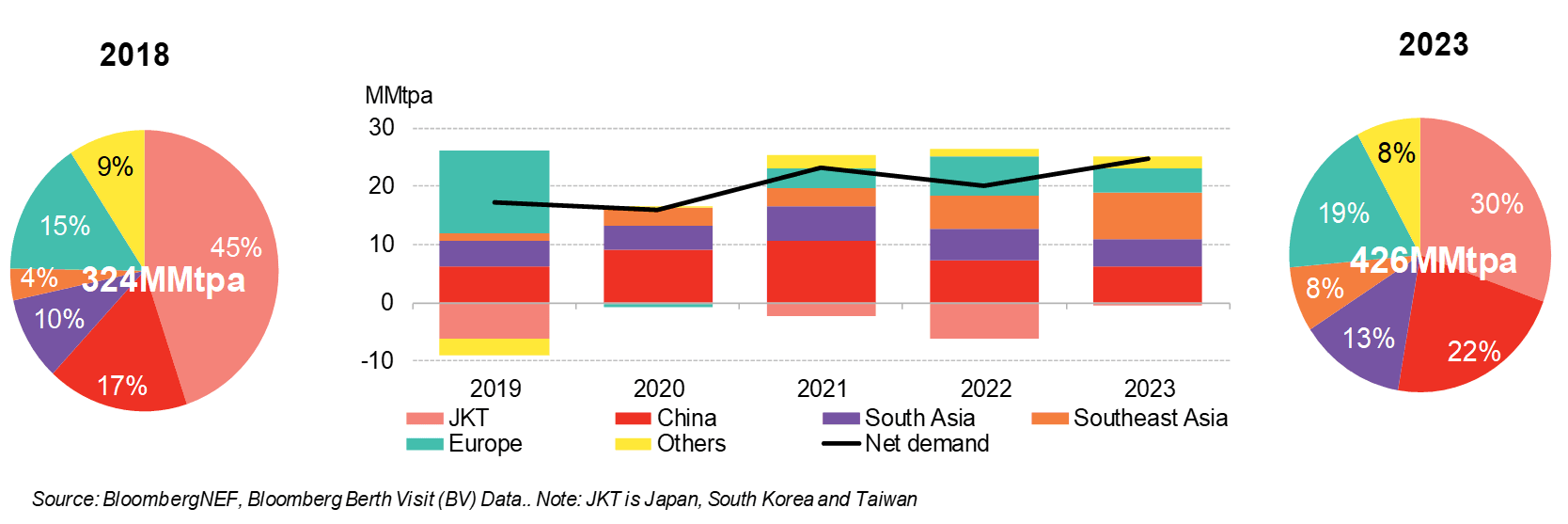

Global LNG demand outlook