U.S. oil and gas producers' climate ambitions still lag those of European peers. While the latter group has ambitious wind- and solar-growth targets, where returns are low, the U.S. majors focus more on reducing emission intensity by improving existing oil and gas operations' efficiency, boosting the share of renewable and biodiesel in their output mix.

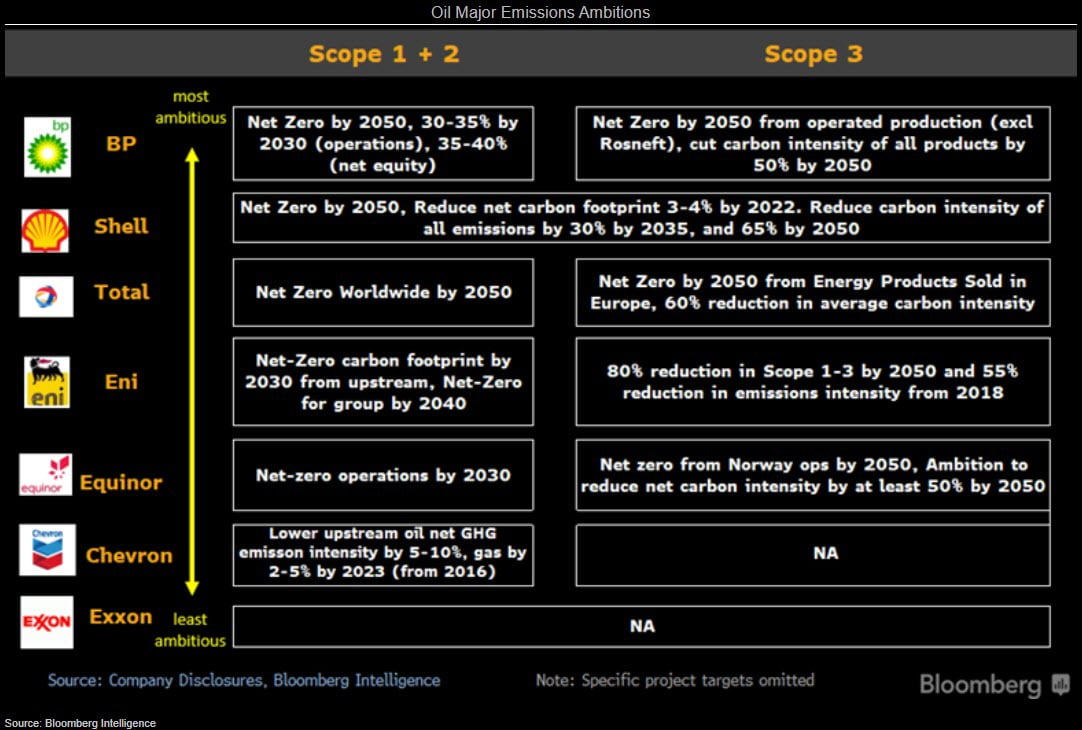

European oil majors have announced increasingly ambitious emissions objectives over the past 12 months, with most outlining various iterations of achieving net zero absolute emissions (Scope 1-3) by 2050, with some accompanied by intensity-based targets. A divergent approach toward emissions reduction between European oil majors and their U.S. peers is widening, we believe, with Exxon and Chevron declining to provide specific absolute emissions targets. We view BP and Shell's emissions plan as the most comprehensive and ambitious, given both have a net-zero target by 2050, leading targets for reduction in emissions intensity and inclusion of short-term targets linked to executive compensation.

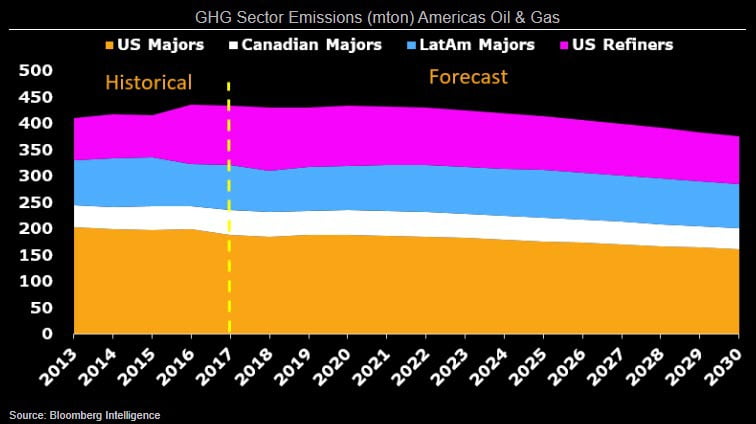

Investments in more productive assets should improve Big Oil's carbon intensity. The previous investment cycle was focused on marginal assets, as triple-digit oil prices enabled more technically complex and smaller-payout projects, but the drop in crude prices has accelerated the need for the industry to focus on capital efficiency that should translate into lower greenhouse gas emissions per unit of production. Pressure from investors and regulators is also bearing fruit, as more companies in the Americas adopt emission targets as part of their investment frameworks.

Disclosure still trails European peers, and none of the major players have added emissions targets to compensation structures, in part due to ambiguity in their calculation and comparability.

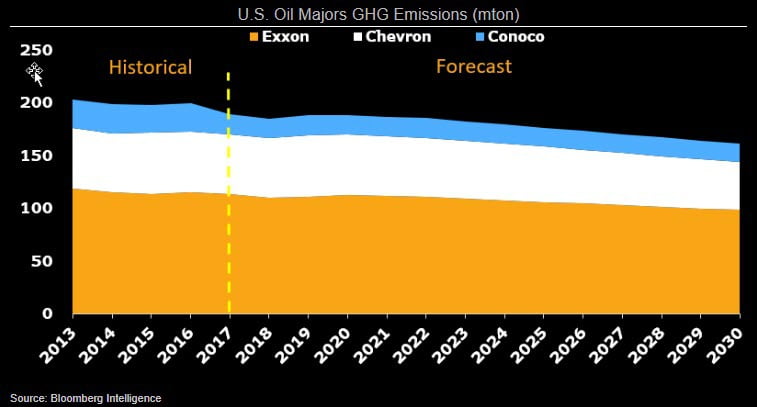

U.S. majors have begun taking a more aggressive stance on climate change after considerable pressure from shareholders and society. Exxon Mobil has been at the epicenter of the climate-change discussion, and under CEO Darren Woods has increased disclosures on emissions and set targets for reduction in carbon and methane intensity. Chevron and ConocoPhillips have set targets to reduce greenhouse gas emissions, and in particular reduce methane emissions and flaring.

Unlike Europeans, U.S. majors aren't moving toward utility or mitigation efforts such as reforestation, but with growing pressure from ESG funds, we expect disclosures and investments in energy transition will accelerate over the coming years. To date, U.S. majors have largely preferred new energies as opposed to incumbent renewables.

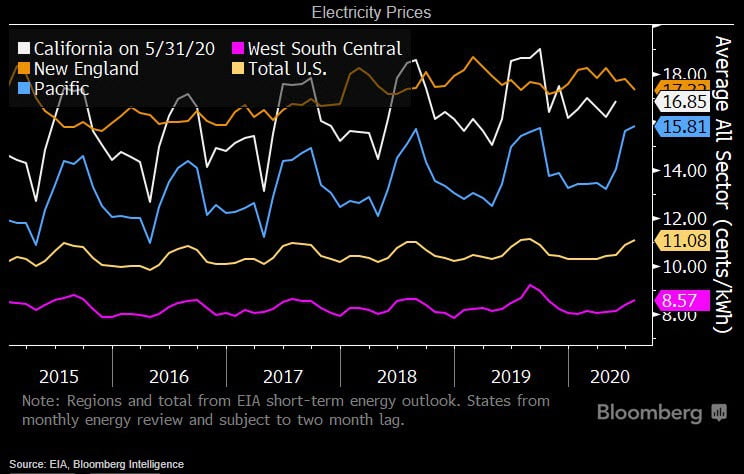

Rising power costs and blackouts in California substantiate Exxon Mobil and Chevron's claim that natural gas is a transition fuel until the world can afford abundant and affordable energy storage. Both still have sizable North American natural gas portfolios and would gain from a push to increase methane's role in the U.S. power grid. ConocoPhillips, BP and Shell also have substantial acreage in the U.S. and could benefit if the issues in California change demand patterns. Each megawatt hour would lead to an increase of about 3,410 cubic feet of demand.

North America has a substantial natural-gas base that can be exploited over the coming decades. The EIA expects the share of electricity generated by natural gas to decline 1% to 36% by 2025, but still grow 18% in total (0.5% a year).

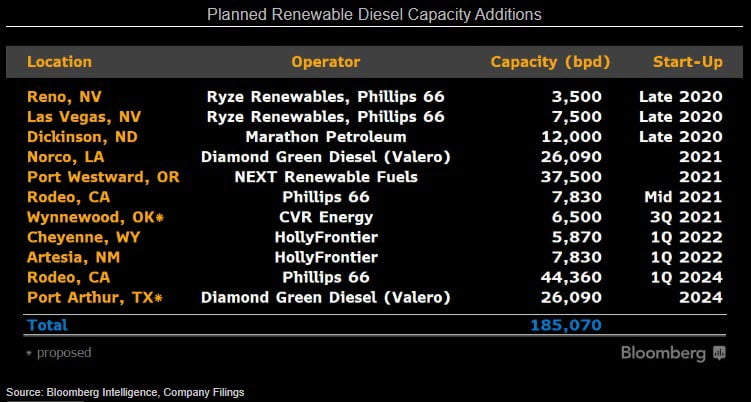

Refiners' push to build renewable diesel units, boasting 30% returns on capital, are underpinned by government subsidies and a belief that carbon regulations will become more stringent. But those economics are still heavily reliant on current incentives, some of which will diminish as more renewable diesel comes online and municipalities struggle with the fiscal burden of Covid-19. More than 185,000 barrels a day of new capacity will come online by 2024, about 3% of U.S. diesel capacity. More projects that could reduce incentives from renewable credits are under study, but the closings of refineries could at least partly mitigate the impact on margins.

There's no risk of oversupply, as renewable diesel has the same properties as regular diesel and can go directly into existing infrastructure, in contrast to biodiesel.

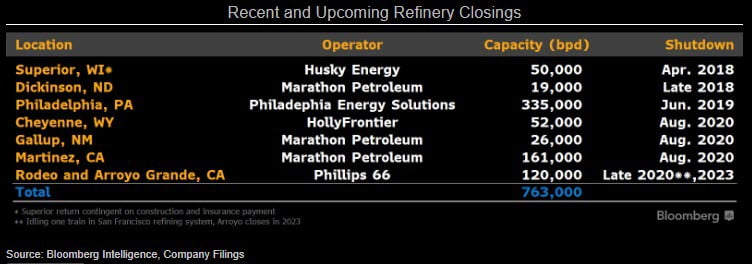

The reduction in demand due to COVID-19 accelerated the closings of marginal refineries and those facing increased regulatory scrutiny, mainly in California. Marathon Petroleum and Phillips 66 closed refineries near San Francisco, as mandates to cut carbon emissions will make refining in the state even more challenging. HollyFrontier's Cheyenne and Marathon's Dickinson plants saw narrowing crude spreads eat into margins, and conversion will generate renewable fuel credits (RINs) that can mitigate exposure in the rest of their portfolios. Refiners with large RIN exposure such as CVR Energy, PBF and Delek could also look to convert units or even full plants to renewable diesel to mitigate costs, but they're challenged by weak balance sheets.

Valero's Green Diamond partnership aims to be the largest renewable diesel producer.