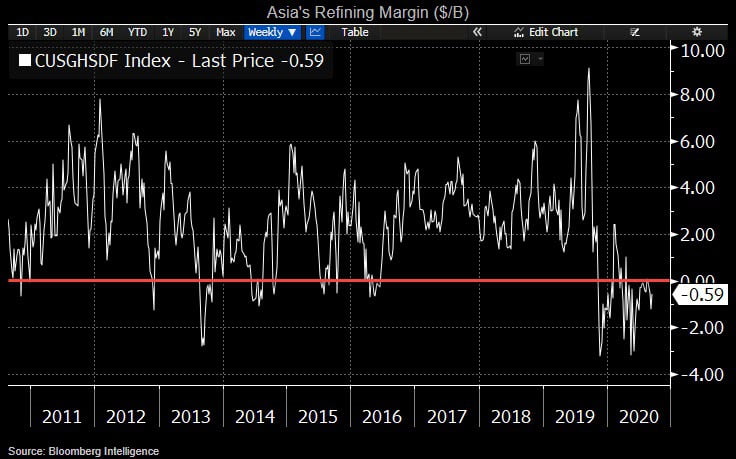

Rising oil-product inventories signal lasting energy demand weakness, which may keep a $40 lid on the oil price. A synchronized jump in road-fuel inventories in major markets could suggest that a demand uptick after June driven by restocking activities may have run its course, evident in Asia’s sub-zero refining margin.

Singapore’s complex refining margin may continue to languish below zero after falling to minus 38 cents a barrel on Sep. 11 vs. a $4.13 rolling five-year average. The negative margin has persisted since May when WTI led the way lower, as Asia’s gasoline and diesel demand remained sluggish, evident in China’s increased exports of transportation fuels. While the hit to consumption may not be as severe as in March, our analysis suggests net incremental oil-product supply of at least 2.5 million barrels per day (mmbpd) in 2H, and 4.2 mmbpd in 2021. A renewed COVID-19 threat may worsen the supply-demand gap, rendering a full recovery elusive.

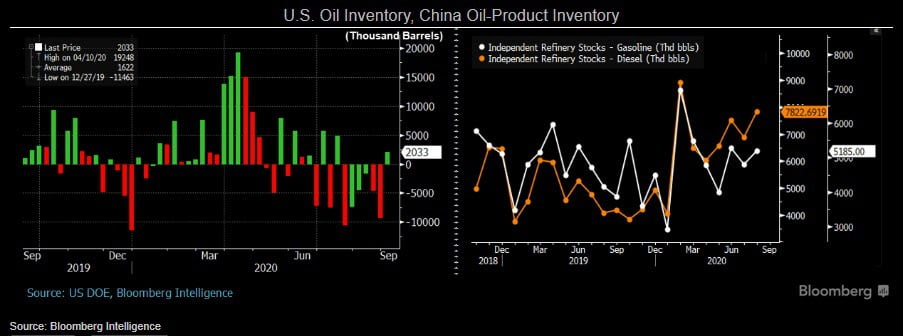

Optimism over recovering oil demand has fuelled a WTI’s price rally to the $40 level. Yet a buildup of global inventory suggests demand remains sluggish, rendering a sustainable oil-price rebound far-reaching. The U.S. Department of Energy indicates crude inventory rose by 2 million barrels to 500 million barrels in the week of Sept. 4, reversing the downtrend since July. China’s August gasoline and diesel inventories at independent refineries were 13 million barrels, 11% higher vs. July. Without a steep pick-up in demand, oil and oil-product inventories may keep swelling, pressuring the crude price.

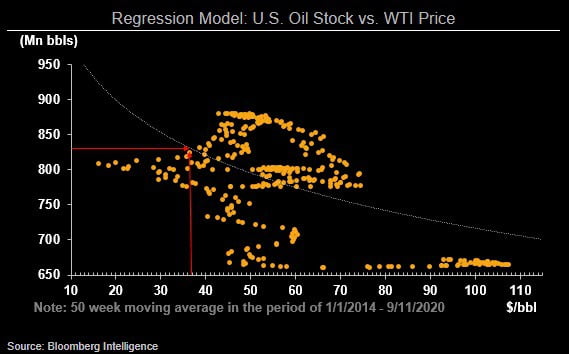

Short-dated oil futures are better proxies than spot for short-term market-price shifts, in our view, as traders tend to use them to capture price volatility. Our price-inventory model suggests WTI crude futures would have traded at the spot price of $37.33 on Sept. 11 if U.S. comparative inventory — crude oil, gasoline and diesel — had fallen to 830 million barrels from 900 million barrels. This implies the market expects oil supply and demand to balance out by end-2020, with inventory shrinking by 65 million barrels. Global demand can recover, in our view, yet it may not be enough to fully absorb inventory. A revival in shale-oil production, escalating U.S.-China tensions and a potential second wave of the pandemic could hamper a crude-price rebound.