By BloombergNEF

By Maggie Kuang, BloombergNEF

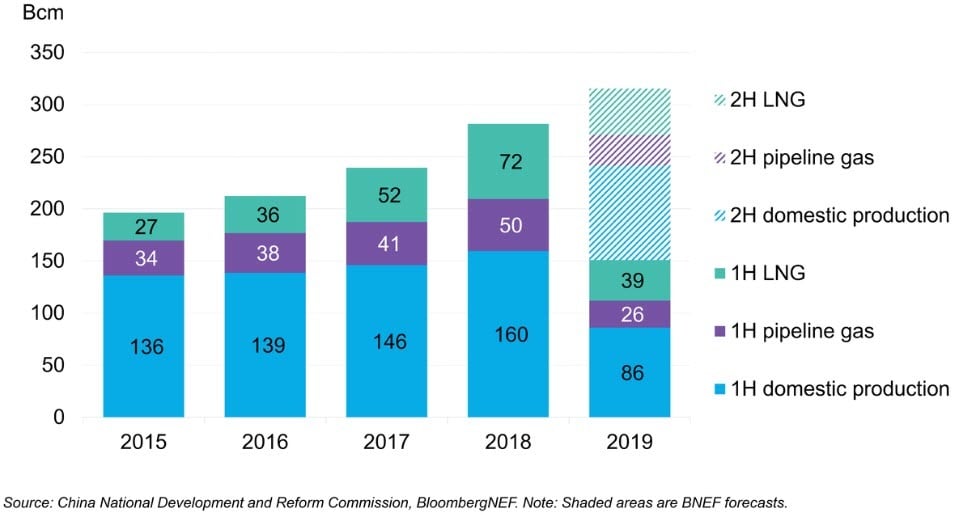

Low LNG prices failed to result in a noticeable demand response in China in the first half, with import growth primarily structural due to a slowdown in overall gas demand growth and modest ramp-up of pipeline gas supply. Although global oversupply persists in the second half and spot LNG will likely remain cheap, the chance for China's LNG demand to respond and grow beyond our expectation is slim.

A faster ramp-up of Kazakhstani supply in the second half and commissioning of Russia’s Power of Siberia pipeline will limit LNG's upside potential in the period. The impact on demand and supply from deeper gas market reforms in the first half via tax cuts, lower pipeline connection fees, and removing upstream investment restrictions will be minimum in the second.

BNEF maintains its forecast of 62 million metric tons of LNG imports in 2019.

China's gas supply by source

By Lujia Cao, BloombergNEF

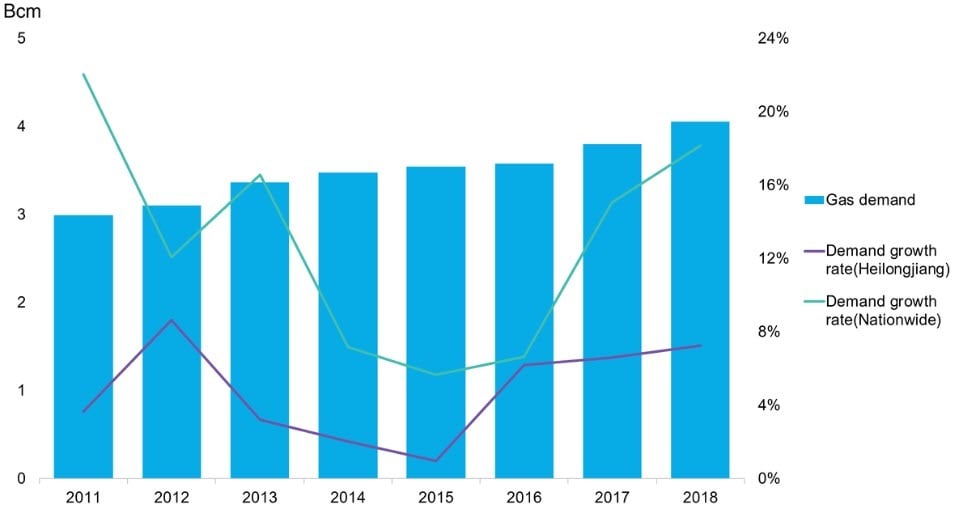

China National Petroleum Corp. (CNPC) has bagged a deal for a provincial gas pipeline construction from Heilongjiang on the back of its anticipated new gas supply from Russia. The job was earlier awarded to four city gas companies.

CNPC plans to provide 15 billion cubic meters gas for Northeast China, which is a huge attraction for the local governments. Jilin province also announced plans to cooperate with CNPC recently.

The next step for CNPC is a likely expansion of its gas retail business in provinces along the China-Russia line. This expansion into downstream retail would provide a hedge against risks from the national pipeline reform, which would take away its almost monopolistic control on gas trunk pipelines.

Heilongjiang gas demand and growth 2011-2018