By Henik Fung and contributing analyst Anthony Cham Fung Yau, Bloomberg Intelligence

Cnooc's strategic focus on increasing production and replacing reserves will make it better positioned for earnings growth in 2020-21. Output growth and cost control should support profit amid volatile oil prices. Cnooc will place greater emphasis on natural gas through domestic exploration and overseas acquisitions. The company will expand its LNG business in the coming years to fill the supply-demand gap in China. We see Cnooc's gas production growth to outpace that of oil in the long term.

CNOOC's 2H faces drag from weak oil prices: Earnings outlook

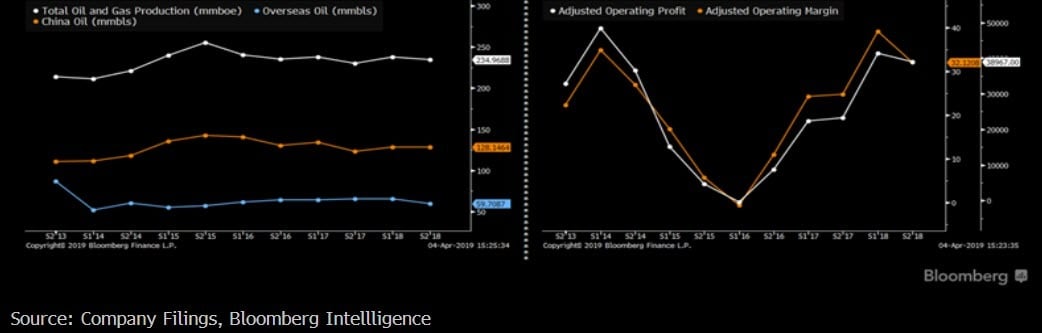

Post-1H Earnings Outlook: CNOOC Ltd.'s 2H earnings may be affected by weaker oil prices. 1H profit jumped 18.7% vs. a year earlier to 30 billion yuan, boosted by a 4.4% increase in oil and gas sales revenue. All-in cost was skillfully controlled at $28.99 a barrel in 1H, below $30.39 a barrel of fiscal 2018. 1H production volume was 243 million barrels of oil equivalent, up 2.5% vs. a year earlier, hitting 50% of its fiscal 2019 target. Realized oil price came in at $64.60 a barrel in 1H, down 4.1% in dollar terms but up 1.2% after including the impact of yuan depreciation. Global oil prices, a key earnings driver of CNOOC, may be adversely impacted in 2H by the trade tension between China and the U.S. The company declared a dividend of 33 Hong Kong cents a share, against 30 cents a share in 1H18.

Cnooc's production set to rise with solid profitability outlook

Cnooc is poised to increase its production and reserve-replacement ratio in coming years, given China President Xi Jinping's directive on energy security. The company aims to steadily increase its production to about 540 million barrels of oil equivalent in 2021. Capital spending will rise correspondingly to support the plan. Profitability should improve if oil-price recovery continues, yet part of the gains will be offset by higher costs. Some cost components, such as diesel, are linked to oil prices. Cnooc has lower upstream costs than PetroChina and Sinopec.