Will Kennedy, Executive Editor, Energy and Commodities

Ashish Sethia is BloombergNEF’s Global Head of Commodities. His team analyzes asset valuations and investments, financing and contractual structures, technology evolution, policy developments and demand-supply drivers in natural gas/LNG, oil & petrochemicals, metals & mining, power, coal and carbon markets.

Fauziah Marzuki leads BloombergNEF’s Asia Pacific gas and global LNG coverage. She has over a dozen years of experience in the oil and gas sector spanning corporate strategy, LNG trading and business development in Asia Pacific, upstream oil commercial planning and operations in the Middle East, and lecturing/training.

Any opinions Ashish Sethia and Fauziah Marzuki express are their own.

Will Kennedy: Hello. Welcome to our Q&A on the global gas market. I’ll be moderating a discussion on the outlook for the natural-gas industry with my colleagues from BloombergNEF, Ashish Sethia, global head of commodities, and Fauziah Marzuki, who leads BNEF’s Asia Pacific gas and global LNG coverage.

The global market has seen rock-bottom prices, putting pressure on the profits for the world’s gas producers, but there have been upsides. The slump has allowed gas to undercut coal, pushing up demand around the world. New pipelines and LNG terminals mean a more integrated global market.

We’ll discuss these trends and the impact of the pandemic on the market.

Let’s kick off with a question for both of you. What has been the impact of the pandemic on the global gas market? As we head toward the northern hemisphere’s winter and a potential second wave how do you assess the outlook?

Ashish Sethia: The pandemic is having an unprecedented impact on the global gas market. Gas consumption grew 2.3% in 2019 to reach an all-time high. This growth was propelled by a staggering 13% increase in liquefied natural gas (LNG) imports.

However, 2020 will see an historic 4% fall in global gas demand, much greater than the 2% observed in 2009, on the back of the global financial crisis.

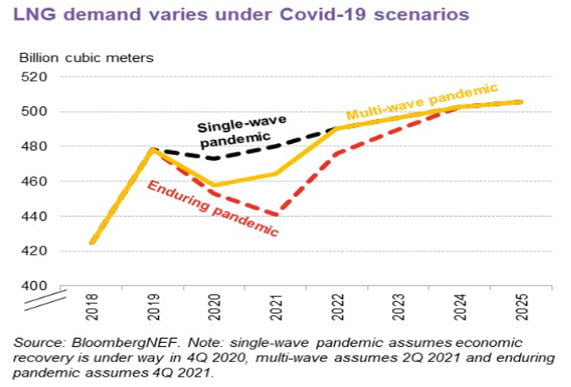

LNG trade is also expected to decline by 4.2% in our base-case scenario, which assumes a multi-wave pandemic where global GDP reaches 4Q 2019 level again only in 2Q 2021. If the pandemic endures further and economic recovery takes longer, the fall in gas demand could be ever steeper.

Fauziah Marzuki: If we start to see repeated waves of Covid-19 outbreaks which require suppression measures into 2021, then we could be looking at a drop in LNG demand in 2020 of 5.3%, falling further into 2021. The market won’t just feel the pinch of gas consumption dropping, but you’ll start to see a knock-on impact on gas infrastructure build out which is supposed to set the scene for future gas demand growth in emerging markets.

Will Kennedy: Fauziah, if we get the Covid crisis under control when do expect the LNG market to start balancing? Is there any hope for producers?

Fauziah Marzuki: If we get things under control before the year is out, then we will see LNG demand rebound in 2021. It will not recover to 2019 levels yet, but by 2022 we’ll see a situation where it gets back on track. Market still won’t be balanced though, the oversupply is still expected to persist. LNG producers will still need to make the difficult decision as to whether they need to curb supply beyond 2020.

Will Kennedy: Ashish, what if things get really bad again? How low can gas prices go? Any chance of seeing the negative prices we saw for oil in April?

Ashish Sethia: If the pandemic doesn’t get much worse than what we have already seen, then prices shouldn’t fall too much. In fact, in the last week, they have moved up a bit.

An interconnected global gas market, thanks to LNG, provides more flexibility and balancing mechanisms than before. U.S. export reduction, fuel switching in the power sector in Europe, higher use of storage in Ukraine, potentially profitable floating storage and price-sensitive demand in Asia can all kick in.

Will Kennedy: At what point does the persistent oversupply start hitting investment in new LNG projects, Fauziah? Is there a risk that some new supply will never get built?

Fauziah Marzuki: It already is! We’ve seen most would-be U.S. LNG producers announce delays to their final investment decisions to 2021. Though the delay can largely be attributed to the Covid-19 pandemic hitting the brakes on any deal-making, the oversupply outlook is making buyers think twice before committing to long-term supply to underpin new projects.

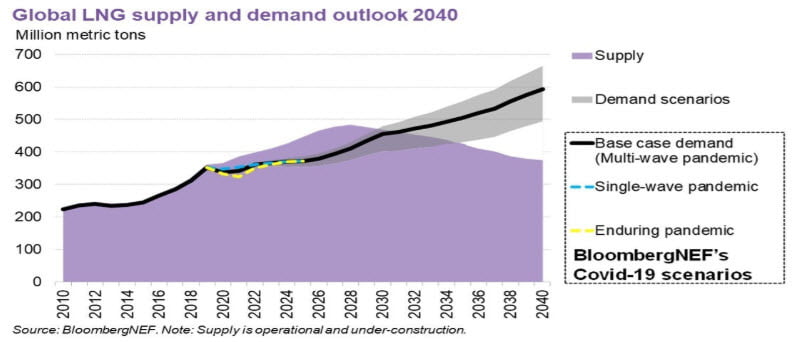

There will always be a risk that LNG supply proposals get shelved; some that are currently on the table have been around for a decade. Based on BloombergNEF’s latest LNG outlook, new supply will be required after 2030. So those decisions to build new LNG projects need to be taken before 2025.

Will Kennedy: Ashish, we have a question from a client. If we see lower gas demand over the coming decades, who are the midstream survivors?

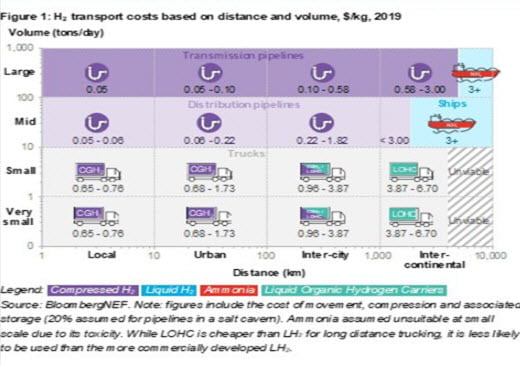

Ashish Sethia: Midstream players that could survive or even thrive in a low gas demand scenario would be the ones with large balance sheets and business model innovation. Innovation could include working on hydrogen as it gets cheaper to produce or investing in renewable energy. In fact, pipelines are going to be one of the most cost effective ways of transporting large volumes of hydrogen.

Will Kennedy: As a follow-up to that, Ashish, what do you make of Warren Buffett’s deal to buy Dominion Resources? Does that show some confidence in the industry’s future?

Ashish Sethia: Dominion’s deal with Berkshire reflects different risk appetite in the gas pipeline business. For Dominion the returns on transmission assets were getting difficult to predict -- something they aspire to do. It still has its gas power generation assets and will continue to operate local gas distribution business as well, which shows that the fuel is here to stay in the energy mix.

Will Kennedy: A question for both of you. We’ve talked about supply and demand fundamentals, but I’m interested in the impact of policy. The pandemic has pushed Europe to an unprecedented green stimulus and we could see a very different administration in the U.S. next year. How will that play into your outlook?

Ashish Sethia: The EU green stimulus is unprecedented in scale but was largely planned before the pandemic. Natural gas usage in the region is surely expected to decline in the long term to meet its climate goals. A large part of the stimulus is aimed to aid technologies like hydrogen. Firms in the gas market are trying to be relatively large players in hydrogen as well.

Fauziah Marzuki: A very different U.S. administration means potentially fewer approvals for U.S. LNG exports projects. However, most of the projects that the market is watching have already received all their permits from the government. A shift in energy policy direction in the U.S. could impact shale production, but it is unlikely to derail the outlook that the U.S. is going to be one of the largest natural gas supply growth engines into the 2040s.

There are still execution question marks around Joe Biden’s plan to ban new fracking permits on federally owned land. It is also difficult to see plans for zero percent emissions from the power sector by 2035 not having a profound impact for gas generators in the power sector, which would ultimately mean potentially curbing gas production.

Will Kennedy: Fauziah, a client question on the LNG shipping market for you. With floating storage in the money in Europe for late fall/early winter, is there a risk of a tightness in the shipping market? Could that limit the amount of cargoes that can be loaded from supply centers like the U.S.?

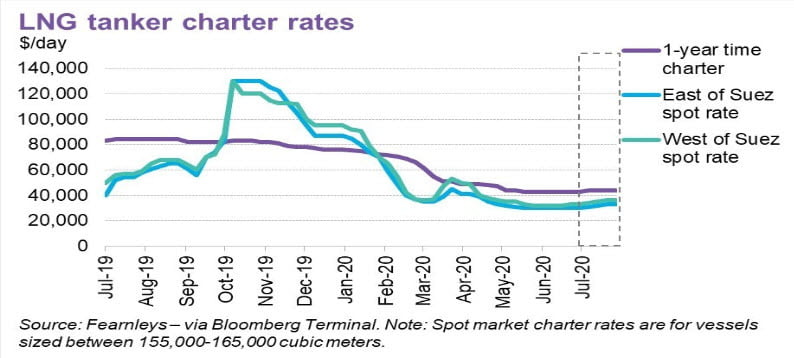

Fauziah Marzuki: We saw LNG spot charter rates dip as more and more U.S. LNG cargoes got cancelled in the summer, thus increasing the number of available tankers. Now as we approach the winter and floating storage is in the money, more traders will hold cargoes, but the difference now is that we’ve actually had a lot of new ships being delivered into the market. Just in July we saw at least three ships taking their maiden voyages.

Will Kennedy: Ashish, another client question. Is the growth of LNG, and low prices, making existing gas infrastructure in consuming countries uneconomic? Are we starting to see wells and pipelines close?

Ashish Sethia: Most of the new infrastructure in consuming countries is being built in Asia, where demand is expected to rise faster than domestic supply. For example, India’s dependence on LNG imports is expected to grow as demand almost doubles by 2040. In some markets in Southeast Asia, domestic production is expected to decline, pushing higher LNG imports. Similarly, in China, the government wants to raise the transmission pipeline capacity by a massive 60% in the next five years. So higher usage of local infrastructure is anticipated in general.

Will Kennedy: Ashish, there’s been a lot of buzz about the potential of hydrogen in the battle to cut carbon emissions. How do you see the interplay between natural gas and hydrogen panning out over the next couple of years?

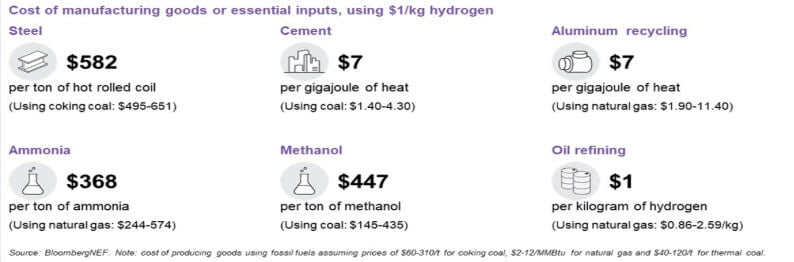

Ashish Sethia: Hydrogen could abate up to 37% of energy-related greenhouse gas emissions, according to BNEF estimates. It also can help reduce carbon emissions in the so-called hard-to-abate sectors like steel. There are a number of potential interplays between the natural gas industry and the hydrogen sector. Lots of hydrogen is currently produced from natural gas, and cheaper carbon-capture technologies can help raise gas usage.

Existing natural gas pipelines are also being used to blend hydrogen, although to a certain level, given technical constraints. Midstream companies with expertise in building, maintaining and operating pipelines can actually be the first ones to build dedicated hydrogen infrastructure in the future.

Will Kennedy: You’re an Asia specialist, Fauziah. As gas prices have slumped, we’ve seen a lot of switching from coal to gas in the U.S. and Europe. Is the same thing happening in Asian gas buyers like South Korea and Japan?

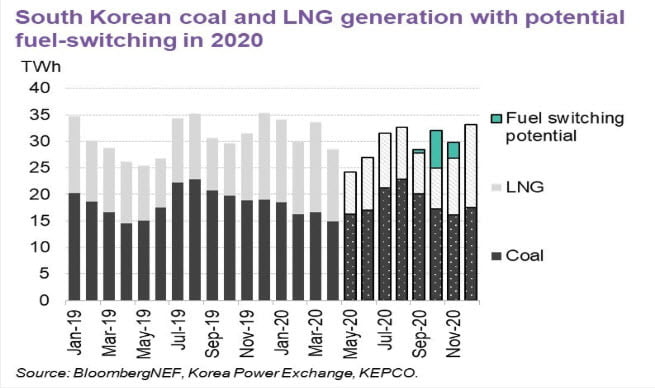

Fauziah Marzuki: The potential for economic coal-to-gas switching is more likely to emerge in South Korea, where they raised a tax on coal in April 2019. Potential is less certain for Japan where the fuel tax for coal is lower. Cheap coal spot prices would really diminish potential for fuel switching in the country.

The North Asian gas market is finally getting to see some activity in terms of fuel switching. Because Japan and South Korea’s LNG import price is pegged to oil prices, with a lag, the collapse in crude oil prices we saw in the first quarter won’t be reflected until the fourth quarter –- peak winter gas demand period for the region.

Will Kennedy: Ashish, the overall tone of the market is fairly downbeat. What are the potential demand surprises that could turn that story around?

Ashish Sethia: Apart from new infrastructure in Asia supporting demand, deregulation in many markets like China, South Korea and India means the arrival of more nimble private players. They have been a bright spot in terms of imports in the region and may continue to do so in the future.

Will Kennedy: Thank you everyone for reading and those who submitted questions and to Fauziah and Ashish for some very enlightening answers. Like every market, the outlook for gas will be shaped by the pandemic, but longer-term the pace of the energy transition will be key.