Oil and gas companies that omit Scope 3 emissions from transition strategies risk stranded assets and investor pressure, in our view. Shell and BP are among those to set ambitious low carbon-energy transition strategies. Exxon Mobil and others who fail to address such emissions exclude their biggest contribution to climate change.

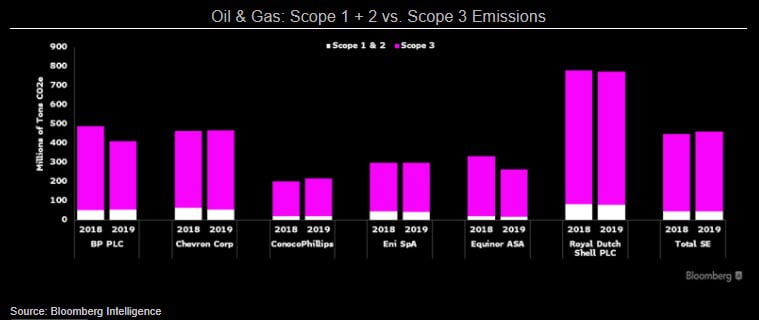

Our analysis of 39 oil and gas companies found that fewer than half report Scope 3 greenhouse gas (GHG) emissions, despite being more than 85% of the total footprint for the average company. Just eight of these companies use Scope 3 in their GHG reduction strategies, suggesting a significant gap as oil and gas companies aim to decarbonize. Shell, which seeks to achieve net-zero emissions by 2050, reports almost 700 million metric tons of Scope 3 emissions vs. 70 million for Scope 1 and 11 million for Scope 2. The company is aiming for net zero by improving operational efficiency and shifting toward natural gas, renewable-power generation and hydrogen.

This could reduce the carbon intensity of each unit of energy sold by 65%, while carbon capture and natural carbon sinks will address remaining Scope 3 emissions.

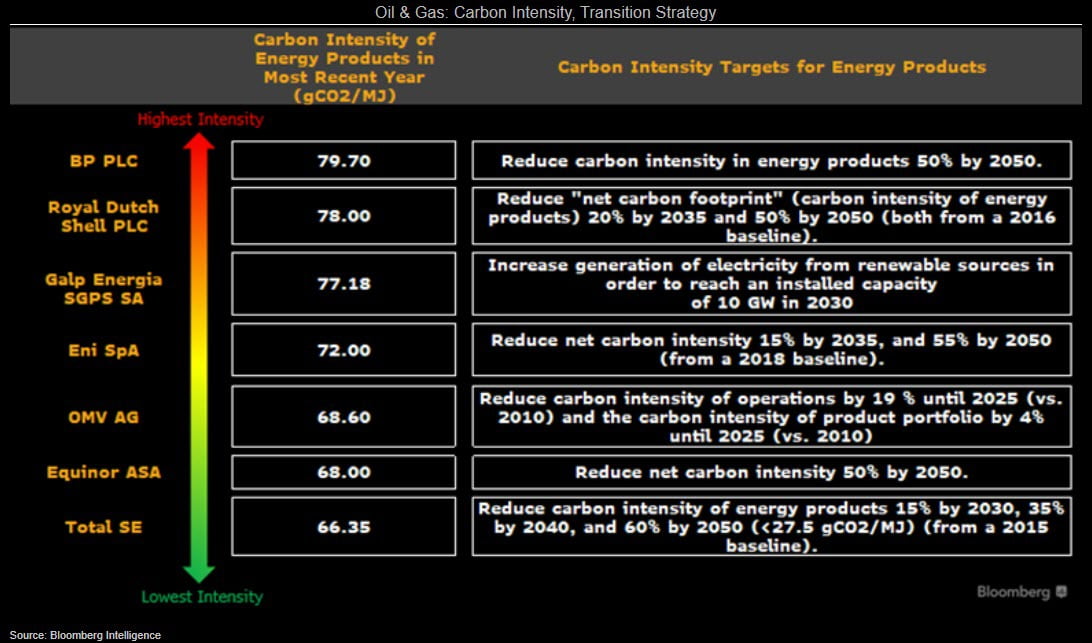

Only 20% of oil and gas companies analyzed have announced Scope 3 GHG-reduction targets, suggesting a majority of the sector may face risk in a low-carbon transition. Fewer disclose current carbon intensity (CO2e/megajoule) of the energy products they sell, which captures the overall carbon intensity of an energy product portfolio, including Scope 1, 2 and 3, and provides a measure of transition to low-carbon energy products. BP and Shell report the highest current carbon intensities, which are matched with ambitious transition strategies.

The Transition Pathways Initiative suggests that European oil and gas companies need to reduce their emissions intensity by 70% by 2050 from 2018 to align with a 2-degree Celsius climate scenario. A 1.5-degree scenario needs a 100% reduction in net emissions in the same period.

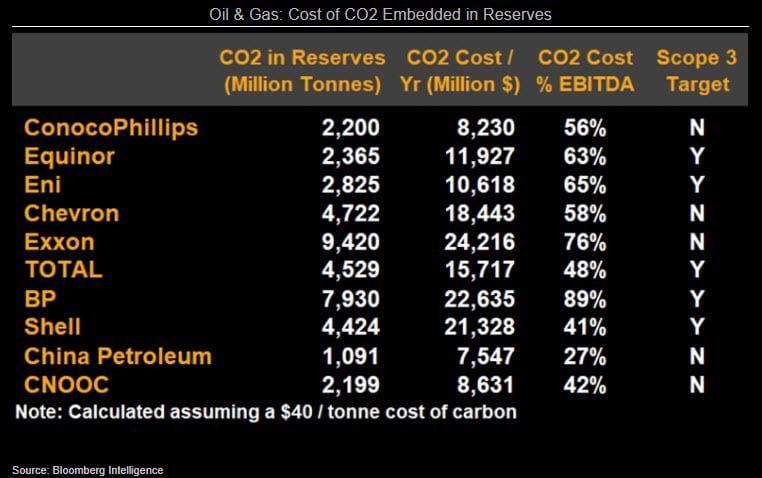

Oil and gas companies that don't reduce Scope 3 emission intensity may be more likely to strand assets, as policymakers curb fossil-fuel use in key regions. Our analysis, assuming $40 a metric ton for CO2 embedded in reserves, suggests carbon could account for almost 60% of average Ebitda for top producers. While carbon prices are hypothetical in many regions, some companies build them into internal calculations and advocate for the implementation of such mechanisms. Shell reports that its analysis assumes carbon prices will exceed 200 euros a ton of CO2e by 2050 to ensure the EU reaches climate neutrality.

Total, Cenovus, Eni, Suncor and BP are among members of the Carbon Pricing Leadership Coalition, a World Bank Initiative aimed at strengthening carbon pricing and applying it across the global economy.

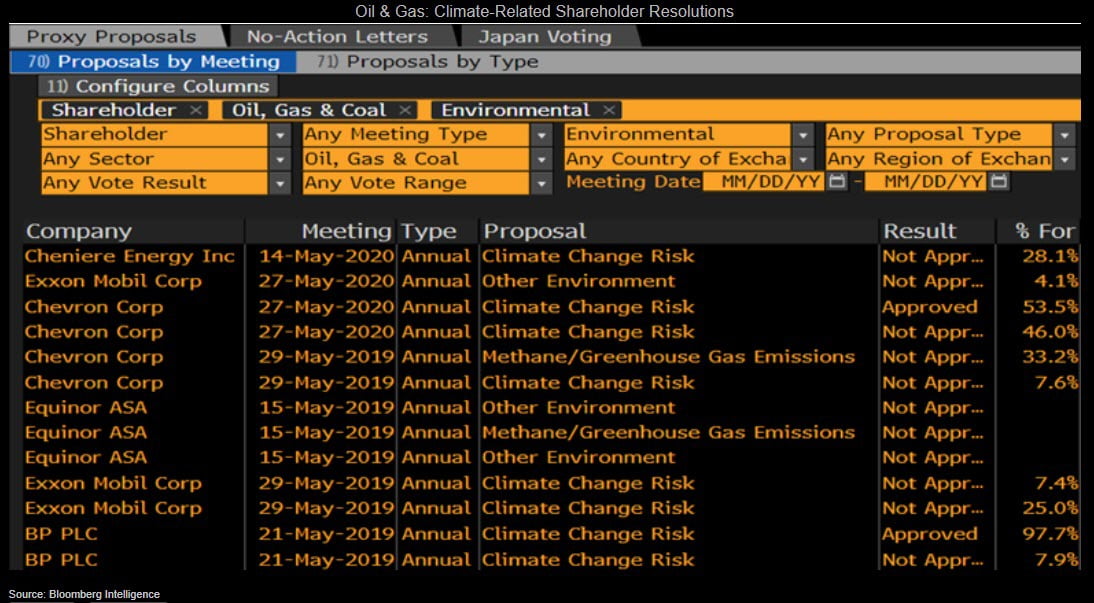

Top emitters that have yet to develop comprehensive greenhouse gas-emission reduction strategies, including Exxon Mobil, Chevron and Rosneft, will face increased investor scrutiny, in our view. As climate change presents risks to investment portfolios and assets, shareholders are seeking change at the companies that contribute most to global greenhouse-gas emissions. Since 2017, the Climate Action 100+ has grown to include more than 500 investors with over $47 trillion in assets under management.

Signatories to the group acknowledge that efforts to engage the world's largest greenhouse-gas emitters to curb emissions, improve governance and strengthen climate-related disclosures are consistent with their fiduciary duties. The list of target companies for the investor initiative includes almost 40 oil and gas companies.

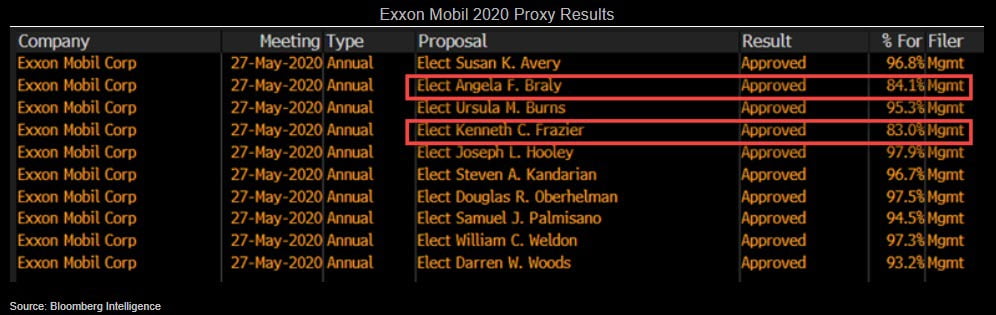

Following through on CEO Larry Fink's threat to vote against boards of companies BlackRock believes aren't doing enough to disclose and manage climate-change risk, the world's largest asset manager took action vs. Exxon Mobil. It withheld support for directors Kenneth Frazier (Exxon's lead independent director) and Angela Braly (public-issues committee chair), saying:

"When effective corporate governance is lacking ... voting against the re-election of the responsible directors is often the most impactful action a shareholder can take." These directors received shareholder support of 83% and 84% vs. a 96% average for other directors.

BlackRock also supported a resolution to require separation of the CEO and board chair roles to improve independent oversight and responsiveness of the Exxon board.