Oil companies' pivot toward a cleaner asset mix is an enduring trend that will blur the lines with utilities. Both groups will focus on growing renewable capacity, retail customers, hydrogen, battery and EV-charging facilities. For oil majors, the long-term investment level will depend on whether they can make a decent return on these vs. the core oil and gas business.

The move by integrated oil companies to transition into broader integrated energy companies is irreversible, in our view. It will see the industry increase investments in deploying renewable and gas-fired generation, battery storage and EV-charging infrastructure, expanding electricity and gas-retail customers, as well as backing hydrogen and carbon capture, utilitzation and storage technologies. This will blur the lines and increase competition between oil companies and utilities. Utilities will likely maintain a lead over Big Oil in renewables and electricity-retail businesses over the next five years due to the huge gap between the two groups.

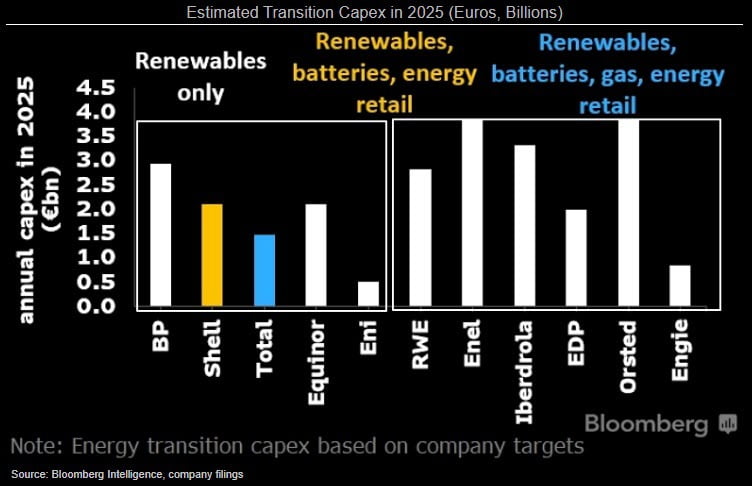

When it comes to investing in renewables, oil and gas companies may narrow the gap with utilities by the mid 2020s. By then, we expect Europe's top-five oil companies to invest more than 9 billion euros in energy transition -- mostly wind, solar -- but also into battery storage, power and gas supply and gas-fired generation, which would still be half of what utilities will invest in renewables alone. BP's 2025 renewable investment target $3-$4 billion is the most ambitious among its oil and gas peers, yet it may significantly lag behind the amount that Orsted, Enel and Iberdrola plan to spend on renewables that year.

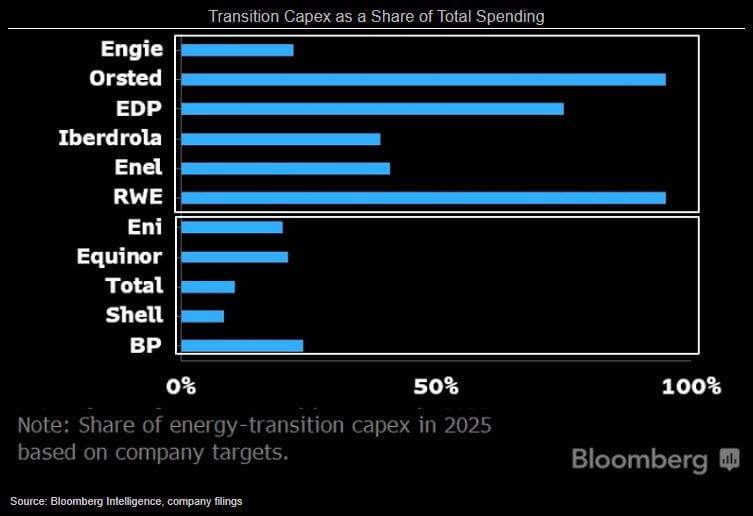

European oil majors may keep dedicating a much lower share of their total capital expenditures to renewables compared with utilities over the next decade, we believe. Top-five European oil and gas companies will increase the share of transition investments as a proportion of their overall capital expenditures to about 20% by 2025 (from about 5-10% today) compared with more than 60% for the six major listed utilities, according to our estimates, based on management guidance.

RWE and Orsted may direct a higher proportion of their 2025 capital expenditure toward renewables compared with utility peers Enel, Iberdrola, EDP and Engie. Among oil companies, transition investments may account for a higher share of BP, Equinor and Eni's 2025 budget compared with Shell and Total.

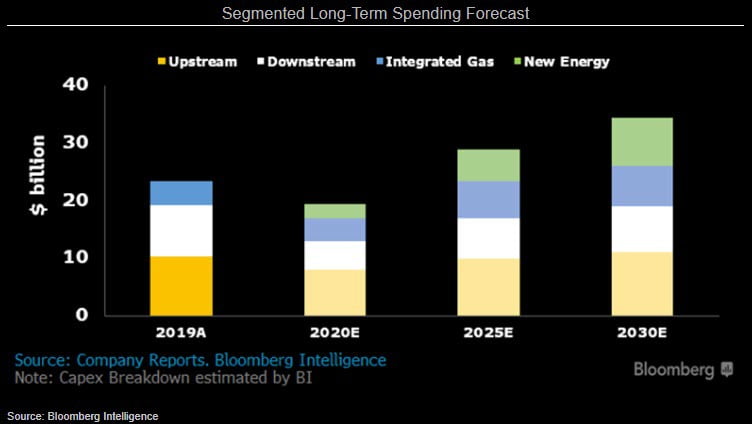

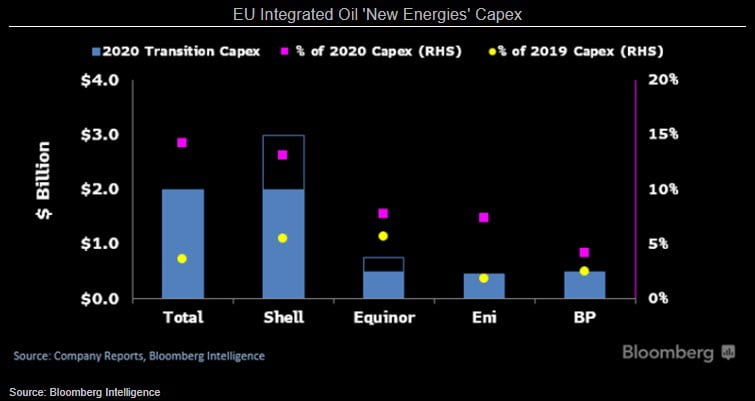

Shell's new-energy investment could climb to at least 25% of annual spending by 2030 vs. about 10% in 2020, we believe. Suggestions from Maarten Wetselaar, Shell's director of Integrated Gas and New Energies, that its annual $1-$2 billion budget for its new-energy division could double beyond 2020, will be conditional on returns achieved. We note this compares to company guidance of an average $2-$3 billion a year from 2021-25. Near-term new-energy capital allocation still pales in comparison with upstream spending, which will comprise more than half of this year's annual investment, and downstream about one-third. Shell has sharply reduced its 2020 spending to $19 billion from $24 billion originally, in response to the COVID-19 pandemic and a collapse in oil prices.

Shell's solar-wind portfolio with combined installed net capacity of about 1GW is broadly in-line with other EU oil majors, but is a small fraction vs. leading solar and wind utility providers. For Shell to meet just the existing renewable capacity of utilities would require a 15x multiple scale of growth from current levels, and doesn't include other power generation (nuclear, hydro, CCGT). We note Shell currently aims to have 5GW of installed renewable capacity by 2025, which is among the most conservative targets of EU peers, suggesting an acceleration beyond 2025.

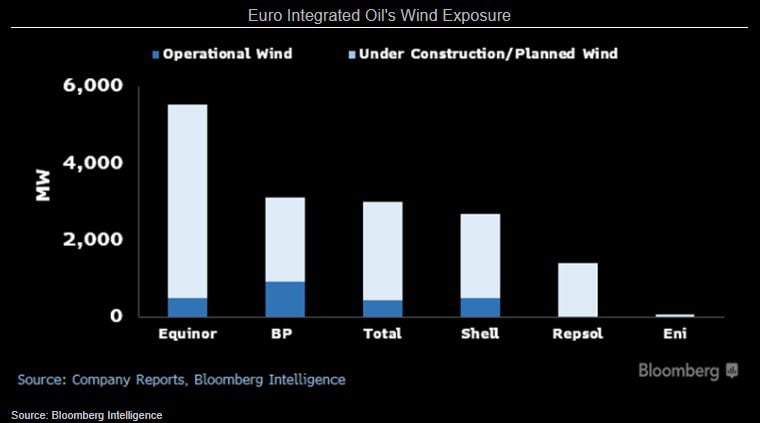

Shell's operational wind portfolio of about 500MW is comprised from onshore wind farms in the U.S., and a 50% interest in Noordzeewind farm in the Netherlands. Shell's solar capacity is primarily from its 44% interest in Silicon Ranch in the U.S.

European integrated oil companies have centered their renewable-growth strategies around wind, particularly offshore, citing the complementary nature of development with offshore oil installations and wind's declining costs, improving turbine technology and mounting policy support. With its acquisition of Empire and Beacon wind development leases, BP has now joined Equinor and Shell as the leaders in offshore wind, holding multi-gigawatt unsanctioned development potential off the northeast shore of the U.S. We see a path for 5-10x increases in their installed net wind capacity by the mid-2020s.

BP holds the largest existing installed wind capacity among peers, exclusively through onshore U.S. wind farms. Total's portfolio includes onshore wind assets in France, via its ownership of Quadran.

Roughly 10% of European integrated oil's annual capital spending this year is being deployed into green technology, renewables and transition businesses, which we see accelerating further to at least quintuple by 2030. We note that BP aims to increase its low-carbon investment tenfold to $5 billion a year by 2030. Both Equinor and Total have signaled that up to 20% of annual investment could be low-carbon by 2030, which we deem conservative. Wind power is also forecast to increase fivefold in scale to about 15% of global power generation by 2040, according to BP's energy outlook, which we expect to be largely achieved via offshore development.

Global wind-power generation reached 651 GW in 2018 (10% offshore), equating to about 5% of global electricity generation.